Bookkeeping & Accounting All-in-One For Dummies (2015)

Book II

Bookkeeping Day to Day

Chapter 2

Counting Your Sales

In This Chapter

![]() Taking in cash

Taking in cash

![]() Discovering the ins and outs of credit

Discovering the ins and outs of credit

![]() Managing discounts for best results

Managing discounts for best results

![]() Staying on top of returns and allowances

Staying on top of returns and allowances

![]() Monitoring payments due

Monitoring payments due

![]() Dealing with bad debt

Dealing with bad debt

Every business loves to take in money, and this means that you, the bookkeeper, have lots to do to ensure that sales are properly recorded in the books. In addition to recording the sales themselves, you must monitor customer accounts, discounts offered to customers, and customer returns and allowances.

If the business sells products on credit, you have to monitor customer accounts carefully in Trade Debtors (Accounts Receivable), including monitoring whether customers pay on time and alerting the sales team when customers are behind on their bills and future purchases on credit need to be declined. Some customers never pay, and in that case you must adjust the books to reflect non-payment as a bad debt.

This chapter reviews the basic responsibilities of a business’s bookkeeping and accounting staff for tracking sales, making adjustments to those sales, monitoring customer accounts and alerting management to slow-paying customers.

Collecting on Cash Sales

Most businesses collect some form of cash as payment for the goods or services they sell. Cash receipts include more than just notes and coins; you can consider cheques and credit- and debit-card payments as cash sales for bookkeeping purposes. In fact, with electronic transaction processing (when a customer’s credit or debit card is swiped through a machine), a deposit is usually made to the business’s bank account the same day (sometimes within seconds of the transaction, depending on the type of system the business sets up with the bank).

The only type of payment that doesn’t fall under the umbrella of a cash payment is purchases made on credit. And by credit, we mean the credit your business offers to customers directly rather than through a third party, such as a bank credit card or loan. We talk more about this type of sale in the section ‘Selling on Credit’, later in this chapter.

The only type of payment that doesn’t fall under the umbrella of a cash payment is purchases made on credit. And by credit, we mean the credit your business offers to customers directly rather than through a third party, such as a bank credit card or loan. We talk more about this type of sale in the section ‘Selling on Credit’, later in this chapter.

Discovering the value of sales receipts

Modern businesses generate sales receipts in one of three ways: by the cash register, by the credit- or debit-card machine or by hand (written out by the salesperson). Whichever of these three methods you choose to handle your sales transactions, the sales receipt serves two purposes:

· Gives the customer proof that the item was purchased on a particular day at a particular price in your shop in case she needs to exchange or return the merchandise.

· Gives the shop a receipt that can be used at a later time to enter the transaction into the business’s books. At the end of the day, the receipts are also used to cash up the cash register and ensure that the cashier has taken in the right amount of cash based on the sales made.

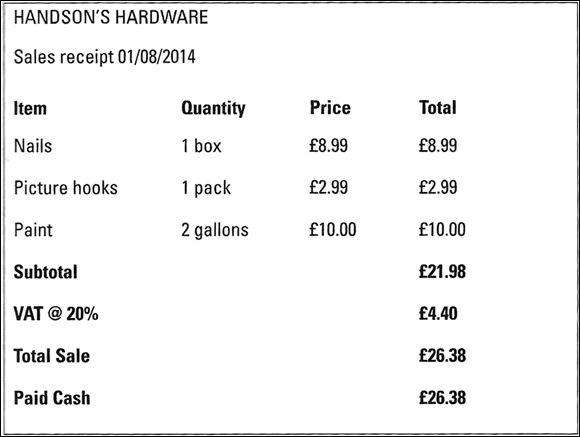

You’re familiar with cash receipts, no doubt, but just to show you how much useable information can be generated for the bookkeeper on a sales receipt, Figure 2-1 shows a sample receipt from a hardware shop.

Figure 2-1: A sales receipt from Handson’s Hardware.

Receipts contain a wealth of information that can be collected for your business’s accounting system. A look at a receipt tells you the amount of cash collected, the type of products sold, the quantity of products sold and how much value-added tax (VAT) was collected.

