Paying for College Without Going Broke, 2017 Edition - Princeton Review, Kalman Chany (2016)

Part V. Worksheets and Forms

Calculating Your Expected Family Contribution

We realize that the pages of worksheets and tables that follow may seem a little intimidating. There are some books out there that claim you can calculate your EFC by consulting a single table that has been prepared by the book’s author. Unfortunately, these tables ask for such vague information from the parent that they do not provide an accurate estimation in the end. The calculators on various websites are all too frequently out-of-date or use flawed logic and result in a case of “garbage in-garbage out”.

When you fill out your need analysis form, you provide the processor with very specific information, but you will not be required to complete a worksheet such as this. The processor simply plugs your information into a computer program that automatically does all the calculations we are about to show you.

So Why Should You Bother to Go Through These Worksheets at All?

There are two excellent reasons.

First, by making the calculations yourself, you will be able to see how the process works; it is amazing how small changes in the way you list your financial information can produce big changes in the final result.

Second, by having an accurate idea of what your Expected Family Contribution will be, you can make informed decisions about which schools to apply to, how to answer questions on the individual school aid forms like, “How much do you think you can afford to pay for college?,” and what early steps you can take for next year.

Ughhhh

If these worksheets fill you with dread, you can always hire an independent financial aid consultant to do these calculations for you. Details on how to find one are in Chapter Eleven.

The Standard Disclaimer

While we believe that these worksheets and tables are accurate, they have not been approved by the U.S. Department of Education. In addition, the worksheets and tables regarding calculation of income have not been approved by the IRS and should not be used to calculate your tax liability for your income tax return.

Worksheet for Calculating the Expected Family Contribution for a Dependent Student

Please note that by TAXABLE INCOME, we mean income that the IRS considers subject to possible taxation, even if the IRS does not require that a tax return be filed because the income is below a minimum level determined by them. As such, it is possible to pay no tax on a small amount of taxable income. UNTAXED INCOME or NONTAXABLE INCOME refers to income that is never subject to income tax. Some income items, such as social security benefits, can be considered either taxable income or untaxed income, depending on the taxpayer’s total income.

Unless otherwise indicated, all references in this worksheet to specific IRS line numbers relate to those lines of the 2015 IRS 1040 form. To avoid confusion, we suggest that you refer to Chapter Three for more detailed descriptions of these various items. If the student’s biological or adoptive parents are living apart, please consult this page and this page-this page if you are unsure whose income should be listed on this worksheet.

The worksheets and tables that follow are based on the current formula for calculating the EFC for the 2017-2018 academic year.

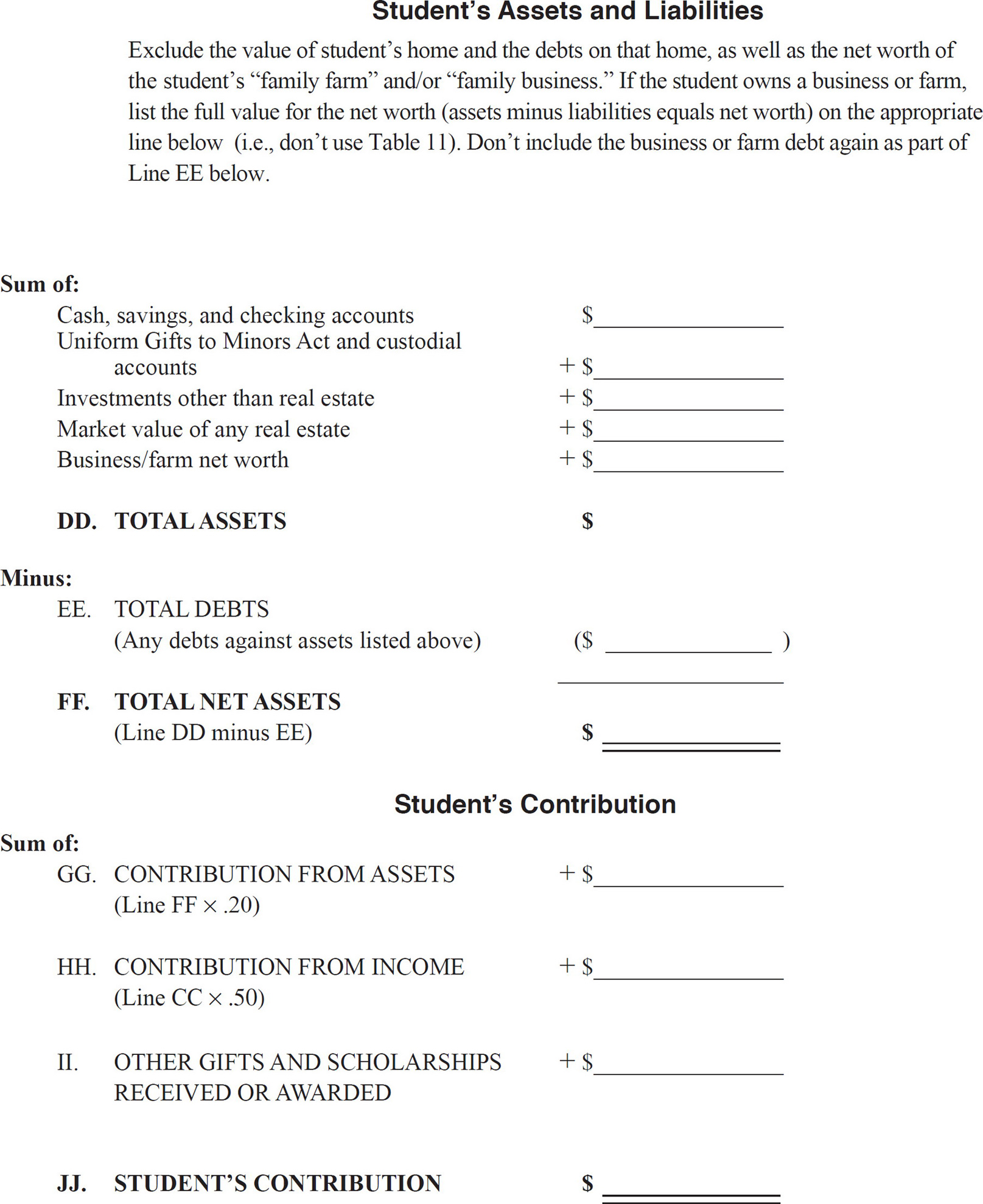

If you meet all of the criteria for the Simplified Needs Test (see this page-this page), you can calculate your EFC under the simplified formula by listing zero on Line O of the Parents’ Worksheet and on Line GG of the Student’s Worksheet. However, we recommend that you also calculate your EFC using asset information since some schools do not use the simplified formula when awarding their own aid funds.

Some helpful tips for completing the worksheets:

1.Round off all figures to the nearest dollar.

2.All income/expense items relate to yearly amounts. Do not use monthly or weekly figures. All asset/liability items relate to current amounts.

3.Since the 2017-2018 EFC will be using “prior-prior-year” income (see this page-this page), all references to income on the Tables and Worksheets that follow should be completed using 2015 income amounts. Most likely by the time you are completing these Tables, you will have already completed the 2015 Federal income tax returns if required to file a return. If that is the case for the student’s parents (or parent and stepparent) required to report information on the FAFSA, then most likely you can skip the calculations for Tables 3 and 6. Simply go to the last line of that respective Table and just list the dollar amount reported on the corresponding line of your U.S. individual income tax return(s). If separate returns were filed for 2015 by the custodial parent(s) - or the custodial parent and stepparent - reporting information on the FAFSA, list the combined dollar amounts from both adults’ tax returns (See this page if you are unsure which parent(s)’ information is to be reported on the FAFSA.) And please remember that one’s marital status for purposes of the FAFSA is the status as the date the FAFSA is filed, not the status at any time during the prior-prior year or prior year.

Exception: If 2015 federal tax individual income tax returns were completed as married filing jointly and the custodial parent is now separated, divorced or widowed from that other adult, then the entire Table 3 should be completed using only the custodial parent’s share of the respective items to determine the custodial parent’s share of the Adjusted Gross Income (AGI). To calculate the last line for Table 6: use the proportionate share of the AGI that you listed on line C of Table 3. Divide that number by the joint AGI figure reported on the actual tax return. The number you have just calculated should then by multiplied by the combined amount of U.S. Taxes paid on the joint return (using the applicable IRS line item referenced for the last line of Table 6) to determine the custodial parent’s share of the U.S. taxes paid that you will list on the last line of Table 6.

