Paying for College Without Going Broke, 2017 Edition - Princeton Review, Kalman Chany (2016)

Part II. How to Take Control of the Process

Chapter 3. Short-Term Strategies for Receiving More Financial Aid

A “Snapshot” of Your Financial Picture

Each year your son or daughter is in college, the school will ask you to fill out a form reporting income and assets—in effect a snapshot of your overall financial picture. You’ve probably noticed that snapshots can be very misleading. In one picture, you may appear youthful and vibrant. In another, you may look terrible, with a double chin and 20 extra pounds. Perhaps neither photograph is exactly correct. Of course, when you are deciding which picture to put in the scrapbook, the choice is easy: throw away the one you don’t like and keep the one you do.

In choosing which financial snapshot to send to the colleges, the object is a little bit different: send them the worst-looking picture you can find.

To be very blunt, the single most effective way to reduce the family contribution is to make your income and your assets look as small as possible.

Well, This Is Not Revolutionary Advice

After all, you’ve been trying to do this for years.

We’re sure you and your accountant are generally doing a fine job of keeping your taxes to a minimum. However, certain long-term tax strategies that normally make all kinds of sense, can explode in your face during college years. Neither you nor your accountant may fully grasp how important it is to understand the ins and outs of the financial aid formulas.

How College Planning Affects Tax Planning

There are two reasons why tax planning has to change during college years.

First, the FAOs (unlike the IRS) are concerned about only four years of your financial life. Using strategies we will be showing you in the next few chapters, you may be able to shift income out of those four years, thus increasing your financial aid.

Second, financial aid formulas differ from the IRS formulas in several key ways. Certain long-term tax reduction strategies (shifting income to other family members, for example) can actually increase the amount of college tuition you will pay. However, astute parents who understand these differences will find that there are some wonderful, legal, logical alternatives they can explore to change the four snapshots the college will take of their income and assets.

Tax accountants who do not understand the financial aid process (and in our experience, this includes most of them) can actually hurt your chances for financial aid.

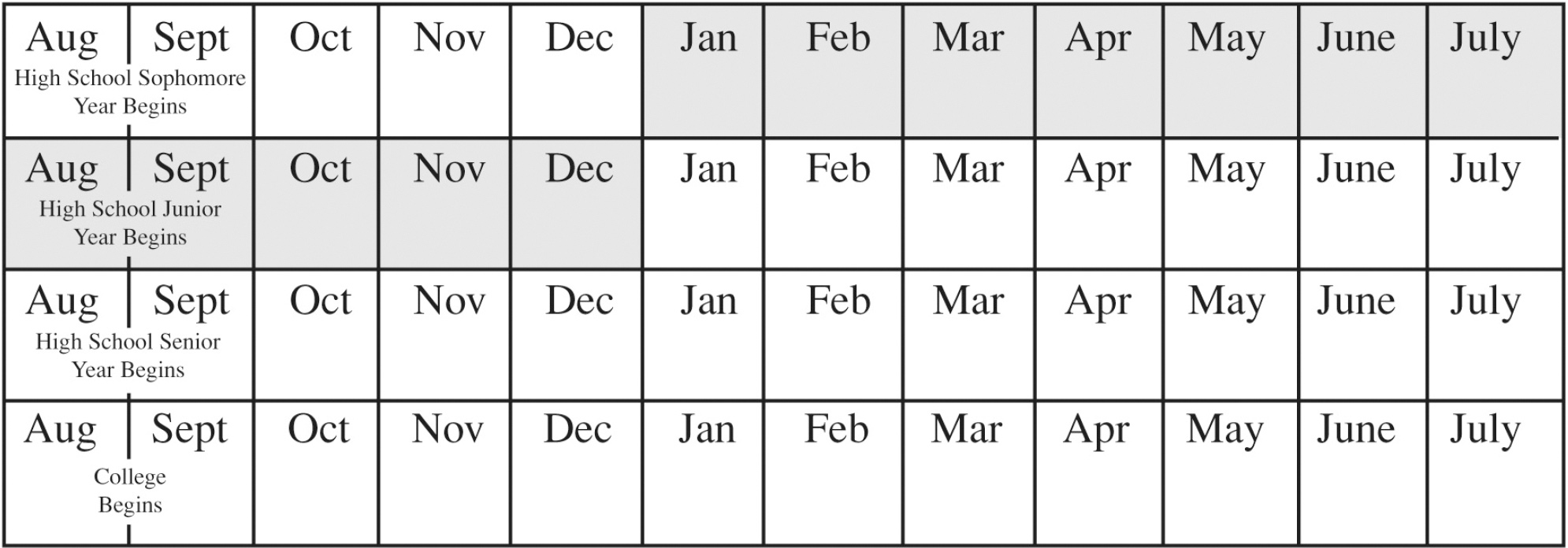

The First Base Year Income

Colleges base your ability to pay this year’s tuition not on what you made this year; not even on what you made last year; they base it on what you made the year before that. This may seem like ancient history, but the colleges have their complicated reasons (which we’ll go into later). Thus the first financial aid scrutiny you will undergo will not be directed at the calendar year during which your child will start her freshman year of college, but two years before. That year is called the first base income year and is the crucial one.

The base income year (shaded in the diagram that follows) extends from January 1 of your child’s sophomore year in high school to December 31 of your child’s junior year in high school. This is when first impressions are formed. The college will get an idea of how much you are likely to be able to afford, not just for the first year of school, but for the remaining years as well. First impressions are likely to endure and are often very difficult to change. Thus it would be helpful to remove as much income as possible from this calendar year.

What If I’m Already Past the Base Income Year?

If you are reading this book and your son or daughter is already in the spring term of junior year in high school, then you have probably missed the chance to make adjustments to your income for the base income year—but don’t despair. First of all, there are three other years still to go; the strategies we outline below can be used to lower the appearance of income in the years to come. And second, you haven’t missed the chance to make adjustments to your assets. That snapshot gets taken on the day you fill out the forms. We’ll talk about assets a little later in this chapter.

What If I’m In the Middle of the Base Income Year?

If you are reading this book and you are still in the base income year, there are a bunch of very specific things you can do to minimize the appearance of income.

What If My Income Radically Changes Between the Base Income Year and When My Daughter Starts College?

If your income has gone up since the base income year, that’s great. No need to report the change, unless you are asked to by an individual college. However, if your income has gone markedly down since the base income year, you can always write to the colleges and explain. We’ll describe this process, called an “appeal”, later in this book.

I’m About to Get a Raise. Should I Say No?

It’s easy to get carried away with the concept of reducing income, and it may appear at first that you would be better off turning down a raise. However, the short answer to this question is,

“Are you crazy?”

More money is always good. Our discussion here is limited to minimizing the appearance of more money. Let’s say you get a raise of $3,000 per year. This will certainly reduce your eligibility for college aid, but will it negate the entire effect of the raise? Not likely. Let’s say you’re in the 25% federal tax bracket, your raise is still subject to social security taxes of 7.65%, and your income is being assessed at the maximum rate possible under the aid formulas. Looking at the chart that follows, you’ll see that even after taxes and reduced aid eligibility are taken into account, you will still be $1,170 ahead, though state and local taxes might reduce this somewhat.

|

raise of: |

$3,000 |

|

|

minus: |

federal tax |

$750 |

|

FICA taxes |

$230 |

|

|

reduced aid |

$878 |

|

|

what you keep: |

$1,170 |

My Spouse Works. Should He or She Quit?

The same principle applies here. More money is good. Not only are you getting the advantage of extra income but also under the federal financial aid formula, for a two-parent family with both parents working, 35% of the first $11,429 the spouse with the lower income earns is deducted as an “employment allowance”. (The same deduction is granted for a single parent household if that parent works.) Even if this increased income decreases your aid eligibility, you will still be ahead on the income. In addition, you will be creating the impression of a family with a work ethic, which can be very helpful in negotiating with FAOs later. FAOs work for their living, and probably earn less than you do. They are more likely to give additional aid to families who have demonstrated their willingness to make sacrifices.

