Paying for College Without Going Broke, 2017 Edition - Princeton Review, Kalman Chany (2016)

Part I. Understanding the Process

Chapter 1. Overview

How the Aid Process Works: Paying for College in a Nutshell

Ideally, you began this process many years ago when your children were quite small. You started saving, at first in small increments, gradually increasing the amounts as your children got older and your earning power grew. You put the money into a mixture of growth investments like stock funds, and conservative investments like treasury bonds, so that now as the college years are approaching you are sitting pretty, with a nice fat college fund, a cool drink in your hand, and enough left over to buy a vacation home in Monte Carlo.

However, if you are like most of us, you probably began thinking seriously about college only a few years ago. You have not been able to put away large amounts of money. Important things kept coming up. An opportunity to buy a home. Taxes. Braces. Soccer camp. Taxes.

If you are foresighted enough to have bought this book while your children are still young, you will be especially interested in our section on long-term planning. If your child is already a senior in high school just about to apply for college, don’t despair. There is a lot you can do to take control of the process.

Most people cannot afford to pay the full cost of four years of college. Financial aid is designed to bridge the gap between what you can afford to pay for school and what the school actually costs. Parents who understand the process come out way ahead. Let’s look at the aid process in a nutshell and see how it works—or at least how it’s supposed to work. Later on, we will take you through each step of this process in greater detail.

The Standardized Need Analysis Forms

While students start work on their admissions applications, parents should be gathering together their records in order to begin applying for financial aid.

At a minimum, you need to fill out a standardized need analysis form called the Free Application for Federal Student Aid (FAFSA). This form, which is available in either a paper version, a PDF version, or an online version, can be filled out only after January 1 of the student’s senior year in high school.

Many private colleges and some state-supported institutions may require you to electronically complete the CSS/Financial Aid PROFILE Form as well. This form is developed and processed by the same organization that brings you the SAT—The College Board.

A few schools will require other forms as well—for example, the selective private colleges often have their own financial aid forms. Graduate and professional school students might also have to complete a Need Access Application, which is a form developed by the Access Group in Wilmington, Delaware. To find out which forms are required by a particular college, consult the individual school’s financial aid office website or printed information. All of the forms ask the same types of questions.

These questions are invasive and prying. How much did you earn last year? How much money do you have in the bank? What is your marital status? A hundred or so questions later, the need analysis company will have a very clear picture of four things:

1. the parents’ available income

2. the parents’ available assets

3. the student’s available income

4. the student’s available assets

The processor of the FAFSA form uses a federal formula (called the federal methodology) to decide what portion of your income and assets you get to keep and what portion you can afford to put toward college tuition this year. This amount is called the Expected Family Contribution (EFC), and will most likely be more than you think you can afford.

However, some schools do not feel that the EFC generated by the FAFSA gives an accurate enough picture of what the family can contribute to college costs. Using the supplemental information on the PROFILE (which is analyzed using a formula called the institutional methodology that is developed by the College Board) and/or using their own individual forms, these institutions perform a separate need analysis to determine eligibility for aid that those schools control directly.