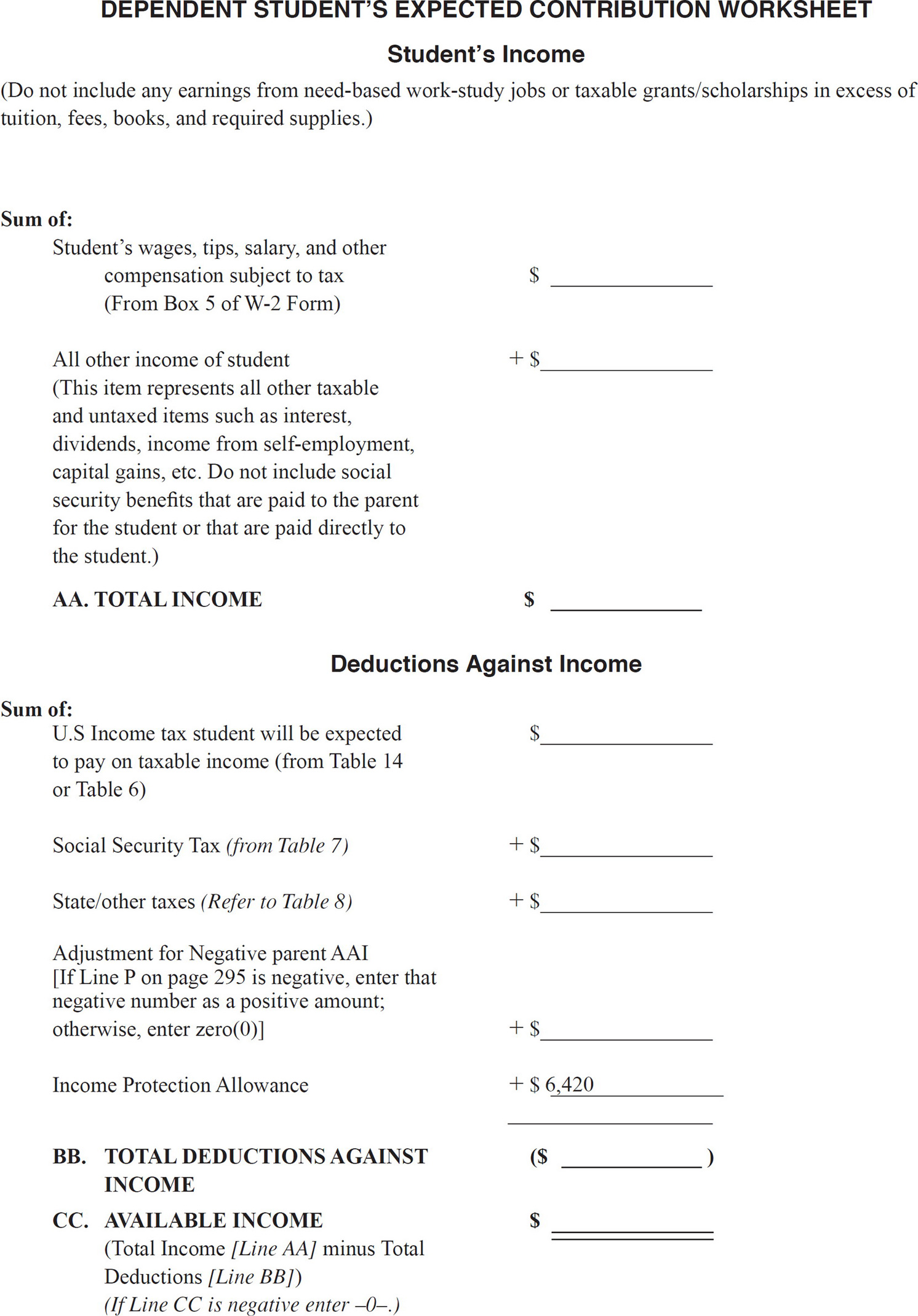

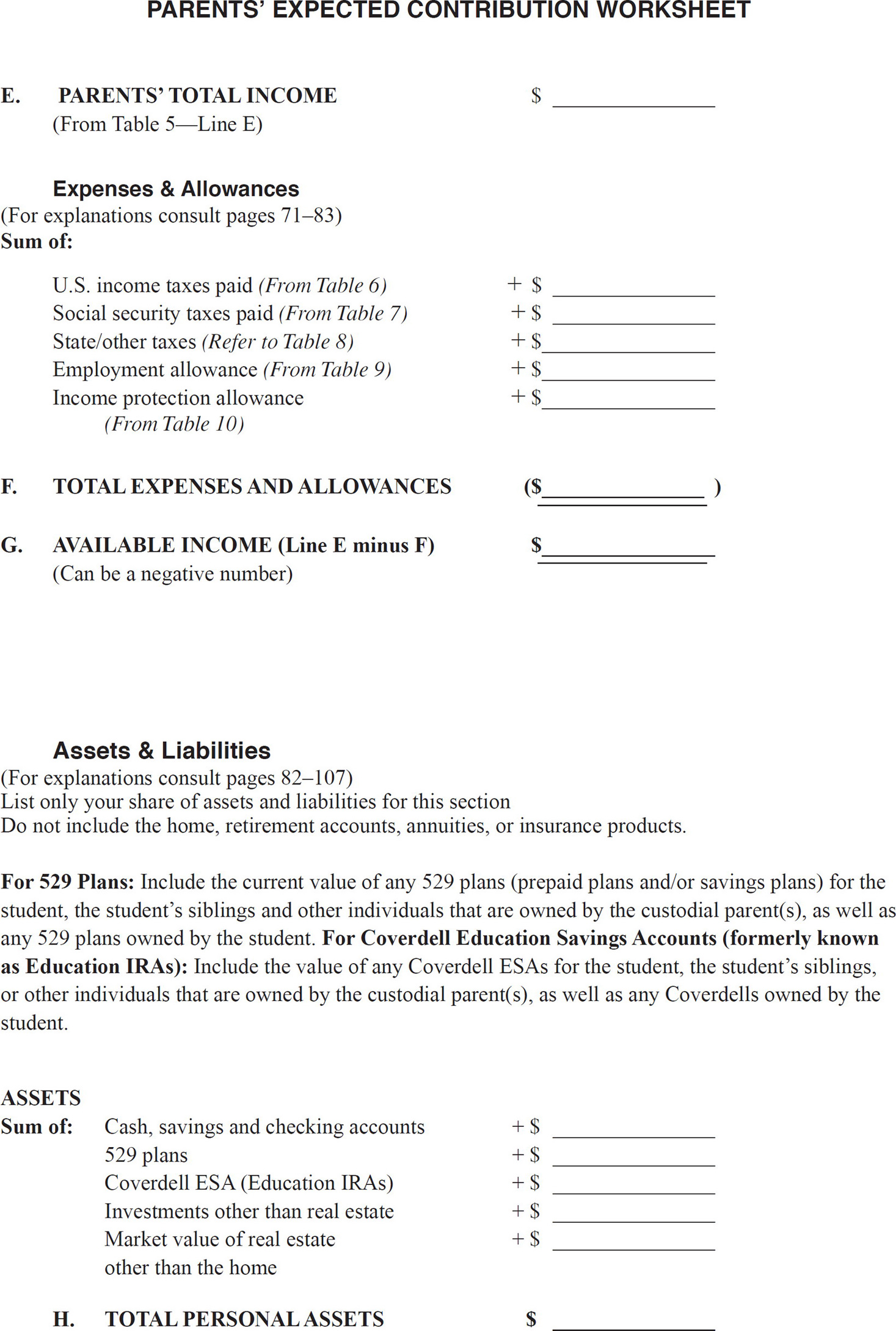

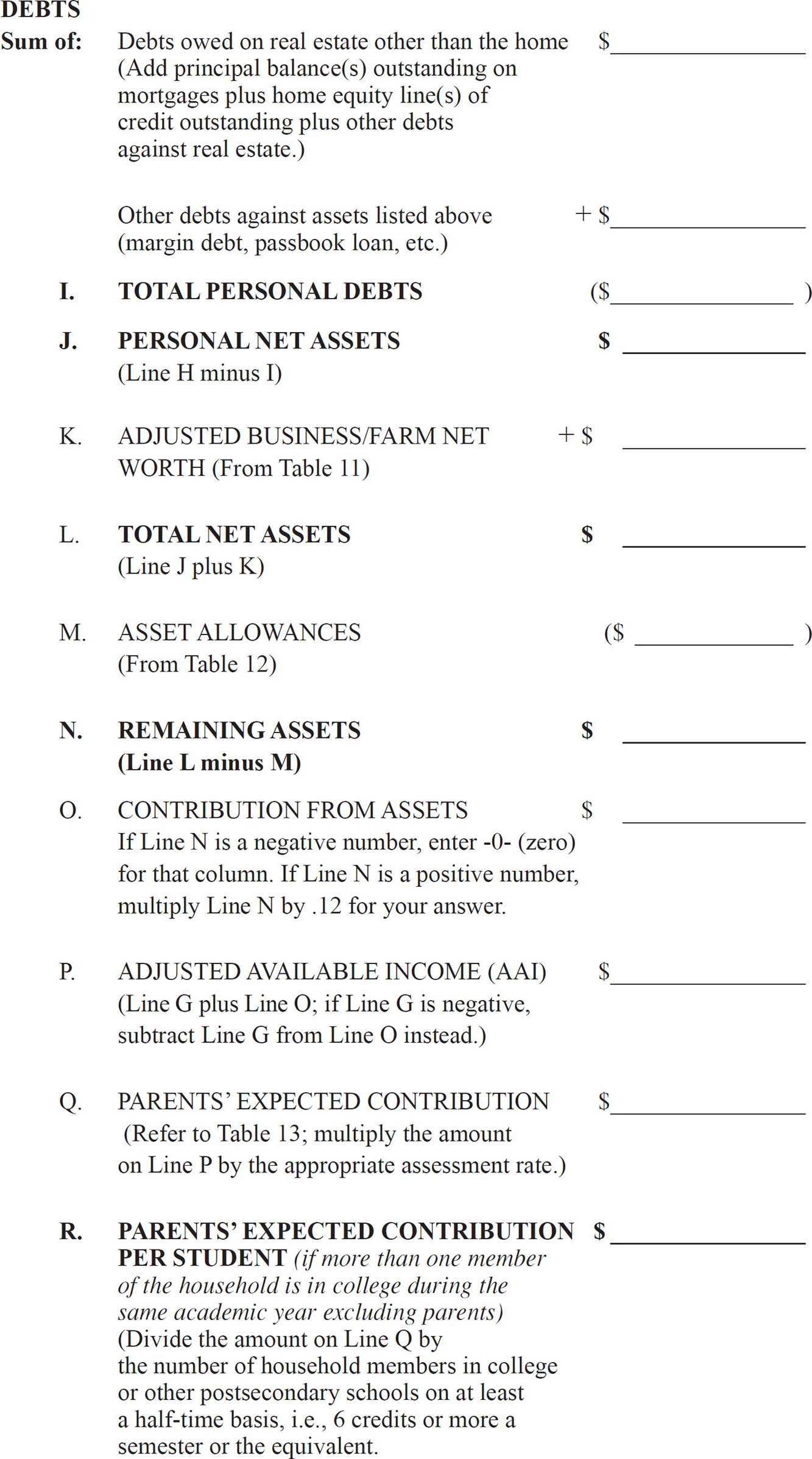

4.Tables 1 through 7 as well as Table 9 and Table 11 (if applicable) must be completed (in order) before you can begin work on the Parents’ Expected Contribution worksheet. The bottom lines from Tables 5 through 7 as well as Table 9 and 11 will be entered on the appropriate section of that worksheet. Table 8, Table 10, Table 12, and Table 13 should be utilized as you are completing that worksheet. Table 14 should be completed before you begin work on the Student’s Expected Contribution worksheet.

5.When completing Tables 1 and 2, be sure to enter the appropriate amounts under the proper column. Do not combine the amounts into one column, as this will give you an incorrect estimate of your Family Contribution.

6.Any number listed in parentheses should be subtracted from the number in the same column above it.

