Bookkeeping & Accounting All-in-One For Dummies (2015)

Book III

Undertaking Monthly and Quarterly Tasks

Head online and visit www.dummies.com/extras/bookkeepingaccountingaio for some free bonus articles.¶

Head online and visit www.dummies.com/extras/bookkeepingaccountingaio for some free bonus articles.¶

In this book …

· Run and check your VAT return and know what you need to do - and when.

· Understand the RTI payroll system, an important aspect of many businesses.

· Know when an accountant may work together with the bookkeeper to provide period-end adjustments, whether at month-end or year-end.

Chapter 1

Adding the Cost of Value-Added Tax (VAT)

In This Chapter

![]() Examining the nuts and bolts of VAT

Examining the nuts and bolts of VAT

![]() Setting up for VAT

Setting up for VAT

![]() Getting the return right

Getting the return right

![]() Paying and reclaiming VAT

Paying and reclaiming VAT

A lot of mystery and tales of horror surround the subject of value-added tax (VAT). Now that HM Revenue & Customs administers both tax and VAT, the average businessperson is facing an even more powerful organisation with a right to know even more about your business.

The rules governing which goods and services are subject to VAT and which items of VAT are reclaimable can be quite complex. This chapter can only scratch the surface and give a broad understanding. Contact both HM Revenue & Customs and your accountant/auditor at an early stage to find out whether all your sales are subject to VAT and how you can ensure that you’re only reclaiming allowable VAT. Remember the following - get it right from the beginning.

Looking into VAT

VAT is a tax charged on most business transactions made in the UK or the Isle of Man. VAT is also charged on goods and some services imported from certain places outside the European Union and on some goods and services coming into the UK from other EU countries. VAT applies to all businesses - sole traders, partnerships, limited companies, charities and so on. In simple terms, all VAT-registered businesses act as unpaid collectors of VAT for HM Revenue & Customs.

VAT is a tax charged on most business transactions made in the UK or the Isle of Man. VAT is also charged on goods and some services imported from certain places outside the European Union and on some goods and services coming into the UK from other EU countries. VAT applies to all businesses - sole traders, partnerships, limited companies, charities and so on. In simple terms, all VAT-registered businesses act as unpaid collectors of VAT for HM Revenue & Customs.

Examples of taxable transactions are:

· Selling new and used goods, including hire purchase

· Renting and hiring out goods

· Using business stock for private purposes

· Providing a service; for example, plumbing or manicure

· Charging admission to enter buildings

As you can see, this list covers most business activities.

Certain services are exempt from VAT, including insurance, finance and credit, some property transactions, certain types of education and training, fundraising charity events and subscriptions to membership organisations. Supplies exempt from VAT don’t form part of your turnover for VAT purposes.

VAT is a tax on the difference between what you buy (inputs) and what you sell (outputs), as long as these items fall within the definition of taxable transactions (see the following sections). At the end of a VAT reporting period, you pay over to HM Revenue & Customs the difference between all your output tax and input tax.

· Input tax is the VAT you pay out to your suppliers for goods and services you purchase for your business. You can reclaim the VAT on these goods or services coming in to your business. (See ‘Getting VAT back’, later in this chapter.) Input tax is, in effect, a tax added to all your purchases.

· Output tax is the VAT that you must charge on your goods and services when you make each sale. You collect output tax from your customers on each sale you make of items or services going out of your business. Output tax is, in effect, a tax added to all your sales.

Notice 700: The VAT Guide needs to be your bible in determining how much you need to pay and what you can reclaim. (You can find this guide at www.hmrc.gov.uk .)

Notice 700: The VAT Guide needs to be your bible in determining how much you need to pay and what you can reclaim. (You can find this guide at www.hmrc.gov.uk .)

Knowing what to charge

In addition to the obvious trading activities, you need to charge VAT on a whole range of other activities, including the following:

· Business assets: If you sell off any unneeded business assets, such as office equipment, commercial vehicles and so on, you must charge VAT.

· Sales to staff: Sales to staff are treated no differently than sales to other customers. Therefore you must charge VAT on sales such as canteen meals, goods at reduced prices, vending machines and so on.