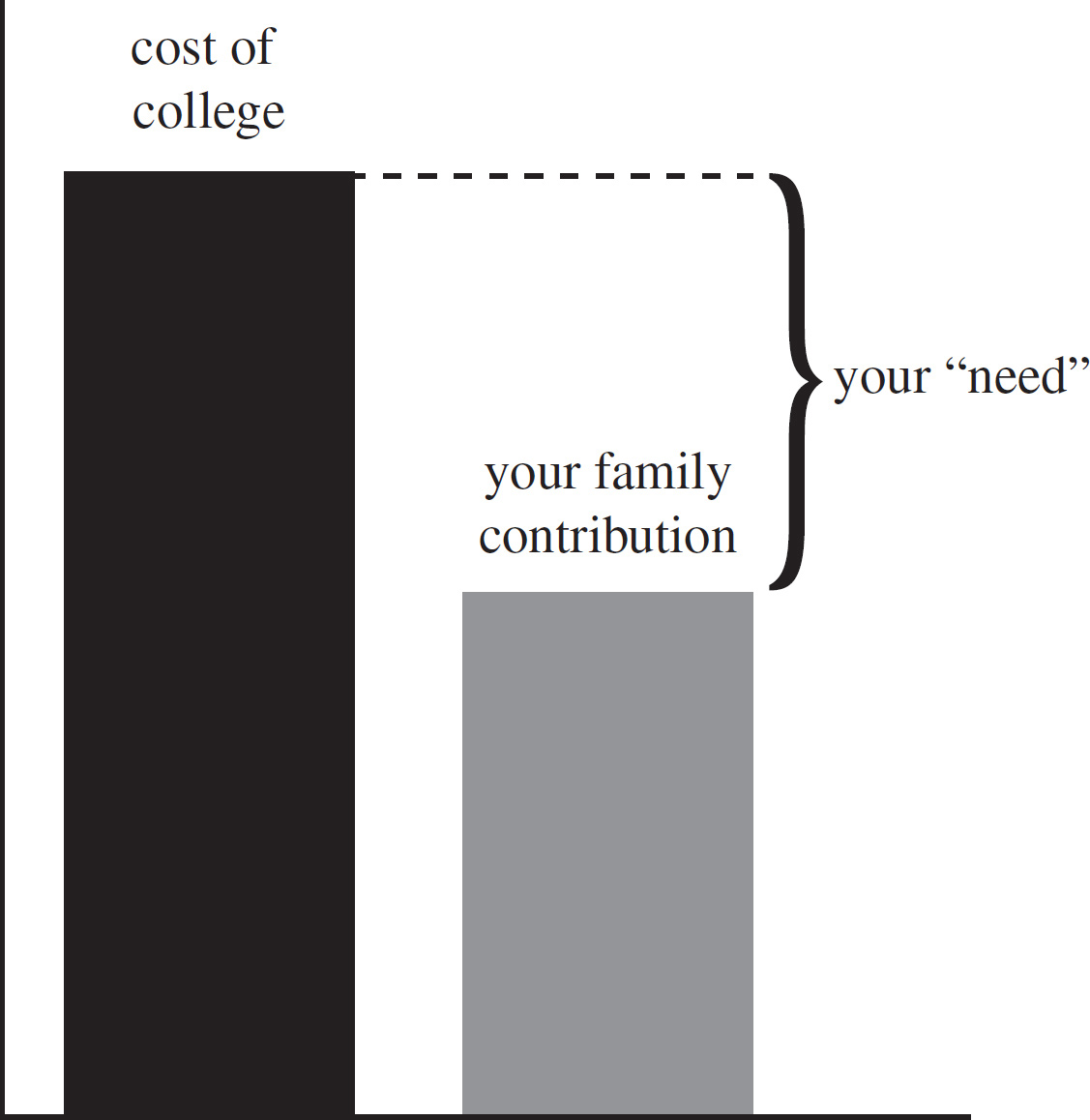

A Family’s “Need”

Meanwhile, the admissions offices of the different colleges have been deciding which students to admit and which to reject. Once they’ve made their decision, the financial aid officers (known as FAOs) get to work. Their job is to put together a package of grants, work-study, and loans that will make up the difference between what they feel you can afford to pay and what the school actually costs. The total cost of a year at college includes:

tuition and fees

room and board

personal expenses

books and supplies

travel

The difference between what you can afford to pay and the total cost of college is called your “need.”

In theory, your Expected Family Contribution will be approximately the same no matter what schools your child applies to. If your EFC is calculated to be $20,300 and your child is accepted at a state school that costs $25,300, you will pay about $16,300, and the school will make up the difference—in this case $5,000—with an aid package. If you apply to a prestigious Ivy League school that costs $70,000, you will still pay about $20,300 and the school will make up the difference with an aid package of approximately $49,700.

In theory, the only difference between an expensive school and a cheaper school (putting aside subjective matters like the quality of education) is the amount of your need. In some cases, depending on how badly the college wants the student, parents won’t pay a penny more for an exclusive private college than they would for a state school.