7.The earnings portion of any qualified withdrawals from Coverdell ESAs (Education IRAs) and Section 529 state savings accounts as well as the increase in the value of any tuition credits redeemed since the time of purchase for Section 529 prepaid plans will not be considered as part of the student’s or parent’s non-taxable income. Therefore, do not include any “earnings” from these accounts as part of your untaxed income in Table 4 or as part of “All other income of student and spouse” on the Student’s Expected Contribution Worksheet.

8.We suggest that you check your math. Even better, you should consider having another family member review your completed tables and worksheets for accuracy. Even if your family contribution figures are higher than the cost of attendance, you should still consider applying for aid since the FAOs may take other factors into account, you may be eligible for state aid benefits not based on these formulas, and/or you may have made an error in your calculations when doing these worksheets.

9.Prior to the 2011 edition, we always included worksheets to calculate the expected family contribution (EFC) under both the Institutional Methodology (IM) as well as the Federal Methodology (FM). However, in a change of policy, the College Board is no longer providing anyone with the tables and formulas to calculate the EFC under the IM. However, they have agreed to provide us with calculations of the EFC using the IM for some sample case studies along with the impact that some institutional options involving the home can have on the basic IM EFC number. A comparative calculation of the EFC in the federal methodology is provided as well. However, keep in mind that small changes to one’s situation can result in significant changes to the EFC in either formula. As such, these case studies should be used for informational purposes only. The EFC figures provided should not be relied on as an exact number of what your EFC will be, even if you believe your own situation is rather similar. These sample case studies and some additional comments regarding the IM appear on this page-this page.

Analyzing Your Numbers

Instead of thinking of the EFC as a definitive number for the amount you will be expected to pay towards college in a given year, you should think of the Parent’s Expected Contribution on Line R (this page) and the Student’s Expected Contribution on Line JJ (this page) as rough approximations for financial aid planning purposes. Until you receive a finalized award package from a school, it is impossible to know for certain the final number for what you will need to contribute. So instead of thinking of absolutes, it would be better to think in terms or probabilities. For example, if the EFC you calculate is quite a bit lower than the Cost of Attendance for the applicable school(s) under consideration, it would be better to focus on using those applicable strategies outlined earlier in the book to lower your EFC and complete the aid forms. This will increase the probability of your receiving more aid and will be more beneficial than trying to figure out exactly how much aid you will receive before admission and aid decisions are known. Similarly, if your EFC is significantly higher than the cost of attendance for all schools under consideration, then it is unlikely - though not certain - that you will not receive any need-based funds in a given year. While you should still apply for aid (as strange things sometimes can happen with the aid process), you should also have a back-up plan (i.e. applying to lower cost schools and/or to schools where there is a high probability the student will receive merit-based aid). And if in future years there will be an increase or decrease in the number of family members in college, then you should take subsequent years’ aid probabilities into account based on the differing number of students attending college.

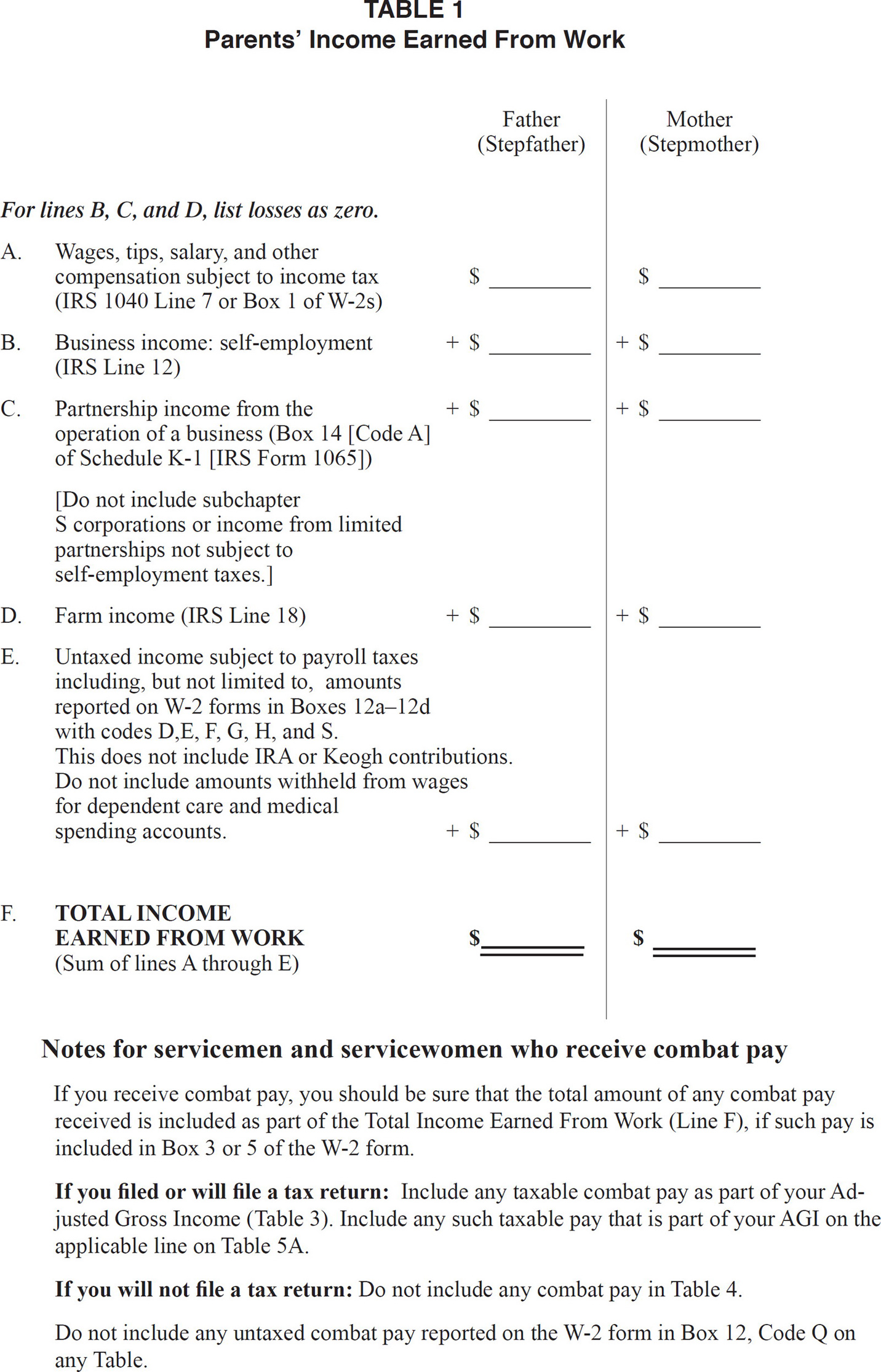

Click here to download a PDF of Table 1.

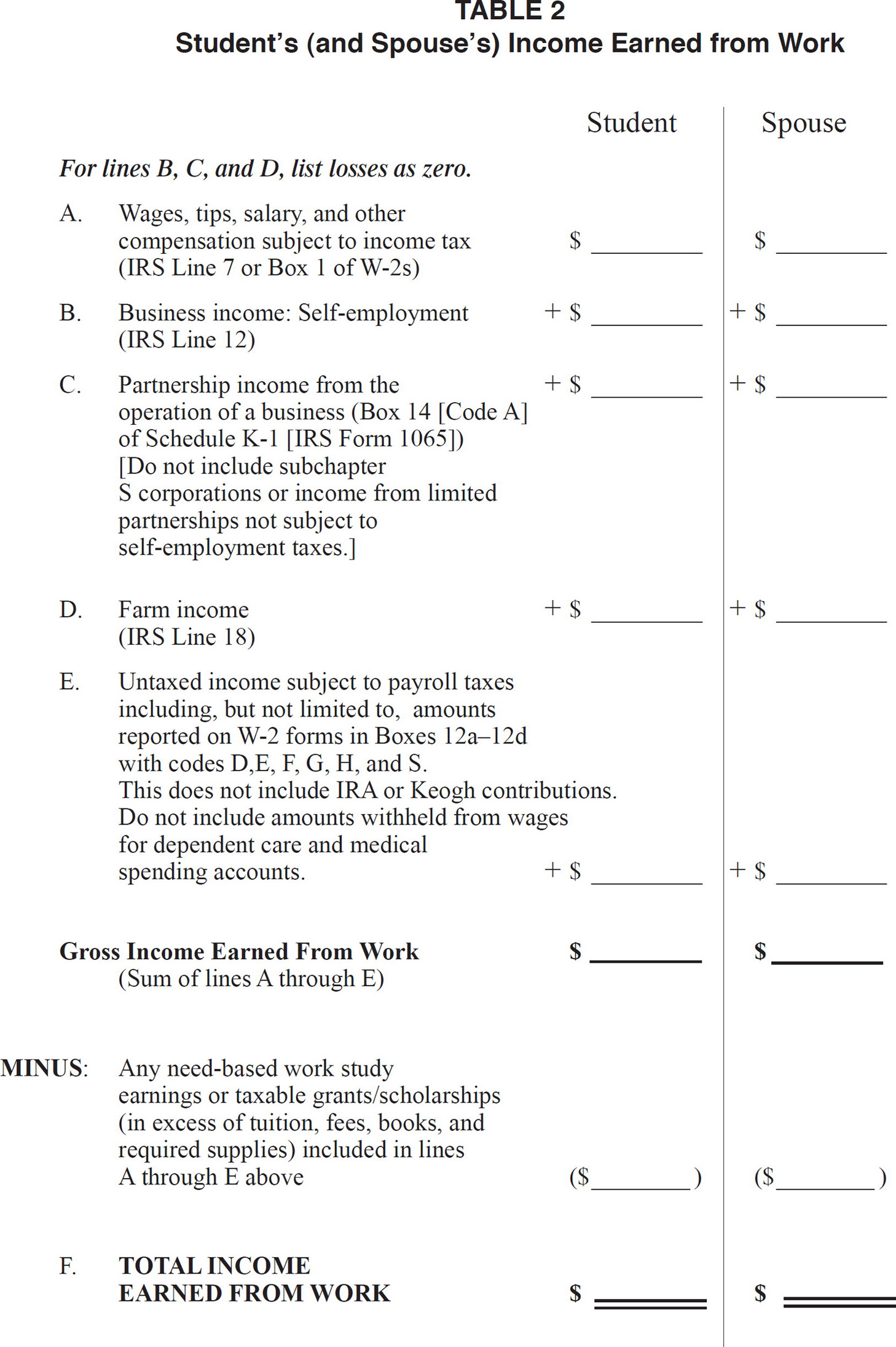

Click here to download a PDF of Table 2.