· Hire or loans: If you make a charge for the use of a business asset, this amount must incur VAT.

· Gifts: If you give away goods that cost more than £50, you must add VAT. Treat gifts as if they’re a sale for your VAT records.

· Goods for own use: Anything you or your family take out of the business must go on the VAT return. HM Revenue & Customs doesn’t let you reclaim the VAT on goods or services that aren’t used for the complete benefit of the business.

HM Revenue & Customs is really hot on using business stock for your own use, which is common in restaurants, for example. HM Revenue & Customs knows that you do it and has statistics to show how much on average businesses ‘take out’ this way. If you don’t declare this item when you’ve used business stock, be prepared to have HM Revenue & Customs jump on you from a great height.

HM Revenue & Customs is really hot on using business stock for your own use, which is common in restaurants, for example. HM Revenue & Customs knows that you do it and has statistics to show how much on average businesses ‘take out’ this way. If you don’t declare this item when you’ve used business stock, be prepared to have HM Revenue & Customs jump on you from a great height.

· Commission earned: If you sell someone else’s goods or services and get paid by means of a commission, you must include VAT on this income.

· Bartered goods: If you swap your goods or services for someone else’s goods or services, you must account for VAT on the full value of your goods or services that are part of this arrangement.

· Advance payments: If a customer gives you any sum of money, you must account for VAT on this amount and the balance when he collects the goods. If, for example, you accept payment by instalments, you collect VAT on each instalment.

· Credit notes: These items are treated exactly like negative sales invoices, so make sure that you include VAT so that you can effectively reclaim the VAT on the output that you’re going to pay, or may have already paid.

In general you don’t have to charge VAT on goods you sell to a VAT-registered business in another European Community (EC) member state. However, you must charge UK VAT if you sell goods to private individuals.

Knowing how much to charge

The rate of VAT applicable to any transaction is determined by the nature of that transaction. The 20 per cent rate applies to most transactions. The type of business (size or sector) generally has no bearing on the VAT rates. Three rates of VAT currently exist in the UK:

· A standard rate of 20 per cent: This is the rate at which most businesses should add VAT to products and services that they sell.

· A reduced rate, currently 5 per cent: Some products and services have a lower rate of VAT, including domestic fuel, energy-saving installations and the renovation of dwellings.

· A zero per cent rate: Many products and services are given a zero rating, including some foods, books and children’s clothing. A zero rating for a product or service isn’t the same as a total exemption.

You can view a list of business areas where sales are reduced-rated or zero-rated in Notice 700, which you can download from www.hmrc.gov.uk . You can call the VAT helpline on 0845 010 9000 if you have queries about the list.

Registering for VAT

First of all you need to register for VAT so that you can charge VAT on your sales and reclaim VAT on your purchases.

The current VAT registration threshold is £81,000 (this threshold changes each year, so check with HM Revenue & Customs for the current threshold). So if your annual UK turnover (sales, not profit) is less than this figure, you don’t have to register for VAT.

You may find it advantageous to register for VAT even though your sales fall below the VAT registration threshold (and may never exceed it). Registering for VAT gives your business increased credibility - if your customers are large businesses, they expect their suppliers to be VAT registered. Also, you can’t reclaim VAT if you’re not registered. If your business makes zero-rated supplies but buys in goods and services on which you pay VAT, you want to be able to reclaim this VAT.

You may find it advantageous to register for VAT even though your sales fall below the VAT registration threshold (and may never exceed it). Registering for VAT gives your business increased credibility - if your customers are large businesses, they expect their suppliers to be VAT registered. Also, you can’t reclaim VAT if you’re not registered. If your business makes zero-rated supplies but buys in goods and services on which you pay VAT, you want to be able to reclaim this VAT.

As your business grows, it may be difficult to know whether you’ve broken through the VAT registration threshold. HM Revenue & Customs states that you must register for VAT if

· At the end of any month the total value of the sales you made in the past 12 months (or less) is more than the current threshold.