This is why families should not initially rule out any school as being too expensive. The “sticker price” doesn’t necessarily matter; it’s the portion of the sticker price that you have to pay that counts. Parents are often under the impression that no matter what type of school their child attends—be it a very expensive private college, an expensive out-of-state public institution, or their local state university—they will receive the same amount of aid. In fact, as you saw from the previous example, the amount of aid you get is in part determined by the cost of the school you choose.

Theory vs. Reality

Of course, the reality is slightly more complicated. Because some schools are using supplemental data (such as home equity) to determine eligibility for their private aid, your expected contribution at a more selective university will most likely be different, and in some cases higher. In later chapters we’ll be talking about what factors can cause the schools to adjust the EFC calculated under the federal methodology, and more important, we’ll be showing you how to minimize the impact of these adjustments.

The Aid Package

About the time your child receives an offer of admission from a particular college, you will receive an award letter. This letter will tell you what combination of aid the FAO has put together for you in order to meet your need. The package will consist of three different types of aid:

Grants and Scholarships—These are the best kinds of aid, because they don’t have to be paid back. Essentially, a grant is free money. Some grant money comes from the federal government, some comes from the state, and some comes from the coffers of the college itself. Best of all, grant money is almost always tax-free. If you are in the 35% combined tax bracket, a $5,000 grant is the equivalent of receiving a raise of $7,692.

Scholarships are also free money, although there may be some conditions attached (academic excellence, for example). Contrary to popular wisdom, scholarships are usually awarded by the schools themselves. The amount of money available from outside scholarships is actually quite small.

Federal Work-Study (FWS)—The federal government subsidizes this program, which provides part-time jobs to students. The money earned is put toward either tuition or living expenses.

Student Loans—These loans, usually taken out by the student rather than the parents, are often subsidized (and guaranteed) by state or federal governments. The rates are usually much lower than regular unsecured loans. In most cases, no interest is charged while the student is in school, and no repayment is required until the student has graduated or left college.

Preferential Packaging

The FAOs at the individual colleges have a lot of latitude to make decisions. After looking at your financial information, for example, they might decide your EFC should be lower or higher than the need analysis processor computed it originally.

More important, the package the FAOs put together for a student will often reflect how badly the admissions office wants that student.

If a school is anxious to have your child in its freshman class, the package you will be offered will have a larger percentage of grant money, with a much smaller percentage coming from student loans and work study. If a college is less interested, the award will not be as attractive.

Your award will also reflect the general financial health of the college you are applying to. Some schools have large endowments and can afford to be generous. Other schools are financially strapped, and may be able to offer only the bare minimum.

If the school is truly anxious to get a particular student, it may also sweeten the deal by giving a grant or scholarship that isn’t based on need. A non-need scholarship may actually reduce your family contribution.

Unmet Need

In some cases, you may find that the college tells you that you have “unmet need.” In other words, they were unable to supply the full difference between the cost of their school and the amount they feel you can afford to pay. This is bad news. What the college is telling you is that if your child really wants to attend this college, you will have to come up with even more money than the college’s need analysis decided that you could pay.

Usually what this means is that you will have to take on additional debt. Sometimes the colleges themselves will be willing to lend you the money. Sometimes you will be able to take advantage of other loan programs such as the Federal Parent Loans for Undergraduate Students (PLUS), which is a partially-subsidized loan to parents of college students. The terms are less attractive than the subsidized student loans but still better than unsecured loans you would get from banks if you walked in off the street.

Sifting the Offers

The week acceptance and award letters arrive can be very tough, as you are confronted with the economic realities of the different schools’ offers. The school your child really wants to attend may have given you an aid package you cannot accept. The week will be immeasurably easier if you have taken the financial aid process into account when you were selecting schools to apply to in the first place.