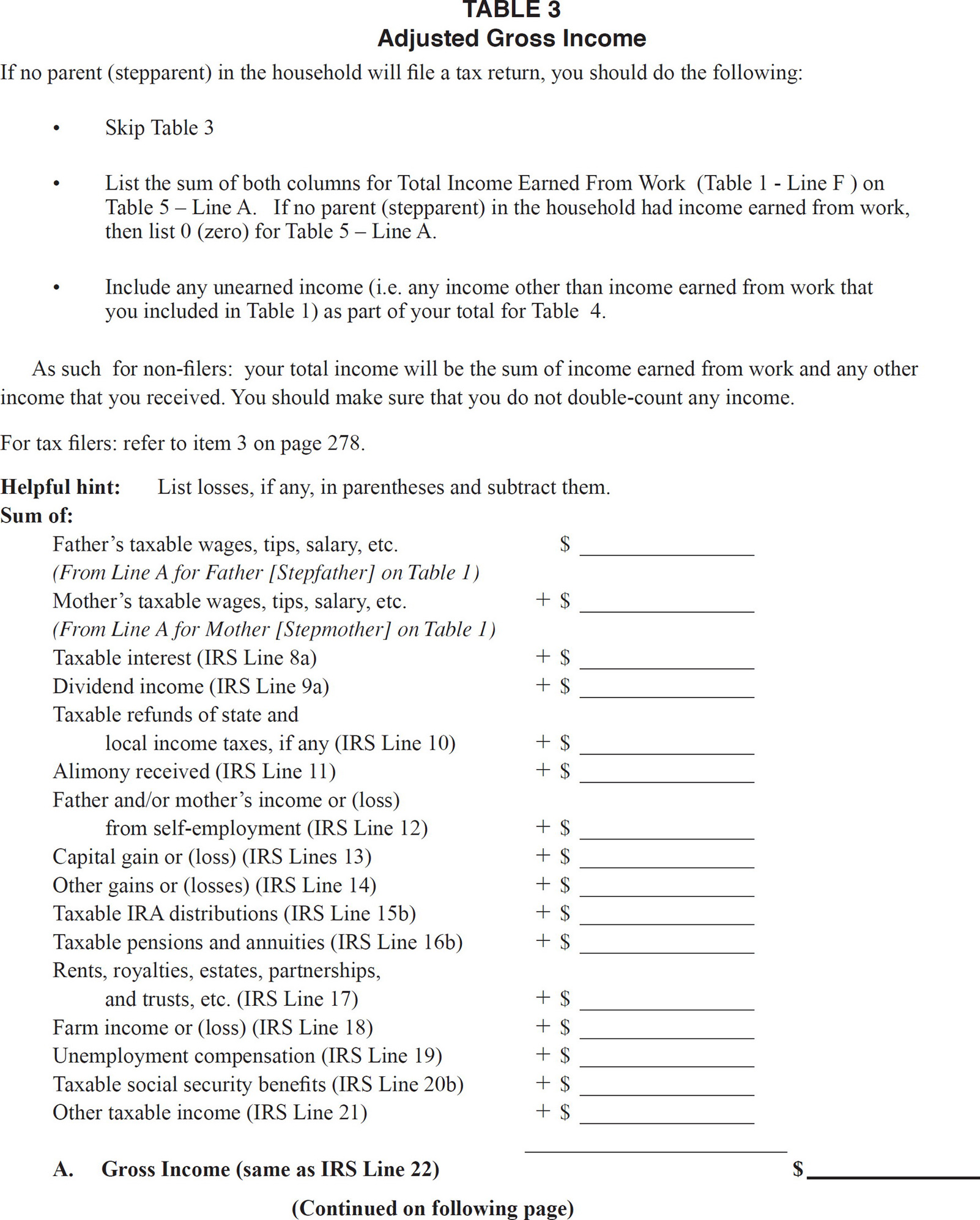

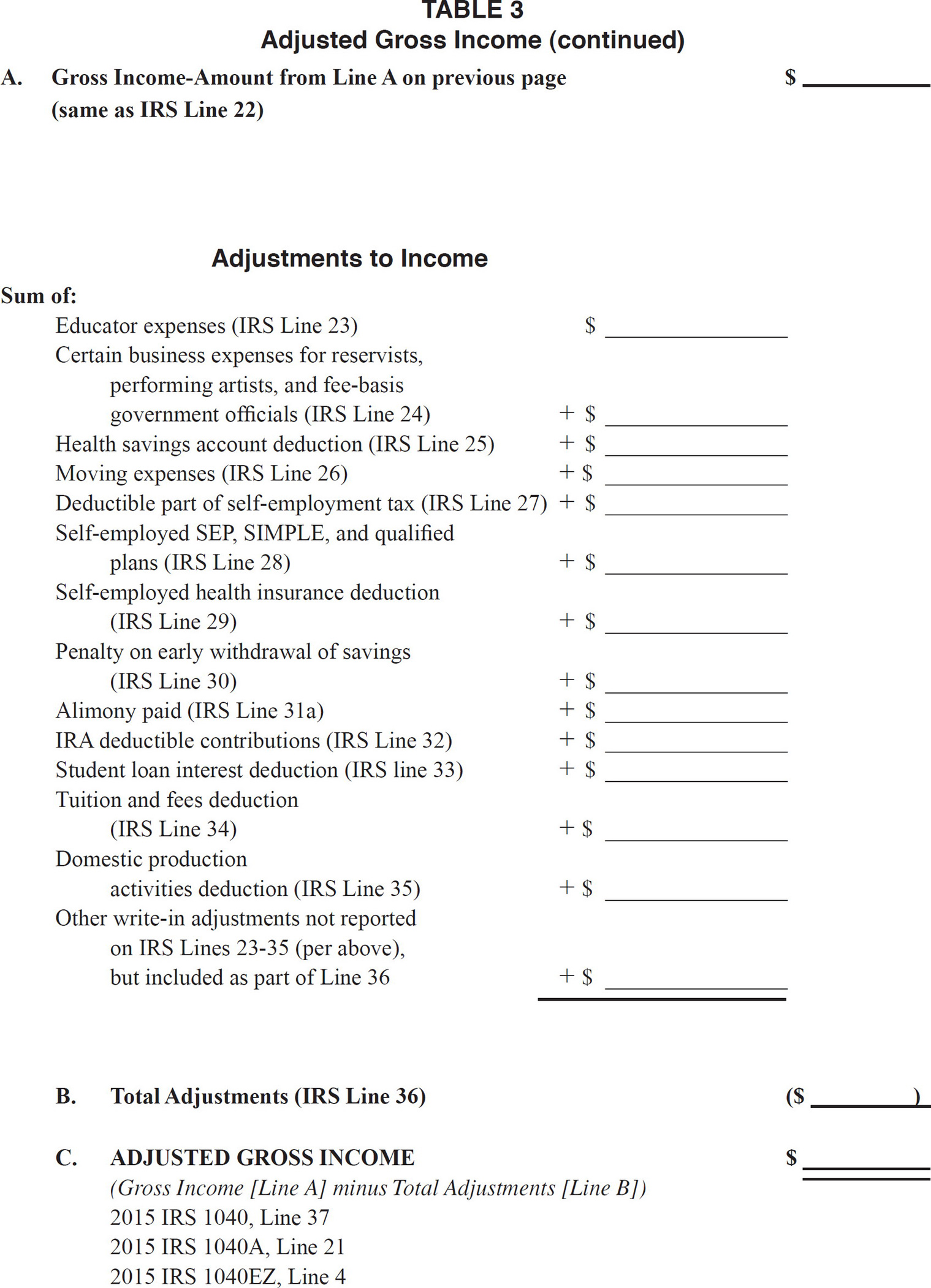

Click here to download a PDF of Table 3.

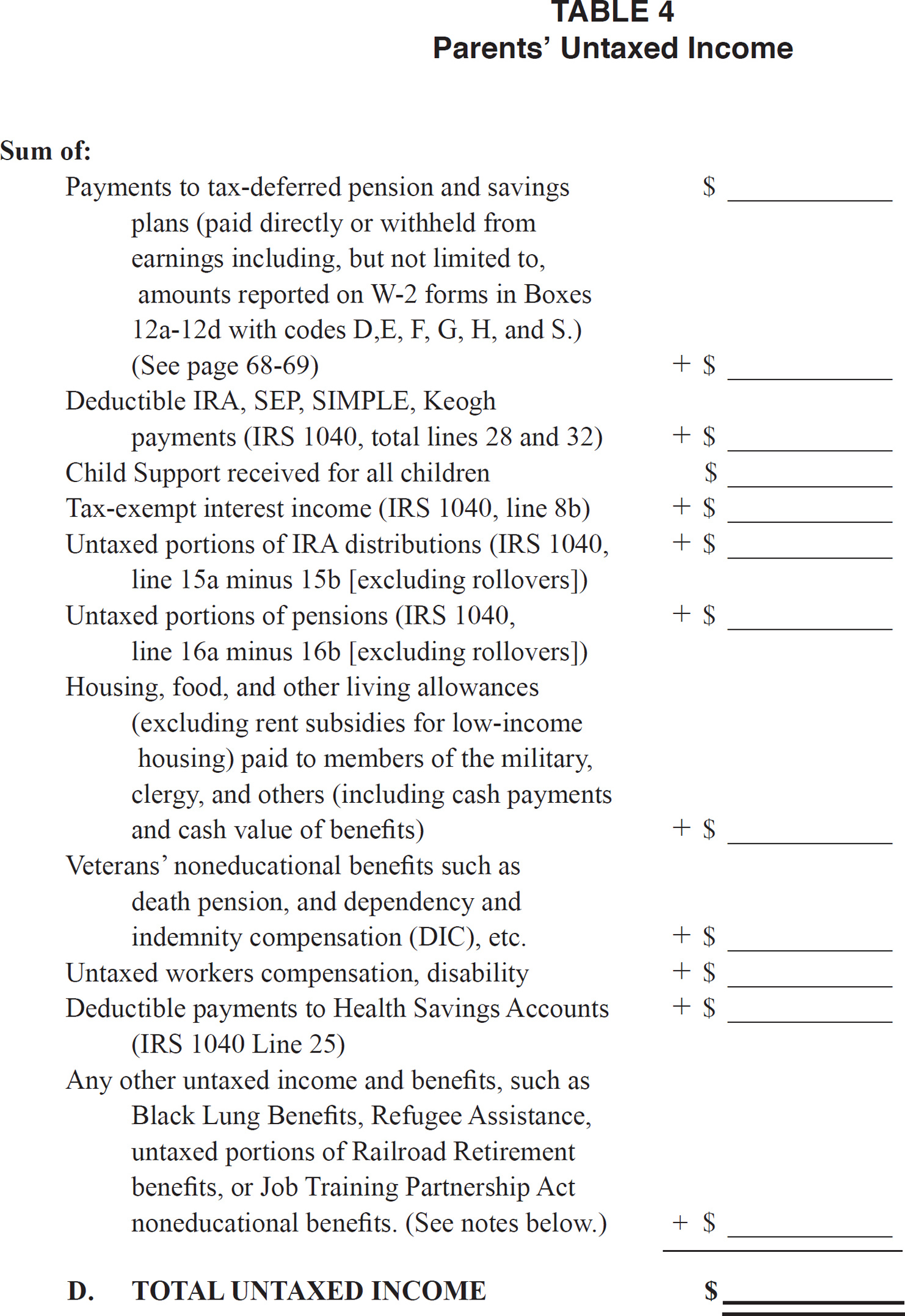

Click here to download a PDF of Table 4.