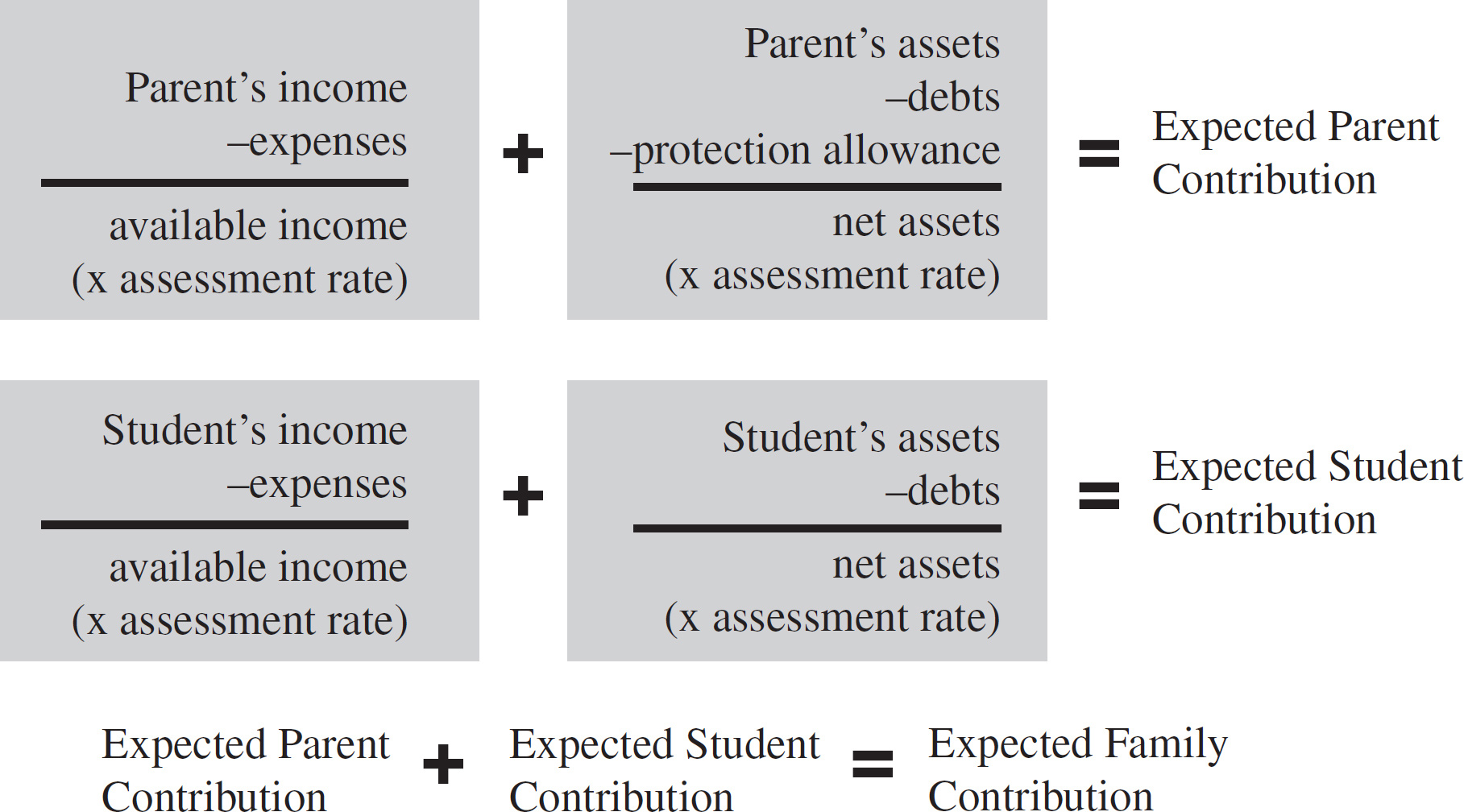

Income vs. Assets

Some parents get confused by the differences between what is considered income and what are considered assets. Assets are the money, property, and other financial instruments you’ve been able to accumulate over time. Income, on the other hand, is the money you actually earned or otherwise received during the past year, including interest and dividends from your assets.

The IRS never asks you to report your assets on your 1040—only the income you received from these assets. Colleges, on the other hand, are very interested in your income and your assets. Later in this chapter, there will be an entire section devoted to strategies for reducing the appearance of your assets. For now, let’s focus on income.

The colleges decided long ago that income should be assessed much more heavily than assets. The intention is that when a family is finished paying for college, there should be something left in the bank. (Don’t start feeling grateful just yet. This works only as long as the colleges meet a family’s need in full.)

INCOME

When considering their chances for financial aid, many families believe that the colleges are interested only in how much income you make from work. If this were the case, the colleges would just be able to look at your W-2 form to see if you qualified for aid. Unfortunately, life is not so simple. The college’s complicated formulas make the IRS tax code look like child’s play.

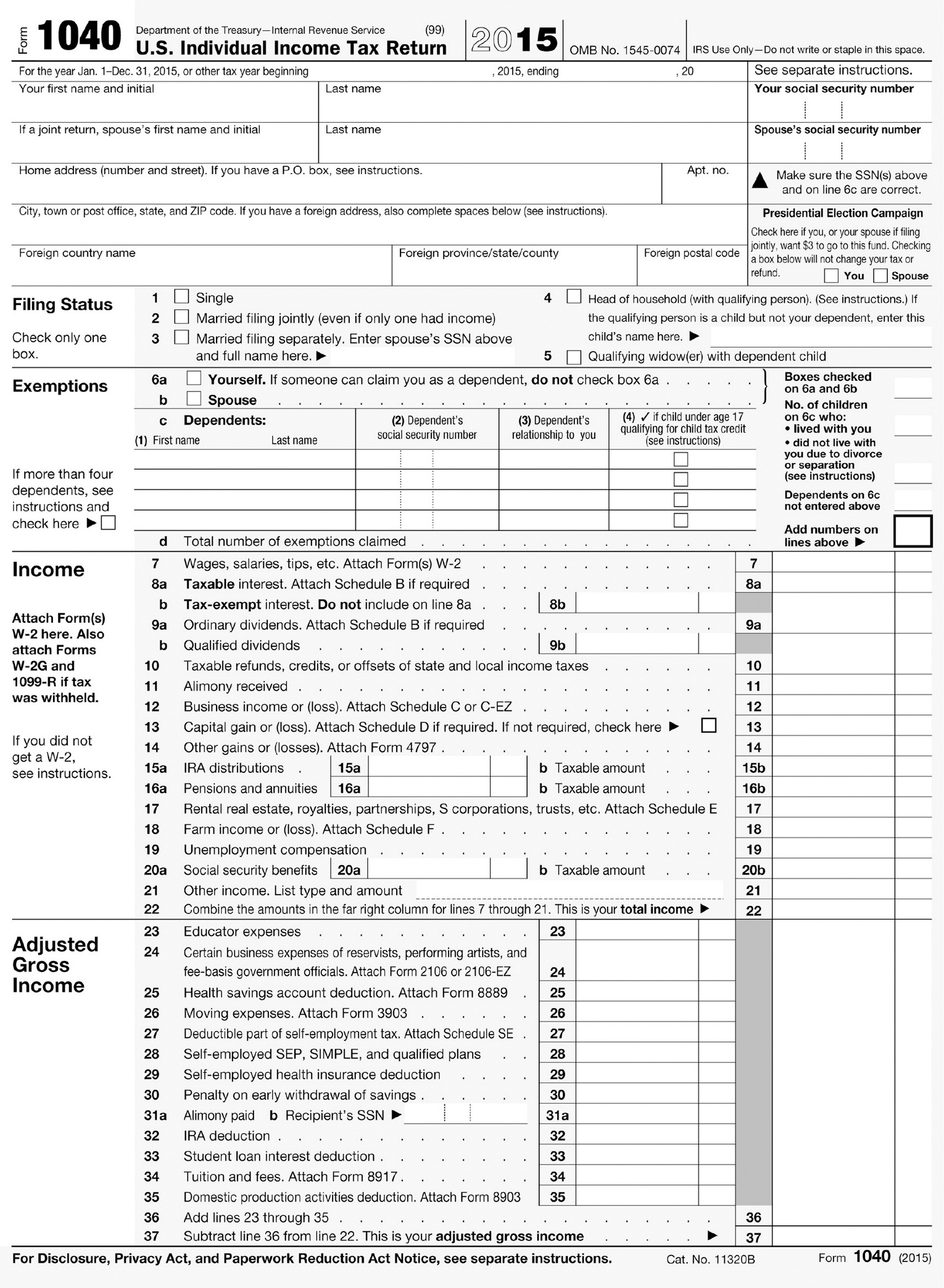

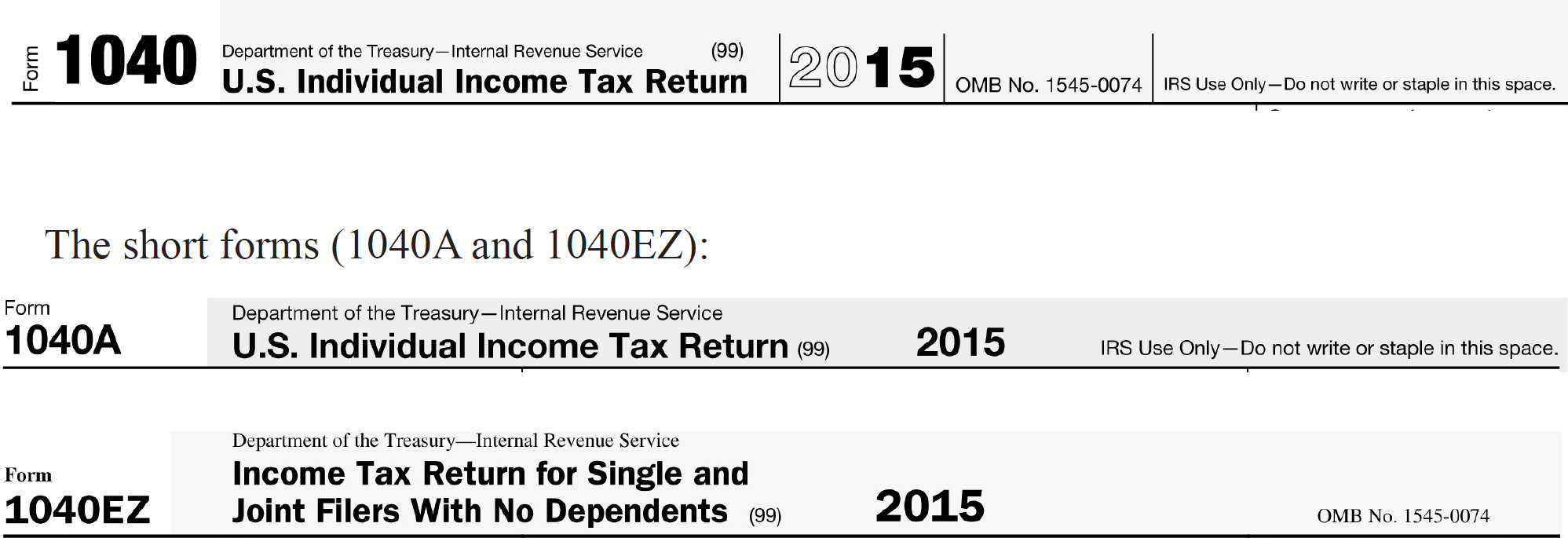

For financial aid purposes, the colleges will be looking at the same income the IRS does. For most of us, that boils down to line 37 of the 1040 IRS form: the Adjusted Gross Income or AGI. (By the way, if you use form 1040A, the AGI is found on line 21; if you use the 1040EZ form, it is on line 4. For simplicity’s sake, from now on, we will refer just to the 1040 long form and line 37.)