We’re assuming that your business operates some form of computerised accounting system, but it may be that you need to journal the sales information from your till into your accounting system (unless of course you have an automated process). Either way, as a reminder, the double entry required to enter your sales information is as follows:

|

Debit |

Credit |

|

|

Bank account |

£26.38 |

|

|

Sales |

£21.98 |

|

|

VAT Collected account |

£4.40 |

Sales receipts for 1 August 2014.

In this example entry, the Bank account is an Asset account shown on the Balance Sheet (see Book IV, Chapter 2 for more about the Balance Sheet), and its value increases with the debit. The Sales account is a Revenue account on the Profit and Loss statement (see Book IV, Chapter 1 for more about the Profit and Loss statement), and its balance increases with a credit, showing additional revenue. (We talk more about debits and credits in Book I, Chapter 2.) The VAT Collected account is a Liability account that appears on the Balance Sheet, and its balance increases with this transaction.

Businesses pay VAT to HM Revenue & Customs monthly or quarterly, depending on rules set by HM Revenue & Customs. Therefore, your business must hold the money owed in a Liability account so that you’re certain you can pay the VAT collected from customers when due. We talk more about VAT payments in Book III, Chapter 1.

Recording cash transactions in the books

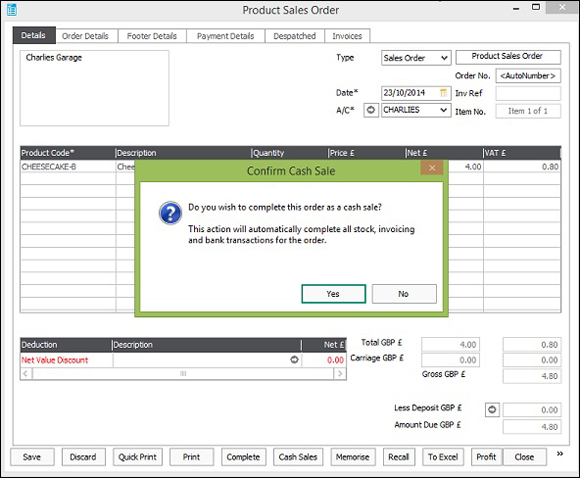

Assuming that you’re using a computerised accounting system, you can enter more detail from the day’s receipts and record stock sold as well. Most of the computerised accounting systems include the ability to record the sale of stock. Figure 2-2 shows you the Sage 50 Accounts Cash Sales screen that you can use to input data from each day’s sales. Note that you need the Sage 50 Accounts Professional version to use the Sales Order Processing function to generate cash sales and automatically update your stock.

Assuming that you’re using a computerised accounting system, you can enter more detail from the day’s receipts and record stock sold as well. Most of the computerised accounting systems include the ability to record the sale of stock. Figure 2-2 shows you the Sage 50 Accounts Cash Sales screen that you can use to input data from each day’s sales. Note that you need the Sage 50 Accounts Professional version to use the Sales Order Processing function to generate cash sales and automatically update your stock.

© Sage (UK) Limited. All rights reserved.

Figure 2-2: Example of a cash sale in Sage 50 Accounts.

Note: A cheaper computerised option would be to use Sage One Cashbook, or Sage One Accounts, which is an online accounting service, but cheap to use. It’s ideal for one-man bands and micro-businesses. Take a look at Sage One for Dummies by Jane Kelly (Wiley) to find out more.

In addition to the information included in the Cash Receipts book, note that Sage 50 Accounts also collects information about the items sold in each transaction. Sage 50 Accounts then automatically updates stock information, reducing the amount of stock on hand when necessary. If the cash sale in Figure 2-2 is for an individual customer, you enter her name and address in the A/C field. At the bottom of the Cash Sales screen, the Print tab takes you to a further menu where you have the option to print or email the receipt. You can print the receipt and give it to the customer or, for a phone or Internet order, email it to the customer. Using this option, payment can be made by any method such as cheque, electronic payment or credit or debit card.

Sage 50 Accounts also gives you the ability to process card payments from customers over the phone and use real-time authorisation and posting. To use Sage Pay, you need a Sage Pay account and a merchant bank account. For more information about this, please see www.sagepay.com.