Do not include extended foster care benefits, student aid, earned income credit, additional child tax credit, welfare payments, untaxed Social Security benefits, Supplemental Security Income, Workforce Investment Act educational benefits, on-base military housing or a military housing allowance, combat pay, benefits from flexible spending arrangements (e.g., cafeteria plans), foreign income exclusion or credit for federal tax on special fuels.

For IRS 1040 tax-filers only: include any amounts reported on Line 25 of the IRS Form 1040 (the Health Savings Account deduction) as part of your response for the “Any other untaxed income and benefits…” (which is the last item above before the Total Untaxed Income).

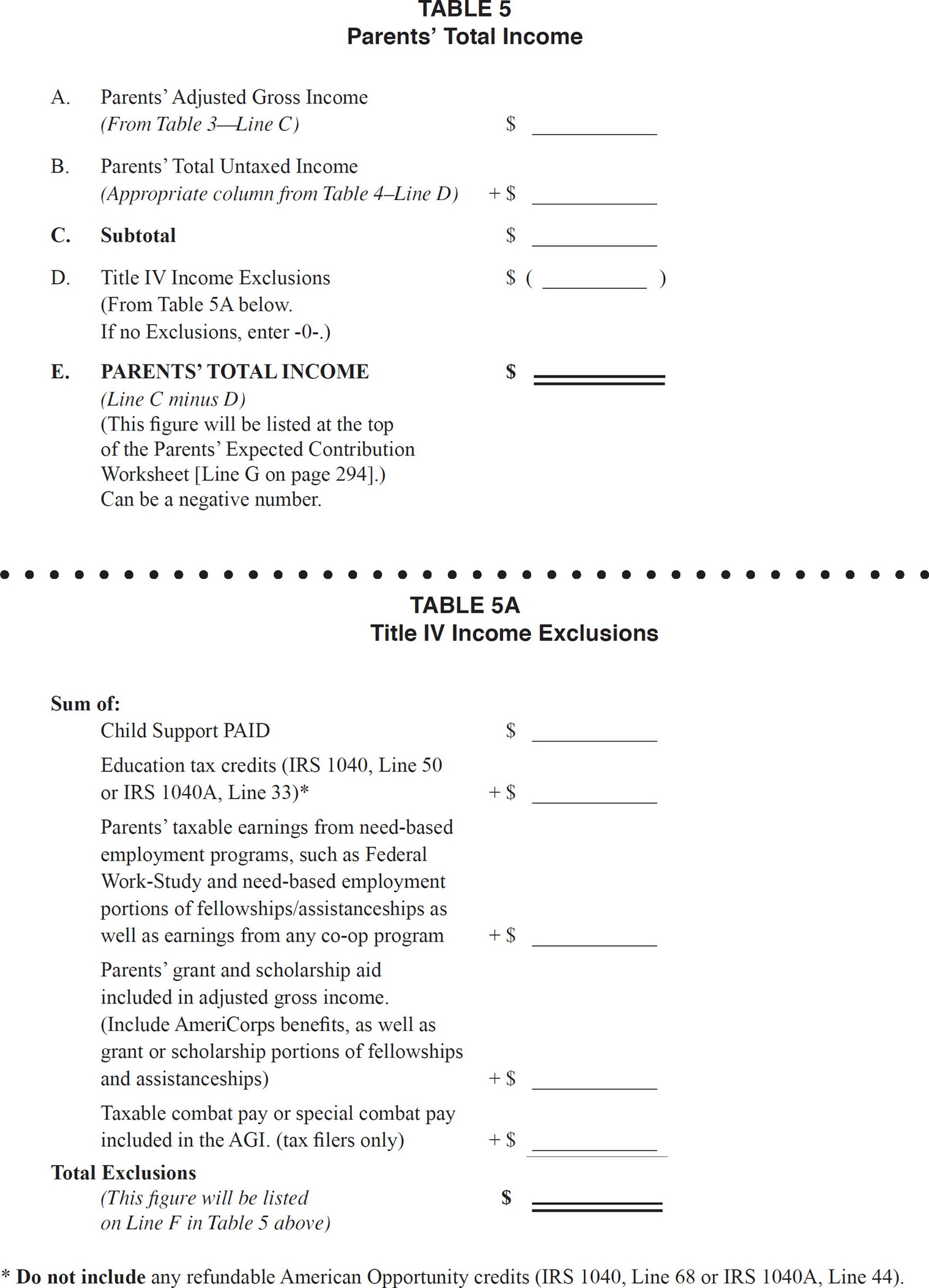

Click here to download a PDF of Table 5-Table 5A.