But for those who file a tax return, the colleges also look at certain other types of income that are not subject to tax, for example, child support, tax-exempt interest, voluntary contributions to a 401(k) plan or other tax-deferred retirement plan.

For those who don’t file a return, the colleges will still look at income earned from work plus other untaxed income.

Before we begin discussing the components of taxable and untaxed income, it is important to understand that even the decision as to which tax form to file (1040 long form vs. the 1040EZ or the 1040A) the student’s parents file can have a significant impact on your eligibility for financial aid.

Not All Tax Returns Are Created Equal

By filing one of the short forms (1040A or 1040EZ), and meeting certain other requirements, you may be able to have parent and student assets excluded from the federal financial aid formulas, which could qualify you for increased federal aid. This is a financial aid loophole known as the “Simplified Needs Test” (SNT). Here’s the way it works: If the parents have adjusted gross income below $50,000, (or for non-tax filers, have income from work which for most means wages reported on a W-2 form below $50,000), and the parent(s) in the household who file a tax return can use the 1040EZ or the 1040A form (or are not required to file any personal income tax return), then all your family’s assets will be excluded from the federal financial aid formulas. This means that eligibility for the Pell Grant, for undergraduate students, and the subsidized Stafford loan will be determined without regard to how much money the parent or the student has in the bank or in a brokerage account.

Click here to download a PDF sample of IRS Form 1040.

It can also be vital to parents with large assets but little real earned income. You can have $49,999 of interest income, and still possibly meet the simplified needs test—in which case even assets of several million dollars will not be used in calculating your EFC.

This can be particularly vital to parents with income below $40,000 but who have significant assets because they now may be able to qualify for the Pell Grant, which is free money that does not have to be paid back.

Of course, many colleges use the College Board’s institutional methodology (which does not utilize the simplified needs test) in awarding their own grant money. However, if you meet the Simplified Needs Test, they cannot use the family assets in determining eligibility for the Pell Grant, and subsidized Stafford loans. If you aren’t sure if you can use the short tax forms, consult the IRS instructions to the forms, or your tax preparer. A few examples of people who can’t use the short form: a self-employed individual, a partner in a partnership, a shareholder in an S corporation, a beneficiary of an estate or trust. In addition, if you had rental or royalty income and expenses, had farm income and expenses, took certain types of capital gains or losses, received alimony, or itemized deductions, you will have to file the long form if you are required to file.

However, for some taxpayers who could itemize deductions, but won’t save much money by doing so, it may still make sense to file the short form if otherwise eligible to do so. You’ll pay slightly higher taxes, but this may be more than offset by a larger aid package. Since this strategy requires a trade-off between tax benefits and aid benefits, we recommend you consult a competent advisor.

Unfortunately, even if you fit the simplified needs test, your accountant may unwittingly blow this lovely loophole for you by insisting on filing the wrong form.

Not All Accountants Are Created Equal

Many accountants are not aware of the aid laws and will try to talk you into using the 1040—simply because that is the only form their computer programs will print out. If you meet the simplified needs test, be prepared to insist that your tax preparer use the 1040EZ or the 1040A forms. It might not even be a bad idea to take this book along with you when you go for your annual appointment with your tax preparer. We have heard of some accountants who tell their clients that if they file the 1040 without itemizing deductions, it is the same as using the short forms. Unfortunately, for financial aid purposes, this is not necessarily true. The federal rules state that you can qualify for the Simplified Needs Test even if you file a 1040, provided you were eligible to file a 1040A or 1040EZ (or you are not required to file a personal tax return) and you meet the income guidelines. However, a representative at the U.S. Department of Education said that this is a “murky area” and that guidelines are still being developed to advise FAOs on how to determine if a family that filed a 1040 was eligible to file a 1040A or 1040EZ (or was not required to file a personal tax return). Since you may have to do a lot of explaining and go through a lot of red tape to convince the FAO (who is not a CPA) that you could have done the short form or were not required to file a personal tax return (and you may not be successful), we recommend that you use the 1040A or 1040EZ if you are eligible to do so (or not file a return at all if you are not required to do so). For your benefit, we have listed the headings of the different returns below so you can identify which are the short forms and which is the long form.

The long form (1040):

Besides the Simplified Needs Test, there is another favorable federal aid loophole known as…

The Automatic Zero-EFC

The federal government has a great break for parent(s) in the household who 1) have a 2015 combined adjusted gross income of $25,000 or less (or if non-tax filers, have combined income from work of $25,000 or less), and 2) can file the 1040A or the 1040EZ tax form (or are not required to file a tax form at all because they are not required to do so).

Note: Prior to the 2012-2013 award year, the income cut-off was considerably higher. However, as part of the December 2011 budget deal by Congress, new legislation reduced the income threshold.

Even if your child has substantial income, or you and your child have substantial assets, the student’s EFC will be judged to be zero if you meet these requirements.

Some accountants encourage retired, disabled, unemployed, or low-income parents to file the long form—which could be troublesome if you otherwise qualify for this break. Many of these parents could file the short form or may not be required to file at all, which will make things much easier when dealing with the FAOs.

Tip #1: There may be some financial aid advantages to filling out the short forms (the 1040A or the 1040EZ) if the IRS permits you to do so. And if you are not required to file a personal tax return but still file a 1040 form, you can still be eligible for the SNT or Automatic Zero-EFC.

Alternate Ways to Qualify

There is an additional way to qualify for the Simplified Need Test (SNT) or the Automatic Zero EFC: if, during the base income year, or the year after the base income year, the student, her parents, or anyone in the parents’ household receives benefits under a means-tested Federal benefit program (other than federal student aid), then they qualify for the Automatic Zero EFC and/or the SNT (provided parental income is below the thresholds mentioned above even if the IRS 1040 is filed). Such benefit programs normally include food stamps, supplemental security income, temporary assistance for needy families (TANF), certain school lunch programs, or certain supplemental nutrition programs for women, infants, and children (WIC).

A dependent student can also qualify for the SNT or Automatic-Zero EFC provided a parent who reports his or her financial information on the FAFSA is considered a “dislocated worker” on the date the FAFSA form is filed (and provided the parental income for the base income year is below the thresholds mentioned above even if the IRS 1040 is filed). A parent can normally qualify for this dislocated worker status by meeting at least one of the following criteria: being laid-off or receiving a lay-off notice from a job; receiving unemployment benefits (due to being laid off or losing a job, provided the person is unlikely to return to their prior occupation); was self-employed but is now unemployed due to economic conditions or natural disaster; or being a “displaced homemaker” (i.e. a stay-at-home mother or father who is no longer supported by their spouse, is unemployed or underemployed, and is having trouble finding or upgrading employment). The financial aid officer at the school will probably require additional documentation to prove such dislocated worker status.

Independent students can also qualify for the SNT and the Automatic-Zero EFC if they meet the same criteria mentioned above, though the Automatic-Zero EFC is not available to a single student or a married independent student without dependents other than a spouse.

A Parents’ Step-by-Step Guide to the Federal Income Tax Form

By reducing your total income (lines 7-21 on the 1040) you can increase your financial aid, which, you should remember, is largely funded by your tax dollars anyway. Let’s examine how various items on your tax return can be adjusted to influence your aid eligibility. The IRS line numbers below refer to the 2015 IRS 1040.

LINE 7—WAGES, SALARIES, TIPS, ETC.

For most parents, there is not much to be done about line 7. Your employers will send you W-2 forms, and you simply report this income. However, there are a few points to be made.

Defer Your Bonus

If you are one of the thousands of Americans in the workplace who receive a bonus, you might discuss with your boss the possibility of moving your bonus into a non-base income year. For example:

If your child is in the beginning of her sophomore year of high school (in other words, if the first base income year has not yet begun) and you are due a year-end bonus, make sure that you collect and deposit the bonus before January 1 of the new year (when the base income year begins). As long as the bonus is included on your W-2 for the previous year, it will not be considered income on your aid application.