If your business accepts credit cards, expect sales revenue to be reduced by the fees paid to credit card companies. Usually, you face monthly fees as well as fees per transaction; however, each business sets up individual arrangements with its bank regarding these fees. Sales volume impacts how much you pay in fees, so when researching bank services, ensure that you compare credit card transaction fees to find a good deal.

If your business accepts credit cards, expect sales revenue to be reduced by the fees paid to credit card companies. Usually, you face monthly fees as well as fees per transaction; however, each business sets up individual arrangements with its bank regarding these fees. Sales volume impacts how much you pay in fees, so when researching bank services, ensure that you compare credit card transaction fees to find a good deal.

Selling on Credit

Many businesses decide to sell to customers on credit, meaning credit that the business offers and not through a bank or credit card provider. This approach offers more flexibility in the type of terms you can offer your customers, and you don’t have to pay bank fees. However, credit involves more work for you, the bookkeeper, and the risk of a customer not paying what she owes.

When you accept a customer’s bank-issued credit card for a sale and the customer doesn’t pay the bill, you get your money; the bank is responsible for collecting from the customer, taking the loss if she doesn’t pay. This doesn’t apply when you decide to offer credit to your customers directly. If a customer doesn’t pay, your business takes the loss.

Deciding whether to offer credit

The decision to set up your own credit system depends on what your competition is doing. For example, if you run an office supply store and all other office supply stores allow credit to make it easier for their customers to get supplies, you probably need to offer credit to stay competitive.

You need to set up some ground rules when you want to allow your customers to buy on credit. For personal customers, you have to decide

· How to check a customer’s credit history

· What the customer’s income level needs to be for credit approval

· How long to give the customer to pay the bill before charging interest or late fees

If you want to allow your trade or business customers to buy on credit, you need to set ground rules for them as well. The decisions you need to make include:

· Whether to deal only with established businesses. You may decide to give credit only to businesses that have been trading for at least two years.

· Whether to require trade references, which show that the business has been responsible and paid other businesses when they’ve taken credit. A customer usually provides you with the details of two suppliers that offered her credit. You then contact those suppliers directly to see whether the customer has been reliable and on time with payments.

· Whether to obtain credit rating information. You may decide to use a third-party credit-checking agency to provide a credit report on the business applying for credit. This report suggests a maximum credit limit and whether the business pays on time. Of course a fee is charged for this service, but using it may help you avoid making a terrible mistake. Asimilar service is available for individuals.

The harder you make getting credit and the stricter you make the bill-paying rules, the less chance you have of taking a loss. However, you may lose customers to a competitor with lighter credit rules.

You may require a minimum income level of £50,000 and make customers pay in 30 days to avoid late fees or interest charges. Your sales staff report that these rules are too rigid because your direct competitor down the street allows credit on a minimum income level of £30,000 and gives customers 60 days to pay before charging late fees and interest charges. Now you have to decide whether you want to change your credit rules to match those of the competition. If you do lower your credit standards to match your competitor, however, you may end up with more customers who can’t pay on time (or at all) because you’ve qualified customers for credit at lower income levels and given them more time to pay. If you do loosen your qualification criteria and bill-paying requirements, monitor your customer accounts carefully to ensure that they’re not falling behind.

You may require a minimum income level of £50,000 and make customers pay in 30 days to avoid late fees or interest charges. Your sales staff report that these rules are too rigid because your direct competitor down the street allows credit on a minimum income level of £30,000 and gives customers 60 days to pay before charging late fees and interest charges. Now you have to decide whether you want to change your credit rules to match those of the competition. If you do lower your credit standards to match your competitor, however, you may end up with more customers who can’t pay on time (or at all) because you’ve qualified customers for credit at lower income levels and given them more time to pay. If you do loosen your qualification criteria and bill-paying requirements, monitor your customer accounts carefully to ensure that they’re not falling behind.

The key risk you face is selling products for which you’re never paid. For example, if you allow customers 30 days to pay and cut them off from buying goods when their accounts fall more than 30 days behind, the most you can lose is the amount purchased over a two-month period (60 days). But if you give customers more leniency, allowing them 60 days to pay and cutting them off after payment is 30 days late, you’re faced with three months (90 days) of purchases for which you may never be paid.