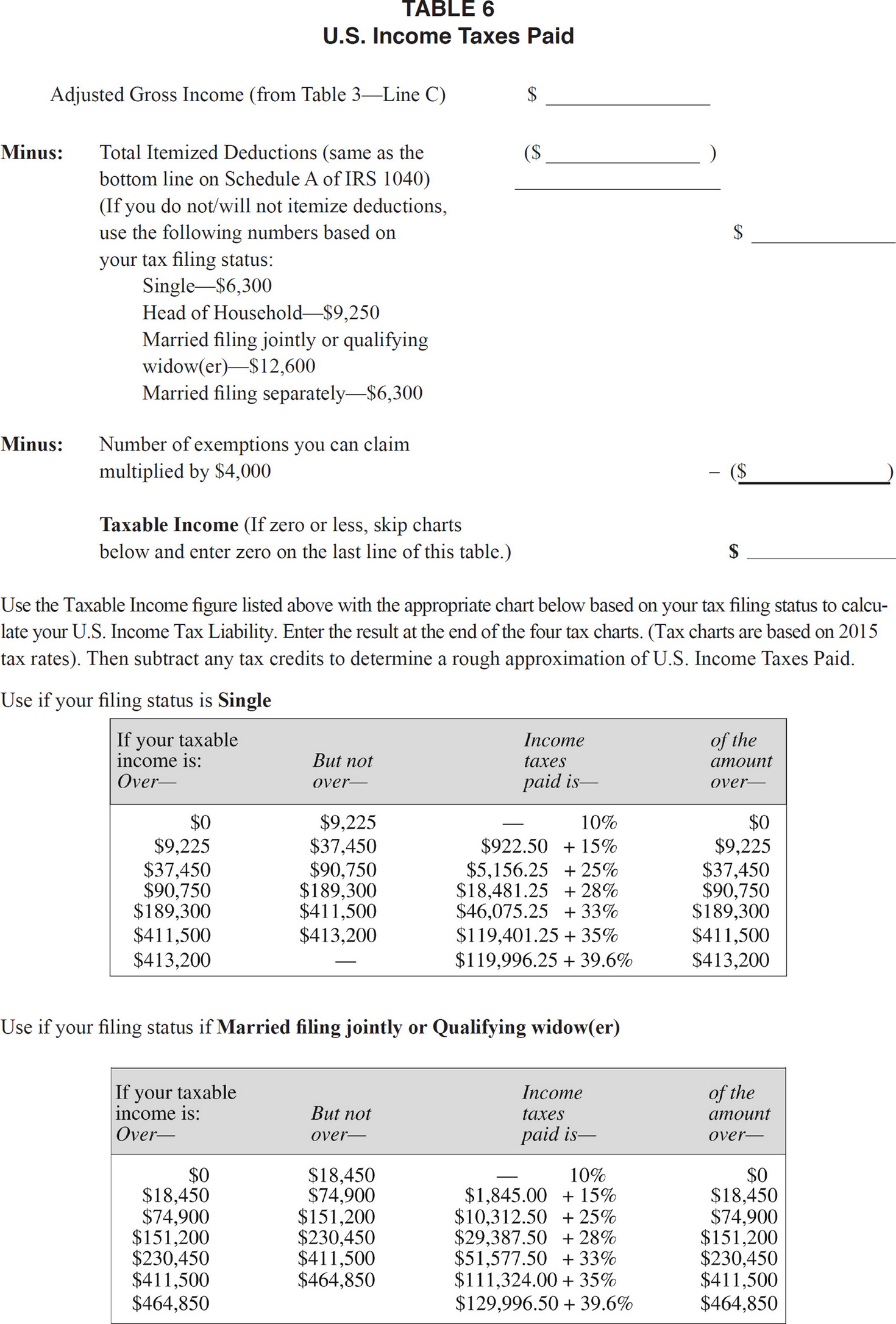

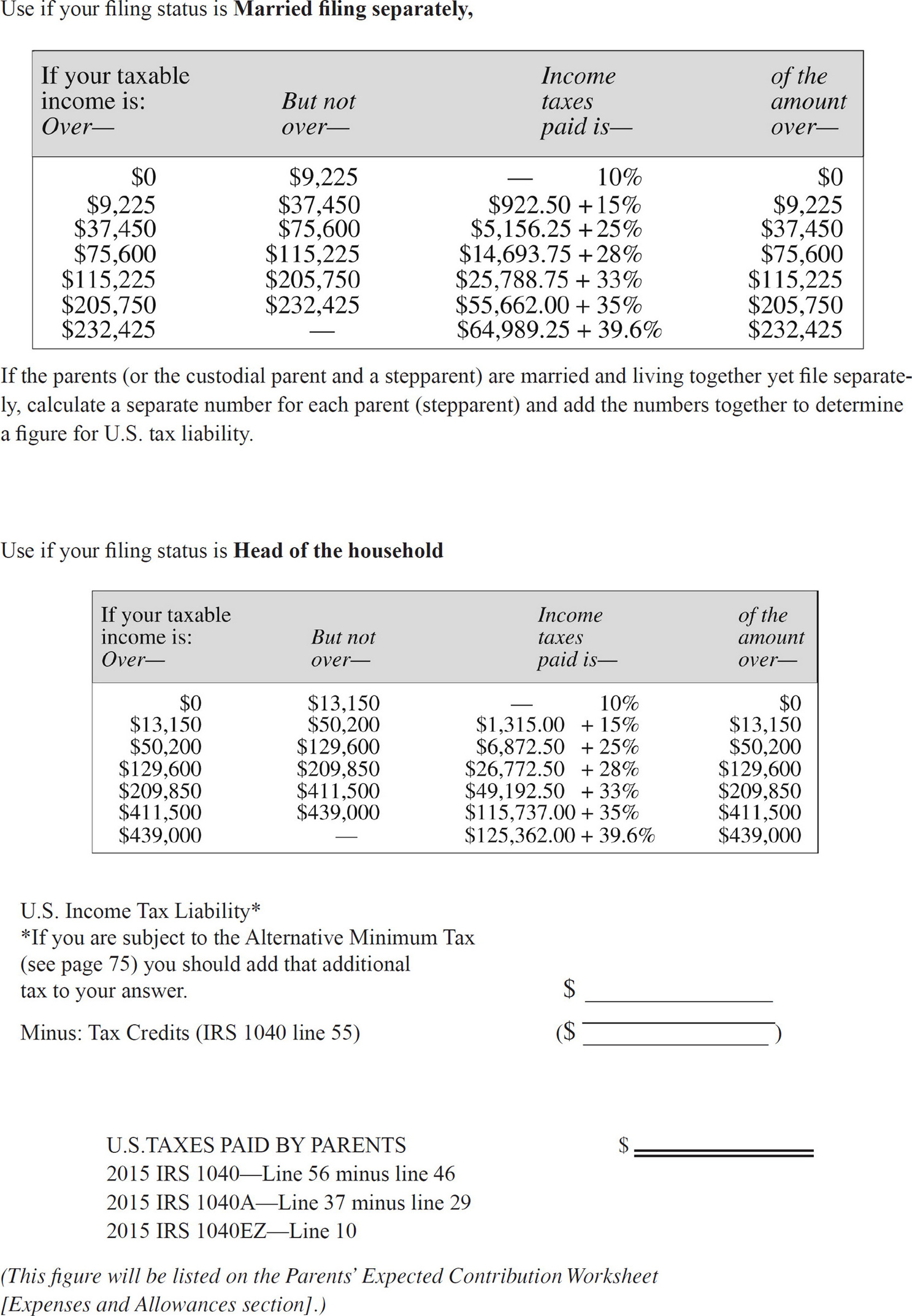

Click here to download a PDF of Table 6.

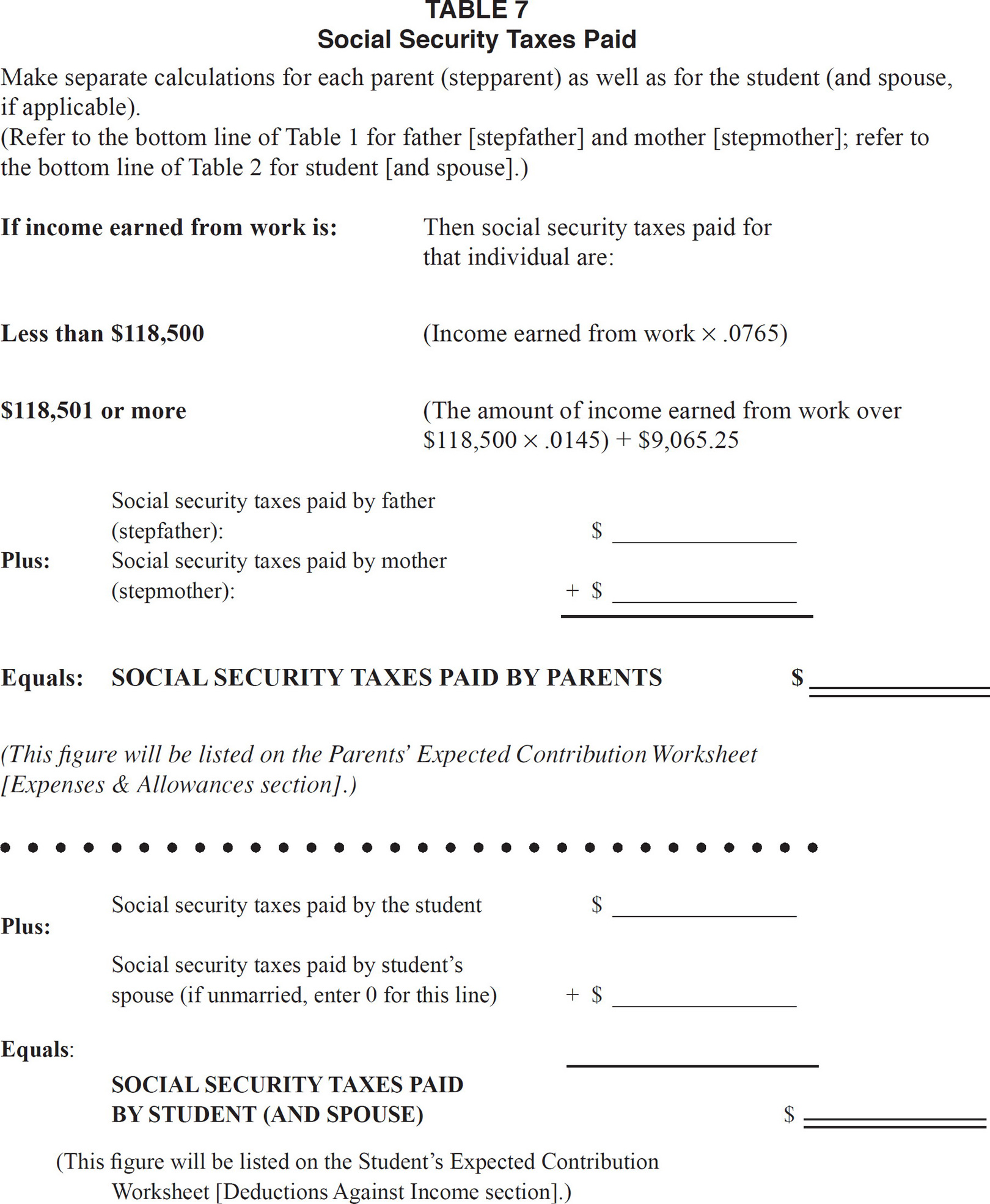

Click here to download a PDF of Table 7.

Beginning in 2013, an additional .9 percent (i.e. nine tenths of one percent) Medicare tax will be assessed on high earning households. This additional tax will be assessed on earned income above $200,000 for individuals and above $250,000 for married couples filing jointly. As we went to press, it was still unclear if the federal methodology will be adjusted to reflect these additional taxes paid. However, given the fact that such high earners typically do not qualify for Pell Grants or demonstrate much, if any, need for other federal need-based aid programs, there is a feeling among many in the aid community that the U.S. Department of Education (DOE) will not make any adjustments to the formula to reflect the additional Medicare taxes one may be paying. As such, you should use the table above to calculate the amount of taxes paid for the purposes of these worksheets. We will, of course, post any change on our update page (www.princetonreview.com/financialaidupdate) should the DOE change their policy.

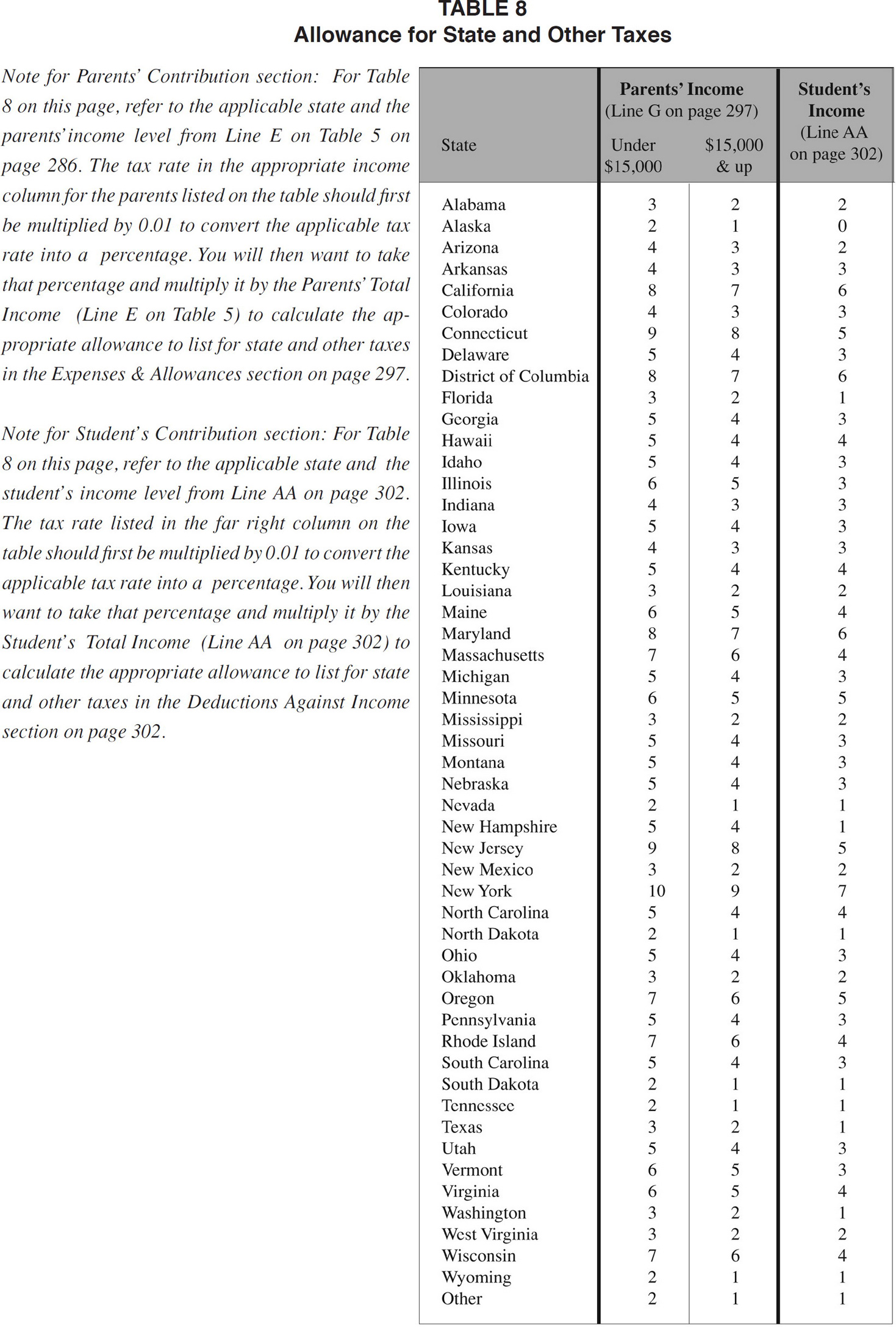

Click here to download a PDF of Table 8.