· At any time you have reasonable grounds to expect your sales to be more than the threshold in the next 30 days.

After you register for VAT, you’re on the VAT treadmill and have to account for output tax on all your sales, keep proper VAT records and accounts, and send in VAT returns regularly.

Paying in and Reclaiming VAT

HM Revenue & Customs adopts a simple process, laying down and policing the rules in two ways:

· Businesses must file periodic returns to the VAT Central Unit (see the later section ‘Completing Your VAT Return’ for when to file VAT payments).

· Businesses receive periodic enquiries and visits from HM Revenue & Customs to verify that these returns are correct.

VAT returns must be completed by the due date, which is shown on the form, and is usually one month after the period covered by the return. Yes, this schedule means that you’ve one month to complete your VAT return. Any payment due to HM Revenue & Customs must be sent electronically. As long as you complete your VAT return on time and don’t arouse the suspicions of HM Revenue & Customs, you may not meet the staff for many years.

You face a financial penalty if your return is late and/or seriously inaccurate. HM Revenue & Customs can and does impose hefty fines on businesses that transgress. Also, offenders who previously had the luxury of quarterly VAT returns often find themselves having to complete monthly VAT returns. Don’t mess around with HM Revenue & Customs!

HM Revenue & Customs targets certain business sectors. In general, businesses structured in a complex manner (such as offshore companies) that involve a lot of cash are likely to come in for extra scrutiny. Experience tells HM Revenue & Customs that looking closely at certain types of businesses often yields extra revenues. Also, businesses that submit VAT returns late on a regular basis attract fines and may be forced to submit monthly VAT returns together with payments on account.

Paying VAT online

HM Revenue & Customs has phased out paper VAT returns, and (apart from a small number of exceptions) you need to file your VAT return online and pay your VAT electronically. The advantage of paying online is that you qualify for seven additional calendar days after the date shown on your return to pay. Visit the HM Revenue & Customs website at www.hmrc.gov.uk and click VAT Online Services to find out about doing your VAT return online. Here’s how it works:

1. Fill in the appropriate boxes on your VAT return, using 0.00 for nil amounts.

2. Make any payment due by electronic methods (BACS, CHAPS or bank giro).

3. Wait for the acknowledgement that your electronic return was received.

4. Keep a copy of the electronic acknowledgement page for your records.

Getting help for small businesses

HM Revenue & Customs has some arrangements to make VAT accounting easier for small businesses. The accounting method that your business uses determines when you pay VAT:

· Annual Accounting: If you use the Annual Accounting scheme, you make interim payments, either three or nine, spread across the year, towards an estimated annual VAT bill. This arrangement evens out VAT payments and helps to smooth cash flow. At the end of the year, you submit a single annual return and settle up for any balance due (or maybe receive a cheque back from HM Revenue & Customs). In effect, you complete one annual VAT return at the end of the year but make periodic payments on account (you agree with HM Revenue & Customs how many payments per year you want).

This arrangement may suit the disorganised business that struggles to complete the more traditional four quarterly VAT returns.

You can use this scheme if you don’t expect your annual sales (excluding VAT) to exceed £1.35 million (or in special cases £1.6 million).

The range is based on estimates of your total sales. If your sales have a boost and exceed £1.35 million, you can stay on this scheme just as long as sales don’t go beyond £1.6 million. If sales exceed £1.6 million, you must come off this scheme.

The range is based on estimates of your total sales. If your sales have a boost and exceed £1.35 million, you can stay on this scheme just as long as sales don’t go beyond £1.6 million. If sales exceed £1.6 million, you must come off this scheme.

· Cash Accounting: If you use the Cash Accounting scheme, your business accounts for income and expenses when they’re actually incurred. Therefore, you don’t pay HM Revenue & Customs VAT until your customers pay you. This arrangement may suit a business that has regular slow-paying customers. You can use this scheme if your estimated VAT taxable turnover isn’t more than £1.35 million.

· Flat Rate Scheme: This arrangement makes VAT much simpler by allowing you to calculate your VAT payment as a flat percentage of your turnover. The percentage is determined according to the trade sector in which your business operates.