Recording credit sales in the books

When sales are made on credit, you have to enter specific information into the accounting system. In addition to inputting information regarding cash receipts (see ‘Collecting on Cash Sales’, earlier in this chapter), you update the customer accounts to make sure that each customer is billed and the money is collected. You debit the Trade Debtors account, an Asset account shown on the Balance Sheet (see Book IV, Chapter 2), which shows money due from customers.

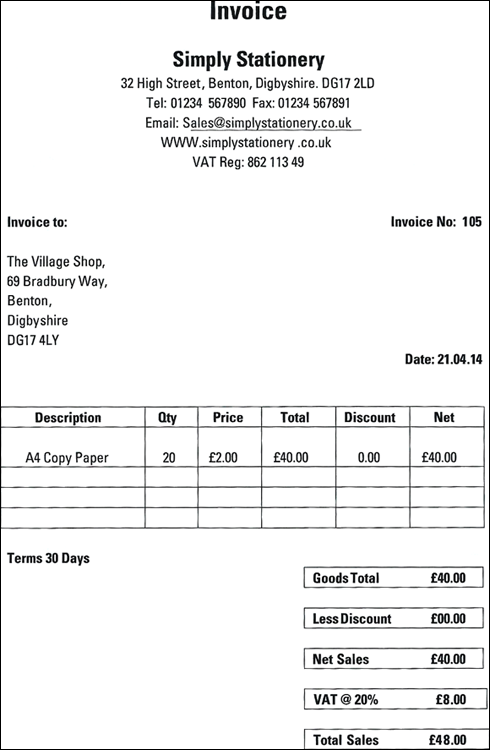

Figure 2-3 shows an example of a sales invoice from Simply Stationery.

Figure 2-3: A sales invoice from Simply Stationery.

When the bookkeeper for Simply Stationery enters this invoice, whether on a computer or in manual ledgers, the journal entry for a credit sale would look like this:

|

Debit |

Credit |

|

|

Trade Debtors |

£48.00 |

|

|

Sales |

£40.00 |

|

|

VAT account |

£8.00 |

A computerised accounting system makes this journal entry automatically, but you still need to know what the bookkeeping entries are, just in case you need to correct something. In addition to making this journal entry, your accounts package will enter the information into the customer’s account so that accurate statements can be sent out at the end of the month.

When the customer pays the bill, you update the individual customer’s record to show that payment has been received. Sage 50 Accounts automatically enters the following into the bookkeeping records:

|

Debit |

Credit |

|

|

Trade Debtors |

£48.00 |

|

|

Cash |

£48.00 |

Payment from The Village Shop

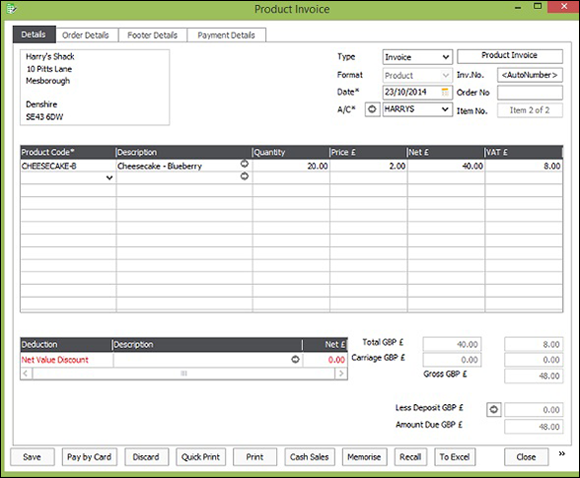

If you’re using Sage 50 Accounts, you can enter credit sales on an invoice like the one in Figure 2-4.

© Sage (UK) Limited. All rights reserved.

Figure 2-4: Creating a sales invoice using Sage 50 Accounts for goods sold on credit.