The money will still appear as part of your assets (provided you haven’t already spent it). But by shifting the bonus into a non-base income year, you will avoid having the colleges count your bonus twice—as both asset and income.

If you are due a year-end bonus and your child is starting his junior year of high school, see if you can arrange to get the bonus held off until after January 1. Yes, it will show up on next year’s financial aid form, but in the meantime you’ve had the benefit of financial aid for this year.

Just as important, FAOs make four-year projections based on your first base income year. Your FAO will have set aside money for you for the next three years based on the aid your child receives as a freshman in college. Who knows what might happen next year? You might need that money. If the FAO hasn’t already set it aside for you, it might not be there when you need it.

Tip #2: Move your bonus into a non-base income year.

If You’ve Had an Unusually Good Year

Maybe you won a retroactive pay increase during the base income year. Or perhaps you just worked a lot of overtime. If you can arrange to receive payment during a non-base income year that would, of course, be better, but there are sometimes compelling reasons for taking the money when it is offered (for example, you are afraid you might not get it later).

However, unless you explain the details of this windfall to the colleges, they will be under the impression that this sort of thing happens to you all the time.

If the base income year’s income is really not representative, write to the financial aid office of each of the colleges your child is applying to, and explain that this was a once-in-a-lifetime payment, never to be repeated. Include a copy of your tax return from the year before the base income year, or from the year after, which more closely reflects your true average income. If helpful to your cause, you may wish to include a projection of your income for the “current year” - the calendar year that will end on December 31 in the middle of the academic year for which you are seeking aid.

Don’t bother sending documentation like this to the companies that process the standardized analysis forms. They are only interested in crunching the numbers on the form, and anyway have no power to make decisions about your aid at specific schools. Documentation regarding a change in circumstances should never be sent to the processing companies. Send it directly to the schools.

Tip #3: If you’ve had an unusually good year, explain to the colleges that your average salary is much lower.

Become an Independent Contractor

If you are a full-time employee receiving a W-2 form at the end of the year, you have significant unreimbursed business expenses, and you are otherwise ineligible for the SNT or the Automatic Zero-EFC, you might discuss with your employer the viability of becoming an independent contractor. The advantage to this is that you can file your income under schedule C of the tax form (“profit or loss from business”), enabling you to deduct huge amounts of business-related expenses before line 37, where it will do you some good. Note: if you are otherwise eligible for the SNT or Automatic Zero-EFC, filing schedule C will disqualify you from receiving such favorable aid treatment, unless you are not required to file a tax return or are eligible by meeting at least one of the two alternate criteria mentioned on this page.

A regular salaried employee is allowed to take an itemized tax deduction for unreimbursed employee expenses (in excess of 2% of the AGI). Unfortunately, because this deduction comes after line 37, it will have no effect on reducing income under the financial aid formula.

An independent contractor, on the other hand, can deduct telephone bills, business use of the home, dues, business travel, and entertainment—basically anything that falls under the cost of doing business—and thus lower the adjusted gross income.

You would have to consult with your accountant to see if the disadvantages (increased likelihood of an IRS audit, difficulties in rearranging health insurance and pension plans, possible loss of unemployment benefits, increased social security tax, etc.) outweigh the advantages. In addition, the IRS has been known to crack down on employers who classify their workers as independent contractors when they are really salaried employees. Like all fuzzy areas of the tax law, this represents an opportunity to be exploited, but requires careful planning.

Tip #4a: If you have significant unreimbursed employee expenses, consider becoming an independent contractor so that you can deduct expenses on schedule C of the 1040. However, be careful if you are otherwise eligible for the SNT or Automatic Zero-EFC.

Even better, you might suggest to your boss that she cut your pay. No, we haven’t gone insane. By convincing your employer to reduce your pay by the amount of your business expenses, and then having her reimburse you directly for those expenses, you should end up with the same amount of money in your pocket, but you’ll show a lower AGI and therefore increase your aid eligibility.

Tip #4b: If you have significant unreimbursed employee expenses, try to get your employer to reimburse these business expenses directly to you—even if it means taking a corresponding cut in pay.

If your employer won’t let you pursue either of these options, you should be sure to explain your unreimbursed employee expenses in a separate letter to the FAOs.

LINES 8A AND 9A—TAXABLE INTEREST AND DIVIDEND INCOME

If you have interest or dividend income, you have assets. Nothing prompts a “validation” (financial aid jargon for an audit) faster than listing interest and dividend income without listing the assets it came from.

For the most part, there is little you can do, or would want to do, to reduce this income, though we will have a lot to say in later chapters about reducing the appearance of your assets.

Some parents have suggested taking all their assets and hiding them in a mattress or dumping them into a checking account that doesn’t earn interest. The first option is illegal and dumb. The second is just dumb. In both cases, this would be a bit like turning down a raise. More interest is good. The FAOs won’t take all of it, and you will need it if you want to have any chance of staying even with inflation.

The one type of interest income you might want to control comes from Series E and EE U.S. Savings Bonds. When you buy a U.S. Savings Bond, you don’t pay the face value of the bond; you buy it for much less. When the bond matures (in five years, 10 years, or whatever) it is then worth the face value of the bond. The money you receive from the bond in excess of what you paid for it is called interest. With Series E and EE Savings Bonds, you have two tax options: you can report the interest on the bond as it is earned each year on that year’s tax return, or you can report all the interest in one lump sum the year you cash in the bond.

By taking the second option, you can in effect hold savings bonds for years without paying any tax on the interest, because you haven’t cashed them in yet. However, when you finally do cash them in, you suddenly have to report all the interest earned over the years to the IRS. If the year that you report that interest happens to be a base income year, all of the interest will have to be reported on the aid forms as well. This will almost certainly raise your EFC.

The only exception to this might be Series EE bonds bought after 1989. The U.S. government decided to give parents who pay for their children’s college education a tax break: low- or middle-income parents who bought Series EE bonds after 1989 with the intention of using the bonds to help pay for college may not have to pay any tax on the interest income at all. The interest earned is completely tax-free for a single parent making up to $77,550 or a married couple earning up to $116,300. Once you hit these income levels, the benefits are slowly phased out. A single parent earning above $92,550 or a married couple earning above $146,300 becomes ineligible for any tax break. All of these numbers are based on 2016 tax rates and are subject to an annual adjustment for inflation.

However, we still recommend that parents who bought these bonds with the intention of paying for college cash them in after the end of the last base income year (after January 1 of the student’s sophomore year in college). Whether the interest from these bonds is taxed or untaxed, the FAOs still consider it income and assess it just as harshly as your wages.

Thus if at all possible, try to avoid cashing in any and all U.S. Savings Bonds during any base income year. With Series E or EE bonds, you may be able to roll over your money into Series H or HH bonds and defer reporting interest until the college years are over. There is also no law that says you have to cash in a savings bond when it matures. You can continue to hold the bond, and in some instances it will continue to earn interest above its face value.

Tip #5: If possible, avoid cashing in U.S. Savings Bonds during a base income year, unless you’ve been paying taxes on the interest each year, as it accrued.

If You Have Put Assets in Your Other Children’s Names

Parents are often told by accountants to transfer their assets into their children’s name so that the assets will be taxed at the children’s lower rate. While this is a good tax reduction strategy, it stinks as a financial aid strategy, as you will find out later in this chapter. However, if this is your situation and you have already put assets under the student’s younger siblings’ names, there is one small silver lining in this cloud: The tax laws give most parents with children under age 18 (or under age 24 if the child is a full time student for at least 5 months during the tax year) the option of reporting their child’s investment income on a separate tax return or on the parents’ own tax return.

Either way, the family enjoys the benefit of reduced taxes due to the child’s lower bracket. The principal advantage of reporting the child’s income on the parents’ return is to save the expense of paying an accountant to do a separate return.

However, if you are completing your tax returns for a base income year, we recommend that you do not report any of the student’s or student’s siblings’ investment income (i.e. interest, dividends, and capital gains) on your tax return. By filing a separate return for those children, you remove that income from your AGI, and lower your Expected Family Contribution. (We’ll discuss reporting of the student’s income later in this chapter.)

Tip #6: During base income years, do not report children’s investment income on the parents’ tax return. File a separate return for each child.

Leveraged Investments

An important way in which the financial aid formulas differ from the tax code is in the handling of the income from leveraged investments. You leverage your investments by borrowing against them. The most common example of leverage is margin debt. Margin is a loan against the value of your investment portfolio usually made by a brokerage house so that you can buy more of whatever it is selling—for example, stock.

Let’s say you had $5,000 in interest and dividend income, but you also had to pay $2,000 in tax-deductible investment interest on a margin loan. The IRS may allow you to deduct your investment interest expenses from your investment income on schedule A. For tax purposes, you may have only $3,000 in net investment income.

Unfortunately, for financial aid purposes, interest expenses from schedule A are not taken into account. As far as the colleges are concerned, you had $5,000 in income.

Of course you will be able to subtract the value of your margin debt from the value of your total assets. However, under the aid formulas, you cannot deduct the interest on your margin debt from your investment income.

During base income years, you should avoid—or at least minimize—margin debt because it will inflate your income in the eyes of the FAOs. If there is no way to avoid leveraging your investments during the college years, you should at least call the FAO’s attention to the tax-deductible investment interest you are paying. Be prepared to be surprised at how financially unsavvy your FAO may turn out to be. He may not understand the concept of margin debt at all, in which case you will have to educate him. In our experience, we have found that if the situation is explained, many FAOs will make some allowance for a tax-deductible investment interest expense.