Under this scheme you can’t reclaim any VAT on your actual purchases, which may mean that you lose out if your business is significantly different to the business model HM Revenue & Customs applies to you. Also, if your business undertakes a large capital spend that has a lot of VAT on it, you’re unlikely to get the entire amount back under this scheme.

You can use this scheme if your annual sales (excluding VAT) aren’t expected to exceed £150,000.

· Retail Schemes: If you make lots of quite small sales to the public, you may find it difficult to issue a VAT invoice for each sale. Several available retail schemes may help. For example, you can use a simpler receipt that a till can print out.

To find out more about the numerous retail schemes, visit the HM Revenue & Customs website (www.hmrc.gov.uk) and click the link for VAT, under Businesses and Corporations. Then click on ‘Getting Started with VAT’, followed by ‘Accounting schemes’ to simplify VAT accounting or save money, and scroll down the screen and select ‘VAT retail scheme’.

Getting VAT back

When you’re completing your VAT return, you want to reclaim the VAT on every legitimate business purchase. However, you must make sure that you only reclaim legitimate business purchases. The following is the guidance that HM Revenue & Customs gives:

· Business purchases: You can reclaim the VAT on all business purchases and expenses, not just on the raw materials and goods you buy for resale. These purchases include things like business equipment, telephone and utility bills, and payments for other services such as accountants’ and solicitors’ fees.

You can’t deduct your input tax for certain purchases, including cars, business entertainment and second-hand goods that you bought under one of the VAT second-hand schemes.

· Business/private use: If you use services for both business and private purposes, such as your telephone, you can reclaim VAT only on the business use. No hard and fast rules exist on how you split the bill - your local HM Revenue & Customs office is likely to consider any reasonable method.

· Pro-forma invoice: If a supplier issues a pro-forma invoice, which includes VAT that you have to pay before you’re supplied with the goods or service, you can’t deduct this amount from your VAT bill on your next return. You can only deduct VAT when you get the proper invoice.

· Private motoring: If you use a business car for both business and private use, you can reclaim all the VAT as input tax, but you have to account for tax on any private motoring using a scale charge (see the later section ‘Using fuel for private motoring’).

· Lost invoices: You can’t reclaim any VAT on non-existent invoices. If you do and you get a VAT visit, you’re in for the high jump!

· Bad-debt relief: Occasionally, customers don’t pay you, and if you’ve already paid over to HM Revenue & Customs the output VAT on this sale, you’re going to be doubly annoyed. Fortunately, HM Revenue & Customs isn’t totally heartless - you can reclaim this VAT on a later VAT return.

Completing Your VAT Return

You need to submit your VAT return online. To do so, go to www.hmrc.gov.uk and click on the link ‘Register (new users)’ in the box called ‘Do it online’ on the top-left side of the page. The site guides you through the setup process. Ensure that you allow plenty of time to register, because it involves receiving user IDs and passwords through the post.

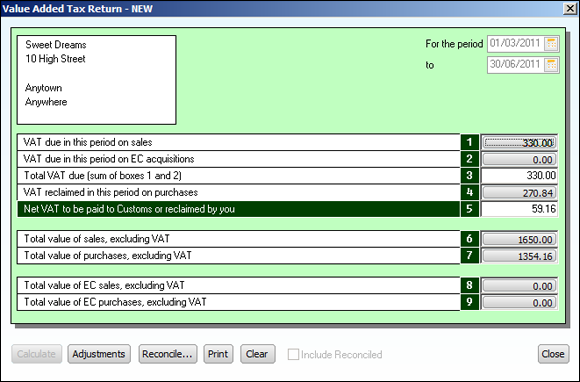

Letting your accounting software complete your VAT return is the easiest method. Sage 50 Accounts does VAT returns as a matter of routine, picking up all the necessary information automatically. You just need to tell the program when to start and when to stop picking up the invoice information. Sage 50 Accounts even prints out the VAT return in a format similar to HM Revenue & Customs’ own VAT return form. Figure 1-1 shows the Sage 50 Accounts VAT return.