Sage 50 Accounts uses the information on the invoice to update the following accounts:

· Trade Debtors

· Stock

· Customer’s

· VAT

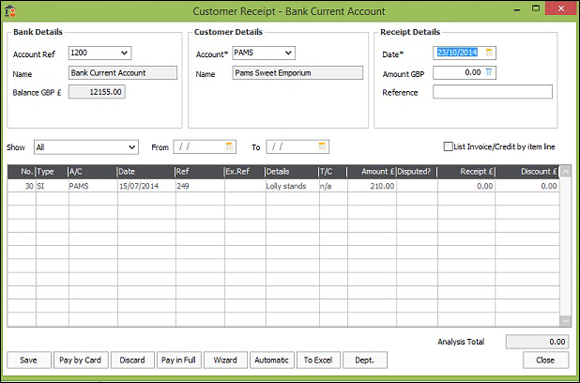

Print out the invoice and send it to the customer straight away. Depending on the payment terms you’ve negotiated with your customers, send out monthly statements to remind customers that their debt to your company is still outstanding. Regular monitoring of your Aged Debtor report ensures that you know who has not yet paid you. In order to keep these reports up to date, allocate the cash to each customer account on a regular basis.

When you receive payment from a customer, here’s what to do:

1. From the Bank module, click the Customer icon and select the customer account.

2. Sage 50 Accounts automatically lists all outstanding invoices. (See Figure 2-5.)

3. Enter how much the customer is paying in total.

4. Select the invoice or invoices paid.

5. Sage 50 Accounts updates the Trade Debtors account, the Cash account and the customer’s individual account to show that payment has been received.

© Sage (UK) Limited. All rights reserved.

Figure 2-5: In Sage 50 Accounts, recording payments from customers who bought on credit starts with the Customer Receipt screen.

If your customer is paying a lot of outstanding invoices, Sage 50 Accounts has two clever options that may save you some time. The first option, Pay in Full, marks every invoice as paid if the customer is settling up in full. The other option, Wizard, matches the payment to the outstanding invoices by starting with the oldest until it matches up the exact amount of the payment.

If your business uses a point-of-sale program integrated into the computerised accounting system, recording credit transactions is even easier for you. Sales details feed into the system as each sale is made, so that you don’t have to enter the detail at the end of the day. These point-of-sale programs save a lot of time, but they can get really expensive.

Even if customers don’t buy on credit, point-of-sale programs provide businesses with an incredible amount of information about their customers and what they like to buy. This data can be used in the future for direct marketing and special sales to increase the likelihood of return business.

Cashing Up the Cash Register

To ensure that cashiers don’t pocket a business’s cash, at the end of each day cashiers must cash up (show that they’ve the right amount of cash in the register based on the sales transactions during the day) the amount of cash, cheques and credit sales they took in during the day.

This process of cashing up a cash register actually starts at the end of the previous day, when cashier John Smith and his manager agree on the amount of cash left in John’s register drawer. They record cash sitting in cash registers or cash drawers as part of the Cash in Hand account.

When John comes to work the next morning, he starts out with the amount of cash left in the drawer. At the end of the business day, he or his manager run a summary of activity on the cash register for the day to produce a report of the total sales taken in by the cashier. John counts the amount of cash in his register as well as totals for the cheques, credit card receipts and credit account sales. He then completes a cash-out form that looks something like Table 2-1:

Table 2-1 Cash Register: John Smith, 25/4/2014

|

Receipts |

Sales |

Total |

|

Opening Cash |

£100 |

|

|

Cash Sales |

£400 |

|

|

Credit Card Sales |

£800 |

|

|

Credit Account Sales |

£200 |

|

|

Total Sales |

£1,400 |

|

|

Sales on Credit |

£1,000 |

|

|

Cash Received |

£400 |

|

|

Total Cash in Register |

£500 |

A manager reviews John Smith’s cash register summary (produced by the actual register) and compares it to the cash-out form. If John’s ending cash (the amount of cash remaining in the register) doesn’t match the cash-out form, he and the manager try to pinpoint the mistake. If they can’t find a mistake, they fill out a cash-overage or cash-shortage form. Some businesses charge the cashier directly for any shortages, whereas others take the position that the cashier’s fired after a certain number of shortages of a certain amount (say, three shortages of more than £10).

The manager decides how much cash to leave in the cash drawer or register for the next day and deposits the remainder. He carries out this task for each of his cashiers and then deposits all the cash and cheques from the day in a night-deposit box at the bank. He sends a report with details of the deposit to the bookkeeper so that the data appears in the accounting system. The bookkeeper enters the data on the Cash Sales screen (refer to Figure 2-2) if a computerised accounting system is being used, or into the Cash Receipts book if the books are being kept manually.