Tip #7: During base income years, avoid large amounts of margin debt.

LINE 10—TAXABLE REFUND OF STATE AND LOCAL INCOME TAXES

Many people see their tax refunds as a kind of Christmas club—a way to save some money that they would otherwise spend—so they arrange to have far too much deducted from their paychecks. Any accountant knows that this is actually incredibly dumb. In effect, you are giving the government the use of your money, interest-free. If you were to put this money aside during the year in an account that earned interest, you could make yourself a substantial piece of change.

So Why Does Your Accountant Encourage a Refund?

Even so, many accountants go along with the practice for a couple of reasons. First, they know that their clients are unlikely to go to the bother of setting up an automatic payroll savings plan at work. Second, they know that clients feel infinitely better when they walk out of their accountant’s office with money in their pockets. It tends to offset the large fee the accountant has just charged for his or her services. Third, a large refund doesn’t affect how much tax you ultimately pay. Whether you have your company withhold just the right amount, or way too much, over the years you still end up paying exactly the same amount in taxes.

So accountants have gotten used to the practice, and yours probably won’t tell you (or maybe doesn’t know) that a large refund is the very last thing you want during base income years. Unfortunately, a large refund can seriously undermine your efforts to get financial aid. Here’s why:

If you itemize deductions and get a refund from state and local taxes, the following year you’ll have to report the refund as part of your federal adjusted gross income. Over the years, of course, this will have little or no effect on how much you pay in taxes, but for aid purposes, you’ve just raised your line 37. This might not seem like it could make a big difference, but if you collect an average state and local refund of $1,600 each year over the four college years, you may have cost yourself as much as $3,000 in grant money.

During college years, it is very important to keep your withholding as close as possible to the amount you will actually owe in taxes at the end of the year.

Tip #8: If you itemize your deductions, avoid large state and local tax refunds.

LINE 11—ALIMONY RECEIVED

Even though this may seem like an obvious point, we have found it important to remind people that the amount you enter on this line is not what you were supposed to receive in alimony, but the amount you actually got. Please don’t list alimony payments your ex never made.

In fact, if your ex fell behind in alimony payments, it’s important that you notify the college financial aid offices that you have received less income this year than a court of law thought you needed in order to make ends meet.

By the same token, if you received retroactive alimony payments, you would also want to contact the colleges to let them know that the amount you listed on this line is larger this year than the amount you normally receive. In a situation like this, you might be tempted to put down on the financial aid form only the amount of alimony you were supposed to receive. Please don’t even think about it. Your need analysis information will be checked against your tax return. By the time they’ve finished their audit, and you’ve finished explaining that this was a retroactive payment, all the college’s aid money might be gone.

LINE 12—BUSINESS INCOME

As we mentioned earlier, it can be to your advantage to become an independent contractor if you have large unreimbursed business expenses. A self-employed person is allowed to deduct business expenses from gross receipts on schedule C. This now much smaller number (called net profit or loss) is written down on line 12 of the 1040 form, thus reducing both taxable income and the family contribution to college tuition.

We will discuss running your own business in greater detail in the “Special Topics” chapter of this book; however, a few general points should be made now.

Many salaried people run their own businesses on the side, which enables them to earn extra money while deducting a good part of this income as business expenses. However, before you run out and decide that your stamp collecting hobby has suddenly become a business, you should be aware that the IRS auditors are old hands at spotting “dummy” businesses, and the colleges’ FAOs aren’t far behind.

On the other hand, if you have been planning to start a legitimate business, then by all means, the time to do it is NOW.

Tip #9: Setting up a legitimate business on the side will enable you to deduct legitimate business expenses, and may reduce your AGI.

Just bear in mind that a business must be run with the intention of showing a profit to avoid running afoul of the IRS “hobby loss” provision. The institutional methodology now adds back business losses to your AGI.

LINES 13A AND 14—CAPITAL GAINS OR LOSSES, OTHER GAINS OR LOSSES

When you buy a stock, bond, or any other financial instrument at one price and then sell it for more than you paid in the first place, the difference between the two prices is considered a capital gain. If you sold it for less than you paid in the first place, the difference may be considered a capital loss. We say “may be” because while you are required to report gains on all transactions, the IRS does not necessarily recognize losses on all types of investments.

When you sell an asset, your net worth really stays the same; you are merely converting the asset into the cash it’s worth at that particular instant. However, for tax and financial aid purposes, a capital gain on the asset is considered additional income in the year that you sold your asset.

During base income years, you want to avoid capital gains if you can because they inflate your income. When you sell a stock, not only does the FAO assess the cash value from the sale of the stock (which is considered an asset) but she also assesses the capital gain (which is considered income).

If you need cash it is usually better to borrow against your assets rather than to sell them. Using your stock, or the equity in your house as collateral, you can take out a loan. This helps you in three ways: you don’t have to report any capital gains on the financial aid form; your net assets are reduced in the eyes of the FAO since you now have a debt against that asset; and in some cases, you get a tax deduction for part of the interest on the loan.

Tip #10: If possible, avoid large capital gains during base income years.

However, there may be times when it is necessary to take capital gains. Below you will find some strategies to avoid losing aid because of capital gains. The following are somewhat aggressive strategies, and each would require you to consult your accountant and/or stockbroker:

✵If you have to take capital gains, at least try to offset them with losses. Examine your portfolio. If you have been carrying a stock that’s been a loser for several years, it might be time to admit that it is never going to be worth what you paid for it, and take the loss. This will help to cancel your gain.

✵You can elect to spread your stock losses and gains over several years. One example: The IRS allows you to deduct capital losses directly from capital gains. If your losses exceed your gains, you can deduct up to $3,000 of the excess from other income—in the year the loss occurred. However, net losses over $3,000 are carried over to future years. It might be possible to show net losses during several of the base income years, and hold off on taking net gains until after your kids are done with college.

✵The institutional methodology does not recognize capital losses that exceed gains. However, certain kinds of government aid are awarded without reference to the schools—for example, the Pell Grant and some state-funded aid programs. Because this aid is awarded strictly by the numbers, a capital loss can make a big difference. (Consult your state aid authorities and the individual schools to see how capital losses will be treated.)

✵If you are worried about falling stock prices but don’t want to report a capital gain, you should consult your stockbroker. There may be ways to lock in a particular price without selling the stock.

✵If you have any atypically large capital gain in a base income year that you must report on an aid form, you should write to the colleges explaining that your income is not normally so high.

The Sale of Your Home

The Taxpayer Relief Act of 1997 changed the way capital gains from the sale of a primary residence are treated. For any sale after May 6, 1997 you are permitted to exclude up to $250,000 in capital gains every two years on the sale of your home (up to $500,000 for a married couple filing jointly). To qualify, the home must have been your primary residence that you owned and occupied for at least two of the last five years prior to the sale. Any gains in excess of the exclusion limits would, of course, be subject to income taxes.

Representatives at the Department of Education and the College Board have stated that only gains above the excludable amounts need to be reported on the aid forms, since they are then part of your Adjusted Gross Income. If you sold your home and must complete the aid forms before you purchase another property, you’ll need to report the money you have from the sale as part of your assets on the aid forms. However, you should be sure to write a letter to the FAOs explaining that you will no longer have those assets once you purchase another property, if that is the case.

LINE 15—IRA DISTRIBUTIONS

This line on the 1040 form covers any withdrawals (called “distributions” by the IRS) made during the year from Individual Retirement Accounts (IRAs). Most financial planning experts advise against early withdrawals before retirement since one of the biggest benefits of an IRA is the tax-deferred compounding of investment income while the funds are in the account. In many cases, early withdrawals will trigger a 10% penalty (if you took out the funds before age 59 1/2) and you’ll have to pay income taxes on part or all of the money withdrawn. (Which part of the withdrawal will be subject to income taxes will depend on whether your prior IRA contributions were deductible or not.)

If that is not enough bad news to discourage you, consider the financial aid implications. Any IRA withdrawal during a base income year will raise your income in the financial aid formulas thereby reducing aid eligibility. The part of the withdrawal that is taxable will raise that all-important line 37 on your tax return; the portion that is tax-free will also affect your EFC, since the aid formulas assess untaxed income as well.

To demonstrate the negative impact of an early IRA withdrawal, let’s look at an example of a parent, age 55, who took funds out of an IRA during the first base income year. The family is in the 25% federal tax bracket and since all prior IRA contributions were tax deductible, the withdrawal will be fully taxable. After subtracting the early withdrawal penalties, income taxes, and reduced aid eligibility, there will be only about 35 cents on the dollar left. Get the point? Early withdrawals from IRAs should be avoided at all costs.

A legitimate rollover of an IRA (when you move your money from one type of IRA investment into another within 60 days) is not considered a withdrawal. You do have to report a rollover to the IRS on the 1040 form, but it is not subject to penalties (so long as you stick to the IRS guidelines) nor is it considered income for financial aid purposes.

Tip #11: Try to avoid IRA distributions during base income years.