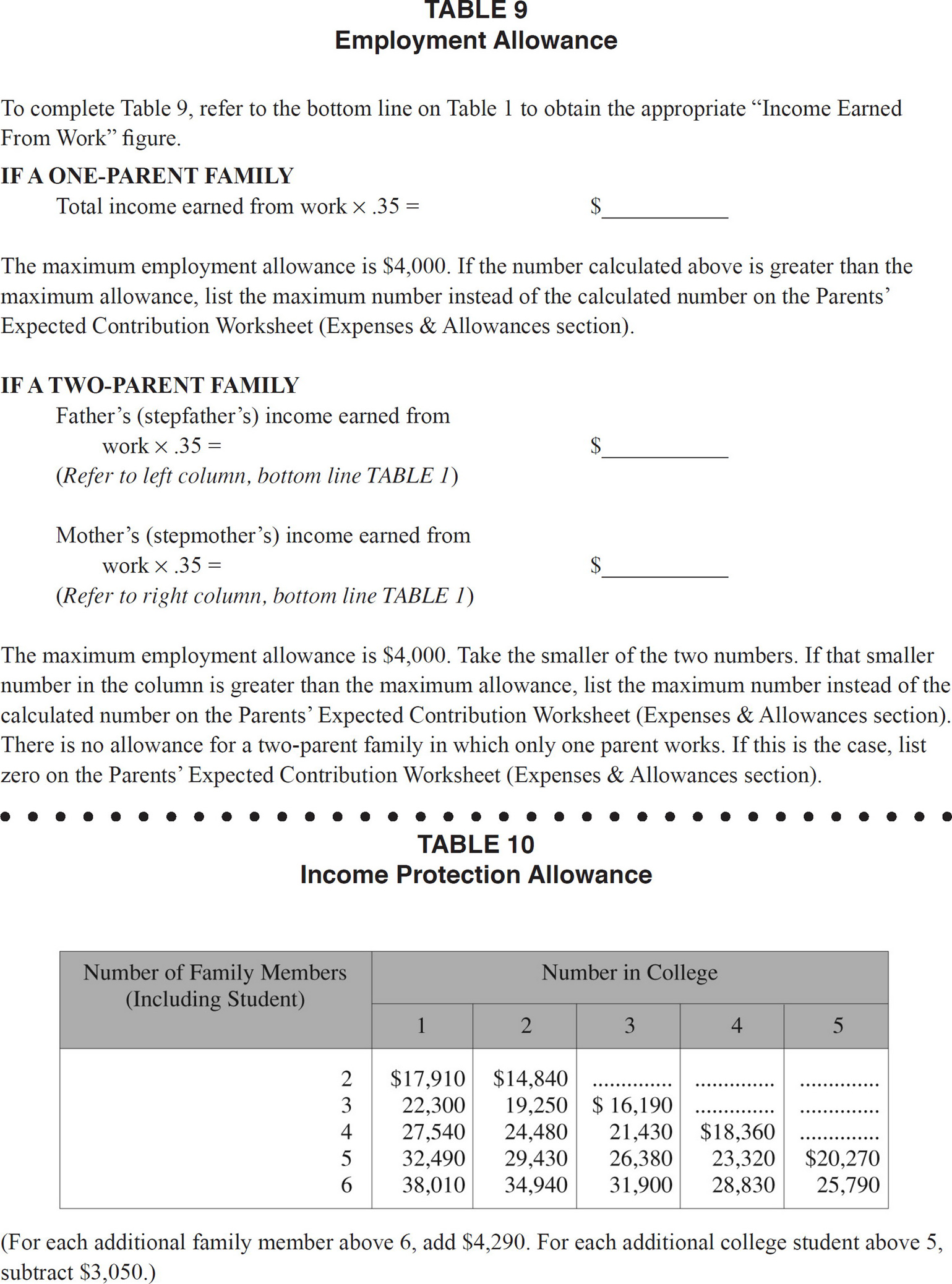

Click here to download a PDF of Table 9 and Table 10.

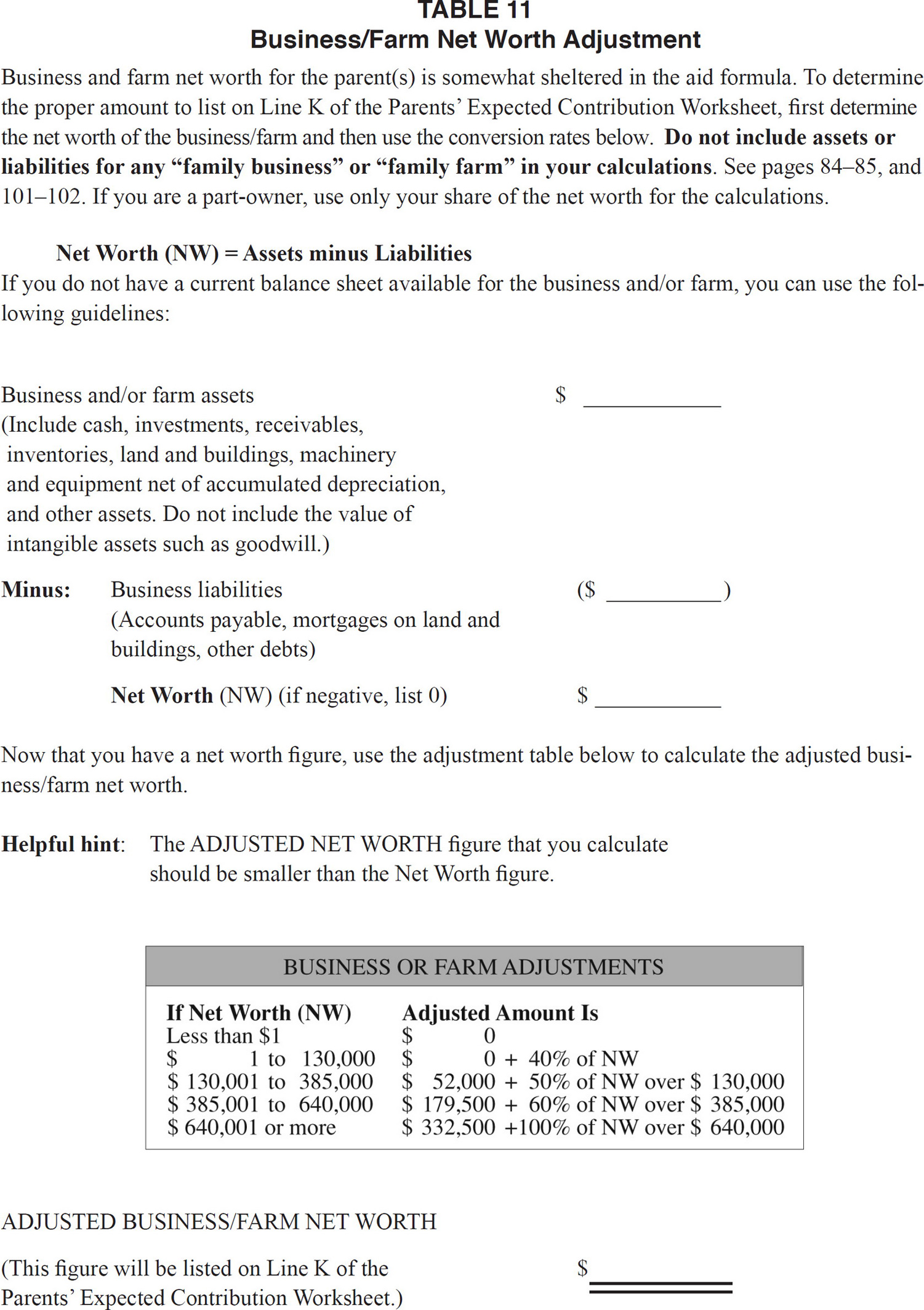

Click here to download a PDF of Table 11.