Monitoring Sales Discounts

Most businesses offer discounts at some point in time to generate more sales. Discounts are usually in the form of a sale with 10 per cent, 20 per cent or even more off purchases.

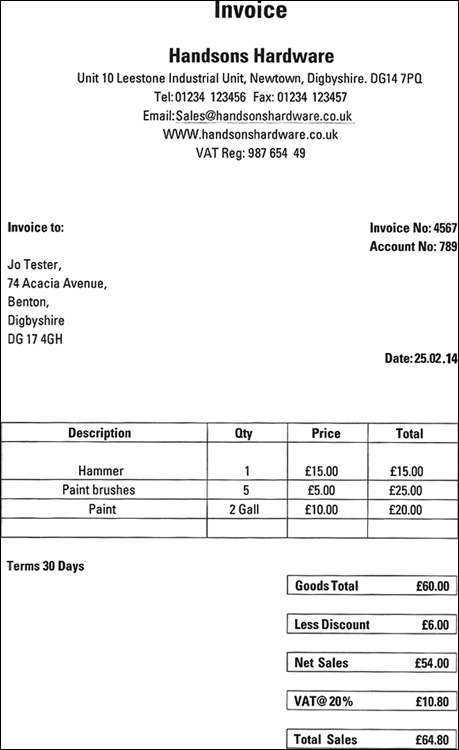

When you offer discounts to customers, monitor your sales discounts in a separate account so that you can keep an eye on how much you discount sales each month. If you find that you’re losing more and more money to discounting, look closely at your pricing structure and competition to find out why you’re having to lower your prices frequently to make sales. You can monitor discount information easily by using the data found on a standard sales invoice. Figure 2-6 shows an invoice from Handson’s Hardware, which shows a discount.

Figure 2-6: A sales invoice from Handson’s Hardware showing a sales discount.

From this example, you can see clearly that the business takes in less cash when discounts are offered. When recording the sale in the Cash Receipts book, you record the discount as a debit. This debit increases the Sales Discount account, which the bookkeeper subtracts from the Sales account to calculate the net sales. (We walk you through all these steps and calculations when we discuss preparing the Profit and Loss statement in Book IV, Chapter 1.) Here’s what the bookkeeping entry would look like for Handson’s Hardware. Remember, if you’re using a computerised accounting system, this double entry is done automatically as you post the invoice onto the system.

|

Debit |

Credit |

|

|

Bank account |

£64.80 |

|

|

Sales Discounts |

£6.00 |

|

|

Sales |

£60.00 |

|

|

VAT |

£10.80 |

Sales invoice no. 4567

If you use Sage 50 Accounts, you can add the sales discount as a line item on the sales receipt or invoice, and the system automatically adjusts the sales figures and updates your Sales Discount account.

Recording Sales Returns and Allowances

Most businesses deal with sales returns on a regular basis. Customers regularly return purchased items because the item is defective, they change their minds or for other reasons. Instituting a no-return policy is guaranteed to produce unhappy customers: ensure that you allow sales returns in order to maintain good customer relations.

Accepting sales returns can be a complicated process. Usually, a business posts a set of rules for returns that may include:

· Returns are allowed only within 30 days of purchase.

· You must have a receipt to return an item.

· When you return an item without a receipt, you can receive only a credit note.

You can set up whatever rules you want for returns. For internal control purposes, the key to returns is monitoring how your staff handle them. In most cases, ensure that a manager’s approval is required on returns. Also, make sure that your employees pay close attention to how the customer originally paid for the item being returned. You certainly don’t want to give a customer cash when she used credit - you’re just handing over your money! After a return’s approved, the cashier returns the amount paid by cash or credit card. Customers who bought the items on credit don’t get any money back, because they didn’t pay anything but expected to be billed later. Instead, a form is filled out so that the amount of the original purchase can be subtracted from the customer’s credit account.