Parents sometimes ask whether it is possible to borrow against the money in their IRAs. You are not allowed to borrow against the assets you have in an IRA. The IRS calls this a “prohibited transaction.”

Note: The Taxpayer Relief Act enacted in August 1997 provides for penalty-free distributions from IRAs after December 31, 1997 if the funds are used to pay for qualified educational expenses (tuition, fees, books, supplies, room and board for the undergraduate or graduate studies of the taxpayer, taxpayer’s spouse, or taxpayer’s child or grandchild). The words “penalty-free” only apply to the 10% early withdrawal penalty. As such, you should not assume that you will not be penalized in the financial aid process or that you will not owe any income taxes if you withdraw funds for qualified education expenses.

The Act also provides taxpayers the opportunity to convert an existing IRA into a Roth IRA, provided certain criteria are met. The major benefit of this type of IRA is the fact that almost all withdrawals from a Roth IRA after age 59 1/2 will be totally tax-free. While the 10% early withdrawal penalty will not apply to this conversion, income taxes must be paid on the entire amount converted unless part of the account represents prior contributions to a non-deductible IRA. If you converted your IRA into a Roth IRA in 2015 you must report this conversion as part of line 15a or 15b on the IRS 1040, thereby raising your income and your EFC in the aid formulas. However, it is important to notify the financial aid offices about any such conversion since the U.S. Department of Education has granted colleges the ability to adjust the family contribution for this unusual transaction. (We’ll discuss the IRAs and Roth IRAs in more detail in Chapter Ten.)

If You’ve Just Retired

As people wait until later in life to have children, it is becoming more commonplace to see retirees with children still in college. If you have recently retired and are being forced to take distributions from traditional IRAs, we suggest that you pull out the minimum amount possible. The government computes what this minimum amount should be based on your life expectancy (the longer you’re expected to live, the longer they are willing to spread out the payments). Because it turns out that the average American’s life expectancy is higher at 66 than it is at 65, it pays to get them to recalculate your minimum distribution for each year your child is in college. Obviously, if you need the money now, then you should take it. But try to withdraw as little as possible, since IRA distributions increase your income and thus reduce financial aid.

Note: You are not required to take distributions from Roth IRAs regardless of your age.

LINE 16—PENSIONS AND ANNUITIES

The same is true of pension distributions. Sometimes it is possible to postpone retirement pensions or roll them over into an IRA. If you can afford to wait until your child is through college, you will increase your aid eligibility. The money isn’t going anywhere, and it’s earning interest.

Note: Any unusually large or early distributions from IRAs or pensions should be explained to the college financial aid offices. Any “rollovers” should also be explained when you submit a copy of your taxes to the school. Since you must include “rollovers” as part of the amount you list on line 15a or 16a of the IRS 1040, some FAOs have been known to incorrectly assume that the family received the funds, but failed to report this untaxed income on the aid forms. If they make this error, the EFC they determine will be much higher than it should be.

LINE 17—RENTS, ROYALTIES, ESTATES, PARTNERSHIPS, TRUSTS, AND LINE 18—FARM INCOME

Like schedule C income, items coming under these categories are computed by adding up your gross receipts and then subtracting expenses, repairs, and depreciation. Be especially thorough about listing all expenses during base income years.

If you have a summer house or other property, you may have been frustrated in the past, because costly as it is to operate a second home, you haven’t been able to deduct any of these expenses. You could consider renting it out while your son or daughter is in college. The extra income might be offset (perhaps significantly) by the expenses that you’ll now be legitimately able to subtract from it. By changing how interest expense and real estate taxes are reflected on your tax return (from an itemized deduction on schedule A to a reduction of rental income on line 17) you reduce the magical AGI. There are special tax considerations for “passive loss” activities and recapture of depreciation, so be sure to consult your advisor before proceeding with this strategy, and remember that many private colleges and a few state schools will not recognize losses of this type when awarding institutional funds since the institutional methodology adds back losses to income.

LINE 19—UNEMPLOYMENT COMPENSATION

If you are unemployed, benefits received during the base income year are considered income under the aid formula. However, some special consideration may be granted to you. We will discuss this in more detail under the “Recently Unemployed Worker” heading in Chapter Nine.

LINES 20A AND B—SOCIAL SECURITY BENEFITS

Total social security benefits are listed on line 20a. The taxable portion of those benefits is listed on line 20b. Whether you have to pay tax on social security benefits depends on your circumstances. Consult the instructions that come with your tax return. For some parents who have other income, part of the social security benefits received may be taxable.

LINE 21—OTHER INCOME

Any miscellaneous income that did not fit into any of the other lines, goes here. Some examples: money received from jury duty or from proctoring SAT exams, extra insurance premiums paid by your employer, gambling winnings.

Gambling winnings present their own problem. The IRS allows you to deduct gambling losses against winnings. However the deduction can, once again, only be taken as part of your itemized deductions on schedule A. Since this happens after line 37, it is not a deduction as far as the need analysis computer is concerned.

Since gambling losses are not likely to provoke much sympathy in the FAOs, we don’t think there would be any point to writing them a letter about this one. During the college years, you might just want to curtail gambling.

This is the last type of taxable income on the 1040, but don’t start jumping for joy yet. The colleges are interested in more than just your taxable income.

Untaxed Income

We’ve just looked at all the types of income that the IRS taxes, and discussed how the financial aid process impacts on it. There are several other types of income that the IRS doesn’t bother to tax. Unfortunately, the colleges do not feel so benevolent. While the IRS allows you to shelter certain types of income, the colleges will assess this income as well in deciding whether and how much financial aid you receive.

Here are the other types of income the need analysis forms will ask you to report, and some strategies.

Untaxed Social Security Benefits

Any social security benefits that are not taxable are defined as “untaxed social security benefits” in the financial aid regulations. Untaxed social security benefits (as well as certain other untaxed income items that years ago were previously assessed as income in the Federal Methodology) do not need to reported as untaxed income on the FAFSA. Such excluded untaxed social security benefits could include any untaxed benefits paid for the student (whether such benefits are paid to the student directly or paid to the parent for the benefit of the student), untaxed benefits paid to a parent for other children, or the untaxed portion of any social security benefits paid for the benefit of the parent(s) themselves. Depending on other income received by the parents during the year, a parent’s own social security benefits may be fully tax-free or partially tax-free. Since any taxable social security benefits are part of the Adjusted Gross Income, they will continue to be assessed in the federal formula and the institutional formula.

Since the social security benefits for most students normally end before the student starts college (and are normally tax-free), the Institutional Methodology has excluded any untaxed social security benefits received for the student from untaxed income for a number of years. However, untaxed benefits paid to a parent for children other than the student and/or the untaxed portion of any social security benefits received by the parent(s) themselves will continue to be assessed in the IM.

We’ll discuss social security benefits in greater detail in Part Three, “Filling Out the Standardized Forms.”

Payments Made into IRAs, Keoghs, 401(k)s, 403(b)s, and TDAs

IRAs (Individual Retirement Accounts), Keoghs, 401(k)s, 403(b)s, and TDAs (short for Tax Deferred Annuities) are all retirement provisions designed to supplement or take the place of pensions and social security benefits. The tax benefit of these plans is that in most cases they allow you to defer paying income tax on contributions until you retire, when presumably your tax bracket will be lower. The investment income on the funds is also allowed to accumulate tax-deferred until the time you start to withdraw the funds.

The 401(k) and 403(b) plans are supplemental retirement provisions set up by your employer in which part of your salary is deducted (at your request) from your paycheck and placed in a trust account for your benefit when you retire. Some companies choose to match part of your contributions to the plans. Keoghs are designed to take the place of an ordinary pension for self-employed individuals. TDAs fulfill much the same purpose for employees of tax-exempt religious, charitable, or educational organizations.

IRAs are supplemental retirement provisions for everyone. Contributions to these plans are tax-deductible in many cases. For example, if an unmarried individual is not covered by a retirement plan at work or a self-employed retirement plan, she can make tax-deductible contributions to an IRA of up to $5,500 (up to $6,500 if age 50 or older) regardless of her income level. If a person is covered by a retirement plan, his contribution to an IRA may or may not be tax-deductible, depending on his income level.

Note: The tax bills enacted in August 1997 and June 2001 involve many changes to the IRA rules. Before making any new contributions, withdrawals, or changes to an IRA, you should be sure to consult IRS Publication 590 for the corresponding tax year (it covers the IRA regulations and is free from Uncle Sam), or seek the advice of a qualified professional who is familiar with the tax laws as well as the financial aid regulations.

Financial Aid Ramifications of Retirement Provisions

Retirement provisions are wonderful ways to reduce your current tax burden while building a large nest egg for your old age—but how do they affect financial aid?

The intent of current financial aid laws is to protect the money that you have built up in a retirement provision. Assets that have already been contributed to IRAs, Keoghs,

401(k)s, and so on by the date you fill out the standardized aid form do not have to appear on that form. In most cases, the FAOs will never know that this money exists. Thus loading up on contributions to retirement provisions before the college years begin makes enormous sense.

However, any tax-deductible contribution that you make into these plans voluntarily during the base income years is treated just like regular income. The IRS may be willing to give you a tax break on this income, but the FAOs assess it just like all the rest of your income, up to a maximum rate of 47%. Deductible contributions made to retirement provisions during base income years will not reduce your income under the aid formula. If you can still afford to make them, fine. Most parents find they need all their available cash just to pay their family contribution. Contributions to Roth IRAs or non-deductible Traditional IRAs are not considered untaxed income since they do not reduce your AGI.