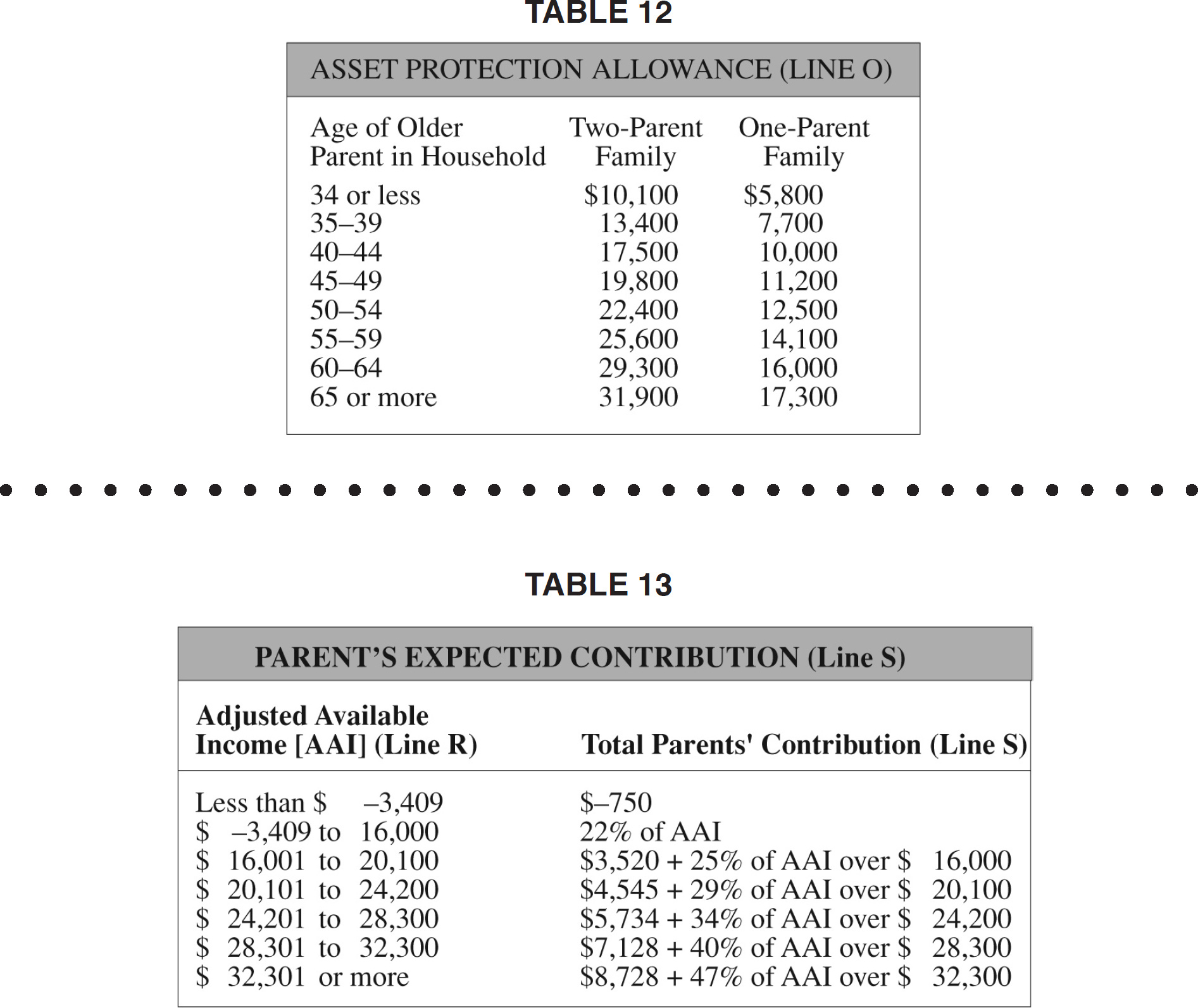

Click here to download a PDF of Table 12 and Table 13.

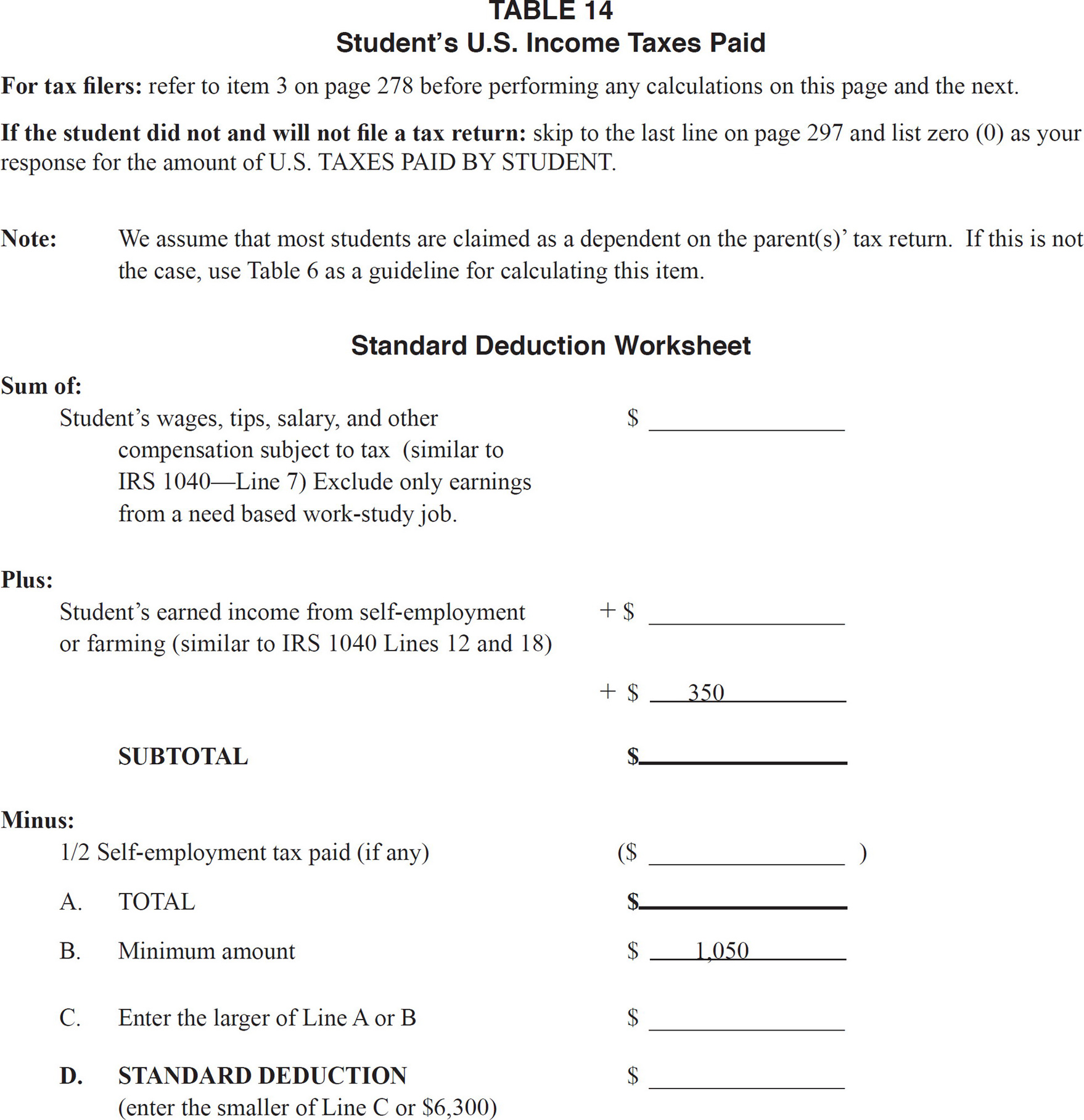

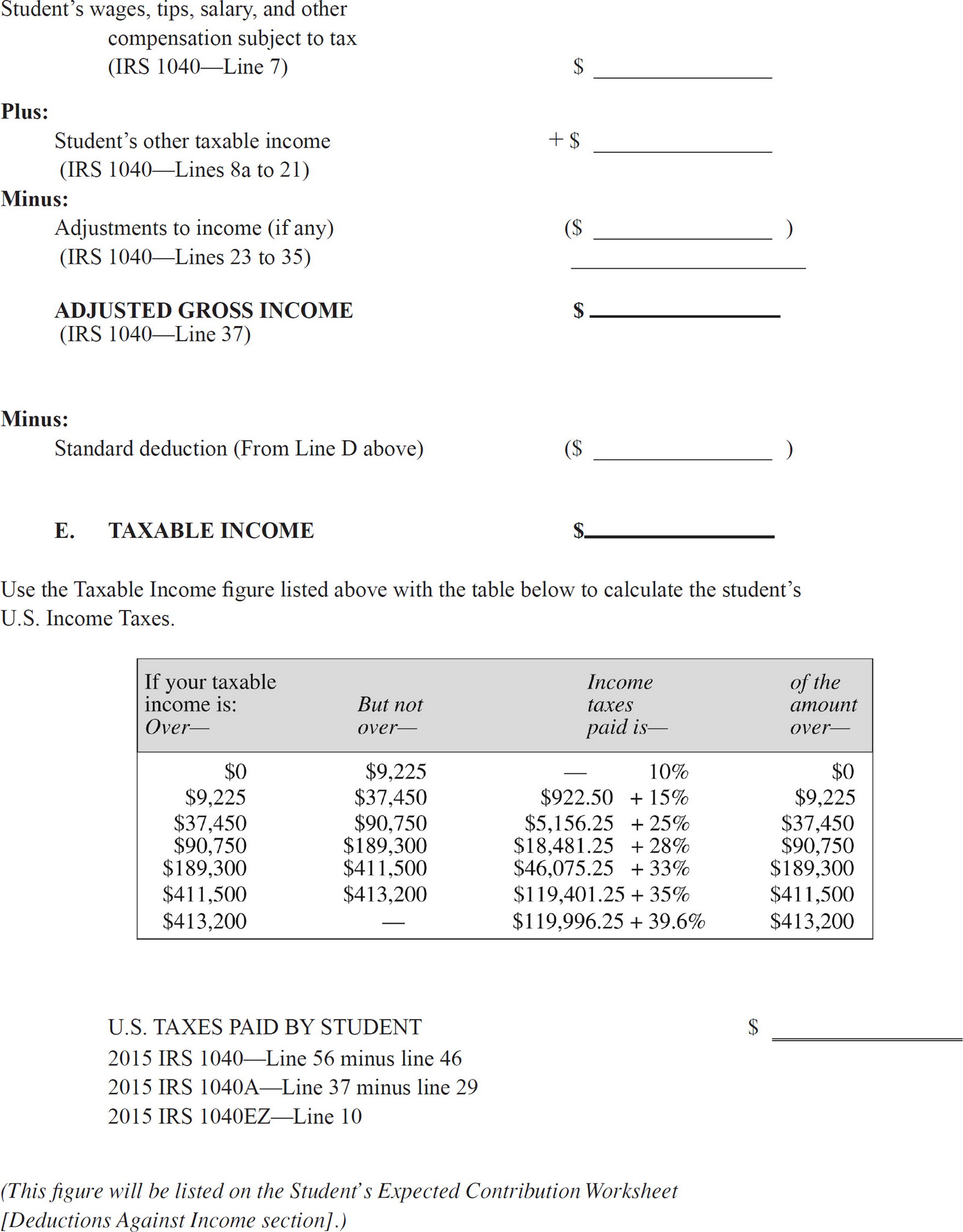

Click here to download a PDF of Table 14.