Figure 1-1: The Sage 50 Accounts VAT return.

Filling in the boxes

At last we come to the nitty-gritty of what figures go into each of the nine boxes on the VAT return. Table 1-1 helps keep the process simple.

Table 1-1 VAT Return Boxes

|

Box |

Information Required |

|

1 |

VAT due on sales and other outputs in the period. Notice 700: The VAT Guide gives further help. |

|

2 |

VAT due from you on acquisitions of goods from other EC Member States. Notice 725 VAT: The Single Market gives further help. |

|

3 |

For paper returns, enter the sum of boxes 1 and 2.The electronic form handles all the maths needed to complete the form. |

|

4 |

The input tax you’re entitled to claim for the period. |

|

5 |

The difference between the figures from boxes 3 and 4. Deduct the smaller from the larger. If the figure in box 3 is more than the figure in box 4, you owe this amount to HM Revenue & Customs. If the figure in box 3 is less than the figure in box 4, HM Revenue & Customs owes you this amount. |

|

6 |

Your total sales/outputs excluding any VAT. |

|

7 |

Your total purchases/inputs excluding any VAT. |

|

8 |

Complete this box only if you supplied goods to another EC member state. Put in this box the total value of all supplies of goods (sales) to other member states. |

|

Note: If you include anything in box 8, make sure that you include the amount in the box 6 total. |

|

|

9 |

Complete this box only if you acquired goods from another EC member state. Put in this box the total value of all goods acquired (purchases) from other member states. |

|

Note: If you include anything in box 9, make sure that you include the amount in the box 7 total. |

We deliberately keep this process simple, but remember that behind every box is a multitude of traps set to ensnare you. The HM Revenue & Customs website, www.hmrc.gov.uk , has detailed notes to help you complete your VAT return.

Glancing at problem areas

Not all businesses are entirely straightforward for VAT purposes. Some business activities have their own unique rules and regulations. The list below outlines the exceptions to the rule:

· Building developer: See VAT Notice 708: Buildings and construction about non-deductible input tax on fixtures and fittings. Also look at Notice 742 Land and Property, regarding land and new-build property sales.

· Tour operator: See VAT Notice 709/5: Tour operators’ margin scheme about VAT you can’t reclaim on margin scheme supplies.

· Second-hand dealer: See VAT Notice 718: margin schemes for second-hand goods, works of art, antiques and collectors’ items about VAT you can’t reclaim on second-hand dealing.

Using fuel for private motoring

If your business pays for non-business fuel for company car users, you must reduce the amount of VAT you reclaim on fuel by means of the scale charge.

Notice 700/64: Motoring expenses gives full details. If you use the scale charge, you can recover all the VAT charged on road fuel without having to split your mileage between business and private use. A scale charge is a method of accounting for output VAT on road fuel bought by a business that is then used for private mileage. The scale charge is based on the CO2 emissions of each vehicle. You can obtain your CO2 emissions from your vehicle registration certificate (for cars registered after 2001). The HMRC website offers full details of all CO2 emissions and the associated fuel scale charge. See www.hmrc.gov.uk for further details.

Notice 700/64: Motoring expenses gives full details. If you use the scale charge, you can recover all the VAT charged on road fuel without having to split your mileage between business and private use. A scale charge is a method of accounting for output VAT on road fuel bought by a business that is then used for private mileage. The scale charge is based on the CO2 emissions of each vehicle. You can obtain your CO2 emissions from your vehicle registration certificate (for cars registered after 2001). The HMRC website offers full details of all CO2 emissions and the associated fuel scale charge. See www.hmrc.gov.uk for further details.

Leasing a motor car

You may find that you’re able to claim only 50 per cent of the input tax on contract hire rentals in certain situations. If you lease a car for business purposes, you normally can’t recover 50 per cent of the VAT charged. The 50 per cent block is to cover the private use of the car. You can reclaim the remaining 50 per cent of the VAT charged. If you lease a qualifying car that you use exclusively for business purposes and not for private use, you can recover the input tax in full.