These plans remain an excellent way of protecting assets. Try to contribute as much as you can before the first base income year. Parents sometimes ask us how colleges will know about their contributions to 401(k) or 403(b) plans, or to tax-deferred annuities. These contributions usually show up in boxes 12a-d of your W-2 form, codes D, E, F, G, H, and S. Don’t even think about not listing them.

A possible exception to this scenario would come up if contributions to these plans would reduce your income below the $50,000 AGI cut-off for the simplified needs test. For example, let’s say your total salary from work is $45,000, your only other income is $7,000 in interest income (from $500,000 in assets you have parked in Certificates of Deposit) and you don’t itemize your deductions. By deferring $2,500 for the year into a 401(k) plan, your adjusted gross income will now be $49,500, and your untaxed income will be $2,500—making you potentially eligible for the simplified needs test which will exclude your assets from the federal formula. Had you not made the contribution to the 401(k) plan, your AGI would be $52,000 and your assets would be assessed (at up to 5.65% per year for parental assets, and 20% per year for student assets).

Tax-Exempt Interest Income

Even though the government is not interested in a piece of your tax-free investments, the colleges are. Some parents question whether there is any need to tell the colleges about tax-free income if it does not appear on their federal income tax return.

In fact, tax-free interest income is supposed to be entered on line 8b of the 1040. This is not an item the IRS tends to flag, but there are excellent reasons why you should never hide these items. For one thing, tax law changes constantly. If your particular tax-free investment becomes taxable or reportable next year, how will you explain the sudden appearance of substantial taxable interest income? Or what if you need to sell your tax-free investment? You will then have to report a capital gain, and the FAO will want to know where all the money came from.

More Untaxed Income

Other untaxed income that is included in the federal financial aid formula includes but is not limited to the tax-free portion of any pensions or annuities received (excluding rollovers), the tax-free portion of IRA distributions (excluding rollovers), child support received, workers’ compensation, veterans noneducation benefits, the Health Savings Account (HSA) deduction (IRS 1040 Line 25), and living allowances paid to members of the military and clergy. Some other categories of untaxed income (for example, untaxed disability benefits) will need to be reported on the FAFSA form as well. There is little to do about this kind of income except write it down. As with alimony, child support reported should include only the amount you actually received, not what you were supposed to receive.

Note: The federal methodology excludes contributions to, or payments from, flexible spending arrangements. The institutional methodology will consider pre-tax contributions withheld from wages for dependent care, medical spending, and HSA accounts as part of untaxed income for the 2017-2018 award year. But along with the HSA deduction, schools will have the opportunity to exclude them. The tuition and fees deduction (IRS 1040 line 34, see this page) will still be considered untaxed income (but only in the institutional methodology). In addition, the following types of untaxed income (which previously were assessed in the federal formula, but are now not considered in the FM) will continue to be considered part of untaxed income in the IM: the earned income credit (IRS 1040 line 66a), the additional child credit (IRS 1040 line 67), welfare benefits, the credit for federal tax on special fuels, and the foreign income exclusion.

EXPENSES

After adding up all your income, the need analysis formulas provide a deduction for some types of expenses. A few of these expenses mirror the adjustments to income section of the 1040 income tax form. Many parents assume that all the adjustments to income from the IRS form can be counted on the standardized financial aid forms. Unfortunately this is not the case. Likewise, many parents assume that all of the itemized tax deductions they take on schedule A will count on the financial aid forms as well. Almost none of these are included in the financial aid formula. Let’s look at adjustments to income first.

Expenses According to the IRS: Adjustments to Income

LINE 23—EDUCATOR EXPENSES

This adjustment to income involves educators in both public and private elementary and secondary schools who work at least 900 hours during a school year as a teacher, instructor, counselor, principal, or aide and who have certain qualifying out-of-pocket expenses. The maximum deduction for this item is $250 per taxpayer, and there are other criteria you need to meet. Prior to this item appearing on the 1040 form, educators could only take such expenses as part of miscellaneous itemized deductions on schedule A of the 1040. If allowable, it is to your advantage to take the deduction as an adjustment to income, rather than lump it with all your other miscellaneous deductions on schedule A. First, because it would reduce your AGI and EFC, and second, because it would be a sure tax deduction if offered. If your total miscellaneous deductions do not exceed a certain percentage of your AGI or you do not itemize, you won’t get a deduction for those expenses at all on your taxes.

LINE 26—MOVING EXPENSES

Job-related moving expenses are deductible as an adjustment to income. Years ago, these expenses could be taken only as part of your itemized deductions, and did not affect your aid eligibility. Since this item will both reduce your tax liability and potentially increase your aid eligibility, you should be sure to include all allowable moving expenses. There have been some recent changes to the tax law regarding what constitutes a moving expense (for example, pre-move house hunting trips are no longer deductible) so be sure to read the IRS instructions or consult a competent advisor.

LINE 27—DEDUCTIBLE PART OF SELF-EMPLOYMENT TAX

Self-employed individuals can deduct one half of the self-employment taxes they pay. The federal and institutional formulas take this deduction into account.

LINES 28 AND 32—IRA DEDUCTIONS AND SELF-EMPLOYED SEP, SIMPLE, AND QUALIFIED PLANS DEDUCTIONS

As we explained above, while these constitute legitimate tax deductions, contributions to deductible IRAs, SEPs, KEOGHs, and other plans that can be deducted on Line 28 or Line 32 will not reduce your income under the FM or IM aid formulas.

However, some forms of state aid (which do not use the federal methodology employed by the colleges themselves) may be boosted by contributions to retirement plans that reduce your AGI as some state programs are based solely on taxable income. We’ll discuss this in detail in Chapter Six, “State Aid.” As we mentioned earlier, contributions to an IRA could lower your AGI below the $50,000 cap for the Simplified Needs Test. Individuals who make contributions to plans that are deducted on Line 28 are either self-employed or a partner and therefore cannot meet the Simplified Needs Test.

LINE 29—SELF-EMPLOYED HEALTH INSURANCE DEDUCTION

This is another adjustment to income recognized by the FAO. If you are self-employed or own more than 2% of the shares of an S corporation, there are two places on the 2015 IRS 1040 form where you may be able to take medical deductions. On line 29, you can now deduct 100% of your qualifying health insurance premiums. It is to your advantage to take the deduction here, rather than lump it with all your other medical expenses on schedule A. First, because it will reduce your AGI, and second, because it is a sure deduction here. If your total medical expenses do not add up to a certain percentage of your total income, you won’t get a deduction for medical expenses at all on your taxes. In addition, high medical expenses (other than those included here on line 29) are no longer an automatic deduction in the federal aid formula as they were prior to the 1993-94 school year. We’ll describe this in detail, under “Medical Deduction” on this page.

LINE 30—PENALTY ON EARLY WITHDRAWAL OF SAVINGS, AND LINE 31A—ALIMONY PAID

If you took an early withdrawal of savings before maturity, which incurred a penalty and/or you paid out alimony, these amounts will be claimed here. The FM and IM aid formulas grant you a deduction for these two adjustments to income as well.

LINE 33—STUDENT LOAN INTEREST DEDUCTION

The Taxpayer Relief Act of 1997 created this adjustment to income. This can involve loans used to cover your own post-secondary educational expenses as well as those of your spouse or any other dependent at the time the loan was taken out. We’ll discuss more of the fine print in Chapter Ten. You should realize that any deduction claimed here will reduce your income under both the federal and the institutional formulas.

LINE 34—TUITION AND FEES DEDUCTION

With this deduction, you may be able to claim up to $4,000 in qualified higher education expense even if you don’t itemize deductions on your income tax return provided your income is low enough and you meet other criteria. Be aware that you can not claim this deduction if you claim the Hope, American Opportunity, or Lifetime Learning credits (see Chapter Ten) for the same student in the same tax year. Withdrawals from Coverdell ESAs and Section 529 plans as well as the claiming of tax-free interest from the sale of U.S. savings bonds can also affect this deduction so you’ll need to carefully read (or have your accountant carefully read) the tax return instructions. This deduction would reduce your income in the federal financial aid formula. For the institutional formula, this deduction is added back to income as part of your untaxed income.

LINE 24—CERTAIN BUSINESS EXPENSES OF RESERVISTS, PERFORMING ARTISTS, AND FEE-BASIS GOVERNMENT OFFICIALS; LINE 35—DOMESTIC PRODUCTION ACTIVITIES DEDUCTION; OTHER WRITE-IN ADJUSTMENTS NOT REPORTED ON LINES 23-35, BUT INCLUDED AS PART OF LINE 36

While each of these adjustments to income will lower your AGI—and therefore your EFC—they are not applicable for the vast majority of tax filers.

Other Expenses According to the Financial Aid Formula

You’ve just seen all the adjustments to income that the IRS allows. The colleges allow you a deduction for several other types of expenses for financial aid purposes as well:

Federal Income Tax Paid

The advice we are about to offer may give your accountant a heart attack. Obviously, you want to pay the lowest taxes possible, but timing can come into play during the college years. The higher the taxes you pay during a base income year, the lower your family contribution will be. This is because the federal income taxes you pay count as an expense item in the aid formula. There are certain sets of circumstances when it is possible to save money by paying higher taxes.