You use the information collected by the cashier who handled the return to input the sales return data into the books. For example, a customer returns an item worth £47 that was purchased with cash. You record the cash refund in the Cash Receipts book like this:

|

Debit |

Credit |

|

|

Sales Returns and Allowances |

£39.17 |

|

|

VAT @ 20% |

£7.83 |

|

|

Bank account |

£47.00 |

To record return of purchase

If the item was bought with a discount, you list the discount as well and adjust the price to show that discount.

In this journal entry:

· The Sales Returns and Allowances account increases. This account normally carries a debit balance and is subtracted from the Sales account when preparing the Profit and Loss statement, thereby reducing revenue received from customers.

· The debit to the VAT account reduces the amount in that account because VAT is no longer due on the purchase.

· The credit to the Bank account reduces the amount of cash in that account.

Sales allowances (sales incentive programmes) are becoming more popular with businesses. Sales allowances are most often in the form of a gift card. A sold gift card is actually a liability for the business because the business has received cash, but no merchandise has gone out. For that reason, gift card sales are entered in the Gift Card Liability account. When a customer makes a purchase at a later date using the gift card, the Gift Card Liability account is reduced by the purchase amount. Monitoring the Gift Card Liability account allows businesses to keep track of how much is yet to be sold without receiving additional cash.

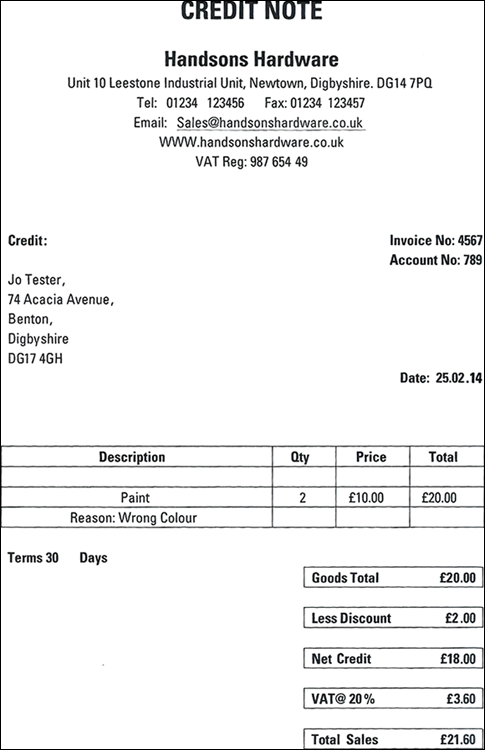

A business that sells goods on credit and then subsequently receives the goods back needs to raise a sales credit note within their accounting system to reverse the effect of the sales invoice that has already been generated.

Figure 2-7 shows an example of a credit note that’s been raised by Handson’s Hardware, because the paint that was delivered was the wrong colour. The customer has returned the paint but needs a refund against her account.

Figure 2-7: An example of a credit note raised, annotated with the double-entry transactions.

The double entry that occurs when a credit note is raised and entered into an accounting system is as follows:

|

Debit |

Credit |

|

|

Sales Return account |

£18.00 |

|

|

VAT account |

£3.60 |

|

|

Debtors account |

£21.60 |

Credit Note dated 25.02.14 to Jo Tester

Monitoring Trade Debtors

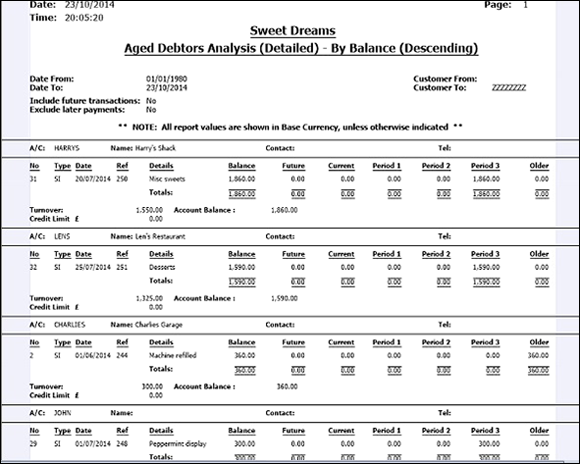

Making sure that customers pay their bills is a crucial responsibility of the bookkeeper. Before sending out the monthly bills, you should run an Aged Debtor report, which lists all customers who owe money to the business and the age of each debt, as shown in Figure 2-8.