Filing under special circumstances

If you’re filing your first VAT return, your final return or a return with no payment, bear a few things in mind:

· First return: On your first return, you may want to reclaim VAT on money you spent prior to the period covered by your first VAT return. In general, you can recover VAT on capital and pre-start-up costs and expenses incurred before you registered for VAT as long as they’re VAT qualifying. For further help on this, refer to Notice 700: The VAT Guide, available from HM Revenue & Customs.

If you’re completing a VAT return for the first time, go to the HM Revenue & Customs website for help (www.hmrc.gov.uk) and/or speak with your accountant. You may be missing a trick in not reclaiming VAT on something you bought but didn’t reclaim the VAT on. More importantly, you may be reclaiming VAT on something that the tax authority doesn’t permit you to reclaim.

· Final return: For help with your final return, read Notice 700/11: Cancelling your registration. If you’ve any business assets, such as equipment, vehicles or stock on which you previously reclaimed VAT, you must include these items in your final VAT return. In effect, HM Revenue & Customs wants to recover this VAT (unless the amount is less than £1,000) in your last return.

As soon as your business circumstances change, you must inform HM Revenue & Customs, which has specified time limits, depending on the circumstances. If you ignore these time limits, you may incur penalties. If in doubt, contact the VAT helpline on 0845 010 9000.

· Nil return: You can file a nil return if you:

· Have not traded in the period covered by the VAT return and

· No VAT exists on purchases (inputs) to recover or

· No VAT exists on sales (outputs) to declare.

Complete all boxes on the return as ‘None’ on your paper-based return or ‘0.00’ on your electronic return.

Correcting mistakes

HM Revenue & Customs accepts the fact that people make mistakes (after all, we’re only human!) and it doesn’t expect perfection. However, it does have strict rules concerning mistakes. If you find a mistake on a previous return, you may be able to adjust your VAT account and include the value of that adjustment on your current VAT return. You can only do this if the mistake is found to be genuine and not deliberate, and is also below the error-correcting threshold (currently £10,000). If the amount is payable to HM Revenue & Customs, include it in the total for box 1 or box 2 (acquisitions). If the amount is repayable to you, include it in the total for box 4.

If you make a bigger mistake (the net value of the mistake is more than £10,000), do not include the amount on your current return. Inform your local VAT Business Advice Centre by letter or on form VAT 652: Voluntary disclosure of errors on VAT returns. The centre then issues a Notice of Voluntary Disclosure showing only the corrections to the period in question, and you become liable for the under-declared VAT and interest. Under these circumstances, no mis-declaration penalty is applied. Form Notice 700/45: How to correct VAT errors and make adjustments or claims helps you.

If you discover that an error has been made, you must disclose it to HM Revenue & Customs immediately. You cannot adjust these errors in a later VAT return.

Pursuing Payments and Repayments

Your completed VAT return results in one of two outcomes: you owe HM Revenue & Customs money or it owes you money - unless of course you complete a nil return, in which case you and HM Revenue & Customs are quits.

If you owe VAT but can’t afford to pay by the due date, still send in your completed VAT return, and then contact the Business Payment Support Service on 0300 200 3835. This service was set up on 24 November 2008 to meet the needs of businesses and individuals affected by the current economic downturn. You can discuss temporary options with the service, such as extending the period of payment.

If you’re owed money, you should receive a repayment about two weeks after you submit your VAT return. If after three weeks you haven’t received your repayment, contact the Customs and Excise National Advice Service on 0845 010 9000.

If your business is due a repayment of VAT on a regular basis and you’re on quarterly VAT returns, switch to monthly VAT returns at the earliest opportunity. Under a monthly system, you wait only two weeks for your VAT repayment rather than an additional two months.

If for any reason you receive a ‘Notice of assessment and/or over-declaration’ as a result of a mistake found by a visiting officer, don’t wait until your next VAT return to rectify the issue. If you owe VAT, send your payment and the remittance advice in the envelope provided. If HM Revenue & Customs owes you, suppress a large smile and pay in the cheque, or check your bank account if you normally pay electronically.