Just as it is important to select a safety school where your child is likely to be accepted, it is also important to select what we call a “financial safety school” that is cheap enough to afford out of your own pocket in the event that the more expensive schools you applied to do not meet your full need. In some cases, the admissions safety school and financial safety school may be the same. If a student is a desirable candidate from an academic standpoint, she is likely to get a good financial aid package as well. However, you should also consider the economic health of the schools you are applying to as well as the past history of financial aid at those schools. This information can be gleaned from many of the college guides (including The Princeton Review’s The Best 381 Colleges, 2017 edition) available at bookstores and online booksellers.

It is also vital to make sure that there is a reasonable expectation that the package will be available for the next three years as well. How high do the student’s grades have to be in order to keep the package intact? Are any of the grants or scholarships they gave you one-time-only grants? Once you’ve received an offer, these are questions to ask the FAO.

Negotiating with the FAOs

Even if a school’s award letter has left you with a package you cannot accept—perhaps the percentage of student loan money in your package is too high; or perhaps your need was not fully met—you may still be able to negotiate a better deal.

Over the past few years we have noticed that the initial offer of aid, especially at some of the more selective schools, seems to have become subject to adjustment. In many cases, if you just accept the first offer, you will have accepted an offer that was not as high as the FAO was willing to go.

Many parents feel understandably hesitant to go back to the table. However, if the aid package is actually too low for you to be able to send your child to that school, you have little to lose by asking for more. And most FAOs will appreciate learning that they are about to risk losing a qualified applicant solely because of money.

The key in these negotiations is to be friendly, firm, and in control. Know what you want when you talk to the FAO and be able to provide documentation. In some cases, the FAO will alter the aid package enough to make it possible for you to afford to send your child to the school.

There is an entire section of this book devoted to the award letter—how to compare award letters, how to negotiate with FAOs, and how to apply for next year.

Same Time Next Year

The financial aid package you accept will last only one year. You will have to go through the financial aid process four separate times, filling out a new need analysis form each year until your child reaches the senior year of college. If your financial situation were to stay exactly the same, then next year’s aid package would probably be very similar to this year’s. We find, however, that most parents’ situations do change from year to year. In fact, after you finish reading this book, there may be some specific changes you’ll want to make.

How the Aid Process Really Works

Parents and students who understand how to apply for financial aid get more. It’s that simple. We aren’t talking about lying, cheating, or beating the system. We’re talking about understanding the system and taking advantage of the rules to get the best deal.

In Part Two, you will learn how to take control of the process. For those parents who are starting early, Chapter Two covers long-term investment strategies that minimize taxes and maximize aid eligibility. For those parents who have children in high school, Chapter Three through Chapter Six will show you how to use the financial aid formulas to save money. We’ll explain in detail how the different parts of your finances and family situation affect your EFC—and what adjustments you can make to boost your aid eligibility. In addition, we discuss how to pick colleges that will give the best aid packages, how to apply for state aid, and—very important—what the student can do.

In Part Three, we provide step-by-step guidelines for handling the financial aid application process, along with line-by-line guidance for completing the two most commonly used standardized financial aid forms for the 2017-2018 award year.

In Part Four, we discuss the offer. What does an award letter look like? What are the different types of aid you may receive, in detail? How do you compare award letters? How do you negotiate with the FAOs to get an improved package?

In Chapter Seven, we talk about innovative payment options and in Chapter Eight, we discuss managing student loans during and after school. In Chapter Nine, we cover in more detail some special topics such as divorced and separated parents, graduate students, minority students, independent students, and other topics that may be of interest to some of our readers. In Chapter Ten, we’ll discuss some important information involving educational tax benefits. For those who feel they need individualized guidance, Chapter Eleven provides tips on how to find a good financial aid consultant. In Chapter Twelve, future trends regarding financial aid and educational financing are covered, as well as some helpful tips for paying for college in these tough economic times.

In Part Five, you will find worksheets that will enable you to compute your expected family contribution for the federal methodology, a version of the 2017-2018 FAFSA, sample copies of promissory notes for the Stafford and PLUS loans, and copies of the 2015 U.S. personal income tax forms.