The principle here is to end up having paid the same amount of taxes over the long run, but to concentrate the taxes into the years the colleges are scrutinizing, thus increasing your aid eligibility.

Let’s look at a hypothetical example. Suppose that you make exactly the same amount of money in two separate years. You are in the 25% income tax bracket, and the tax tables don’t change over these two years. Your federal tax turns out to be $6,000 the first year and $6,000 the second year, for a total tax bill of $12,000 for the two years.

Let’s also suppose that you decide to make an IRA contribution during only one of the two years, but you aren’t sure in which year to make the contribution. You’re married, 52 years old, and neither of you is covered by a pension plan at work, so you are able to make a tax-deductible IRA contribution of $6,500. This turns out to reduce your federal taxes by $1,625 for the year in which you make the contribution. Since, in this case, your tax situation is precisely the same for both years, it doesn’t make much difference in which year you take the deduction.

|

$12,000 |

total taxes over 2 years (if no IRA contribution made) |

|

|

- $ 1,625 |

tax savings for IRA contribution |

|

|

$10,375 |

total taxes for the 2 years |

Over the two years, either way, you end up paying a total of about $10,500 in federal taxes.

It’s All a Matter of Timing

Here’s where timing comes in. What if the second of the two years also happens to be your first base income year? In this case, you’re much better off making the contribution during the previous year. By doing so, as we’ve already explained, you shelter the $6,500 asset from the need analysis formula, and get a $1,625 tax break in the first year.

But much more important, by making the contribution during the first year, you choose to pay the higher tax bill in the second year—the base income year—which in turn lowers your Expected Family Contribution. Over the two years, you’re still paying close to the same amount in taxes, but you’ve concentrated the taxes into the base income year where it will do you some good.

Tip #12: Concentrate your federal income taxes into base income years to lower your Expected Family Contribution.

Obviously, if you can afford to make IRA contributions every year, you should do so; building a retirement fund is a vital part of any family’s long-term planning. However, if like many families, you find that you can’t afford to contribute every year during college years, you can at least use timing to increase your expenses in the eyes of the FAOs. By loading up on retirement provision contributions during non-base income years, and avoiding tax-deductible retirement contributions and other tax-saving measures during base income years, you can substantially increase your aid eligibility.

The above example assumed that tax rates would be the same from year to year. Should tax rates change from one year to the next, you will need to balance your tax planning with your financial aid planning to determine the best course of action

Charitable Contributions

Large donations to charity are a wonderful thing, both from a moral standpoint and a tax standpoint—but not during a base income year. When you lower your taxes, you raise your family contribution significantly. We aren’t saying you should stop giving to charity, but we do recommend holding off on large gifts until after the base income years.

Extra Credits

When you are asked questions about U.S. income taxes paid on the FAFSA, the government and the colleges are not interested in how much taxes you had withheld during the year, or whether or not you are entitled to a refund. Instead, they are interested in your federal income tax liability after certain tax credits are deducted, which happens to be the amount of line 56 minus line 46 on the 2015 IRS 1040 form. While most tax credits that you claim will eventually reduce your aid eligibility (since lower taxes mean lower expenses against income in the formulas), the tax benefits from these credits will be much greater than the amount of aid that is lost. As such, you should be sure to deduct any and all tax credits that you are entitled to claim on your tax return.

Be aware that under the federal formula, any education tax credits claimed (such as the Hope Scholarship Credit and the Lifetime Learning Credit) will not reduce aid eligibility. While any nonrefundable education credits claimed - for 2015, these would be claimed on line 50 of the IRS Form 1040 - will reduce the amount of U.S. income taxes paid, they will also be considered an “exclusion from income”, which in aid speak means a deduction against income. So in effect, any education credits claimed will reduce expenses and income by an equal amount, thereby allowing families and students the full benefit of the Hope Credit, the American Opportunity Credit, or the Lifetime Learning Credit. (Later in Chapter Ten, we’ll discuss some strategies to insure you get the maximum credits allowed by law; for now, we just want to focus on their aid impact.)

Unfortunately, the institutional formula has not been as benevolent. Since the nonrefundable education credits are not considered an exclusion against income, any amounts nonrefundable credits claimed will partially reduce aid eligibility. However, the College Board will give colleges the option of having any refundable education credits added back to the amount of U.S. income taxes paid, so that any impact on aid will be negligible.

Currently, the Federal Methodology reduces the amount of U.S taxes paid (reported on Line 56 of the 2015 1040) by the amount of any excess advance premium tax credit reported on line 46 of the return. And we went to press, the College Board had not yet decided for the IM if they would use the amount on line 56 of the 1040 for this item—or if they would mirror the FM and deduct any amount on line 46 from the line 56 amount. (For the IRS 1040A, the amount of the taxes paid reported on Line 37 is reduced by line 29.)

Both the FM and IM do not consider any refundable portion of the American Opportunity Credit to be untaxed income. These would be claimed on Line 68 of the 2015 IRS 1040 or Line 44 of the 1040A. A nonrefundable credit can only be claimed if a taxpayer has income tax liability, while a refundable credit can be claimed even if the taxable income is so low that there is no resulting income tax liability.

The Alternative Minimum Tax

Until recently, those families who were subject to the Alternative Minimum Tax were actually penalized in the aid formulas—for while they had to pay the tax, the formulas did not take this additional tax into account. The Alternative Minimum Tax (AMT) is an additional tax that is incurred if certain deductions or tax credits reduce the amount of U.S. income taxes paid below a certain level. Many of our readers don’t have to worry about the AMT since it usually impacts more individuals in the top income tax brackets.

But we have good news for those few readers who must pay the AMT. Federal income taxes paid in the financial aid formulas currently includes any Alternative Minimum Tax liability. This will generally reduce the EFC in both the federal and institutional methodologies for those subject to the AMT, since the amount of federal income taxes paid is a deduction against income in the formulas.

Deduction for Social Security and Medicare Taxes

The financial aid formulas give you a deduction for the Medicare and social security taxes (otherwise known as FICA) that you pay. Parents often ask how the colleges do this since there doesn’t seem to be a question about social security taxes on the financial aid forms. The deduction is actually made automatically by computer, but it is based on two questions on the financial aid form. These questions are in disguise.

On the FAFSA and the PROFILE, the two questions are “father’s income earned from work,” and “mother’s income earned from work.” At first glance these questions appear to be about income. In fact, for tax filers these are expense questions. If you minimize the amounts you put down here, you may cost yourself aid.

Therefore, you should be sure to include all sources of income from work on which you’ve paid FICA or Medicare taxes: wages (box 1 of your W-2), income from self-employment (line 12 of the 1040), income from partnerships subject to self-employment taxes (not including income from limited partnerships), deferred compensation (tax-filers only), and combat pay (for servicemen and servicewomen).

A Financial Aid Catch-22

Wages that you defer into a 401(k), 403(b), or other retirement plan are not subject to income tax by the IRS, but you still pay social security taxes and/or Medicare taxes on them. (Currently, income above $118,500 is exempt from FICA. However, there is no income ceiling on Medicare taxes.)

The strange thing is that, while the purpose of the questions regarding income earned from work on the financial aid forms is to allow the need analysis companies to calculate the social security and Medicare taxes you paid, the instructions for the forms don’t tell you to include deferred income. For example, if your income was $40,000 last year and you deferred $5,000 of it into a 401(k), the instructions tell you to put down $35,000 as your income from work.

Welcome to the Wacky World of Financial Aid

The instructions are wrong. It’s just that simple. Other aid professionals agree with us. So please ignore the instructions. If you contributed any pre-tax wage income (subject to Social Security and/or Medicare taxes) into tax-deferred retirement accounts, include it as part of the question on income earned from work on the FAFSA.

Will this make a real difference to your aid package? It depends on how much you defer. Say you and your spouse defer $5,000 each, and you are in the 47th percentile in aid assessment. By including this money as part of income earned from work, you could increase your aid eligibility by about $380 per year.

This might seem petty, but these small amounts—$380 here, $200 there—can add up. Put another way, this is $380 a year ($1,520 over four years) that you may not have to borrow and pay interest on.

Note: There are two situations when you should not include your tax-deferred contributions to retirement plans as part of income earned from work. If you do not file a tax return, your income earned from work will be treated as an income item when the data is processed. Since you must also include such contributions as untaxed income on the forms, your income will be overstated in this situation. You should also avoid adding such contributions to your income earned from work if this would disqualify you from otherwise meeting all the criteria for the Simplified Needs Test or the Automatic Zero-EFC (see this page).

State and Local Tax Allowance

This is another calculation that is done automatically by the need assessment computer. The computer takes the sum of your taxable and untaxable income and multiplies it by a certain percentage based on the state you live in to determine your deduction. The formula for each state is slightly different. (See Table 8.)

This works very well for people who live and work in the same state, but presents real problems for everyone else. If you live in one state but work in another where the taxes are higher, you may be paying more in taxes than the formula indicates. The financial need computer isn’t programmed to deal with situations like this, and people who don’t fit the program get penalized.

The only way to deal with this is to write to the individual colleges’ aid offices to let them know about your special situation.