Figure 2-8: An Aged Debtor report using Sage 50 software.

The Aged Debtor report quickly tells you which customers are behind in their bills. In this example, customers are put on stop when their payments are more than 60 days late, so all the accounts shown, with the exception of the John account, should be put on stop, until the invoices are paid and their accounts are brought up to date.

Give a copy of your Aged Debtor report to the sales manager so she can alert staff to problem customers. The sales manager can also arrange for the appropriate collections procedures. Each business sets up its own specific collections process, usually starting with a phone call, followed by letters and possibly legal action, if necessary.

Accepting Your Losses

You may encounter a situation in which a customer never pays your business, even after an aggressive collections process. In this case, you’ve no choice but to write off the purchase as a bad debt and accept the loss.

Most businesses review their Aged Debtor reports every 6 to 12 months and decide which accounts need to be written off as bad debt. Accounts written off are recorded in a Nominal Ledger account called Bad Debt. (See Book I, Chapter 4 for more information about the Nominal Ledger.) The Bad Debt account appears as an Expense account on the Profit and Loss statement. When you write off a customer’s account as bad debt, the Bad Debt account increases and the Trade Debtors account decreases.

To give you an idea of how you write off an account, assume that one of your customers never pays £105.75 due. Here’s what your journal entry looks like for this debt:

|

Debit |

Credit |

|

|

Bad Debt |

£105.75 |

|

|

Trade Debtors |

£105.75 |

Sage 50 Accounts has a wizard that helps you write off individual transactions as a bad debt and does all the double entry for you, so you don’t need to worry!

If the bad debt included VAT, you’ve suffered a double loss because you’ve paid over the VAT to HM Revenue & Customs, even though you never received it. Fortunately, you can reclaim this VAT when you do your next VAT return.

Have a Go

The rest of this chapter gives you extra practice on double-entry bookkeeping, so that you’re able to carry out adjustments to the accounts if you need to. More importantly, it means that you’ll understand what your computerised accounting system is doing in the background every time you post an entry.

It may be worthwhile referring back to the golden rules of bookkeeping mentioned in Book I, Chapter 2. You see, sticking the rules up on your wall doesn’t seem so daft now, does it?!

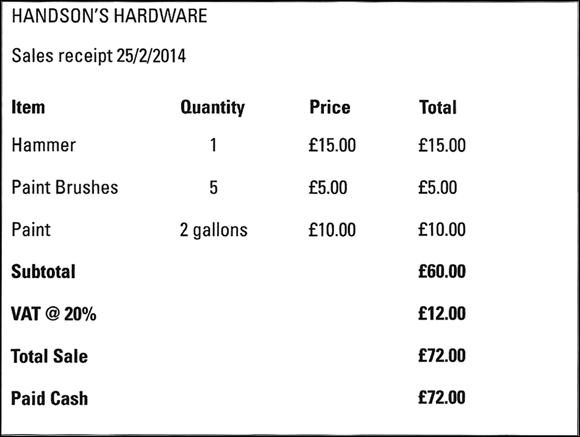

1. Take a look at the sales receipt in Figure 2-9. How would you record this transaction in your books, if you were the bookkeeper for a hardware business?

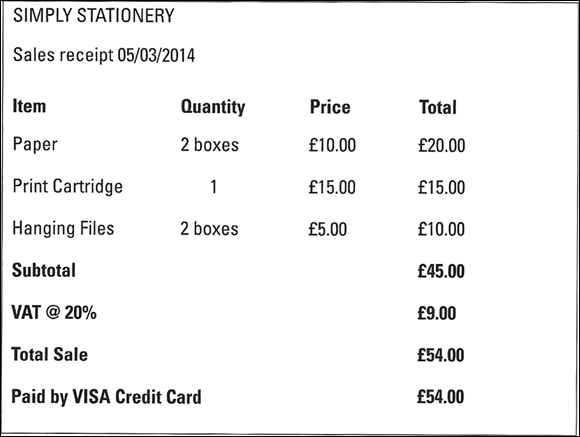

2. Looking at the sales receipt in Figure 2-10, how would you record this transaction in your books, if you were a bookkeeper for this office supply business?

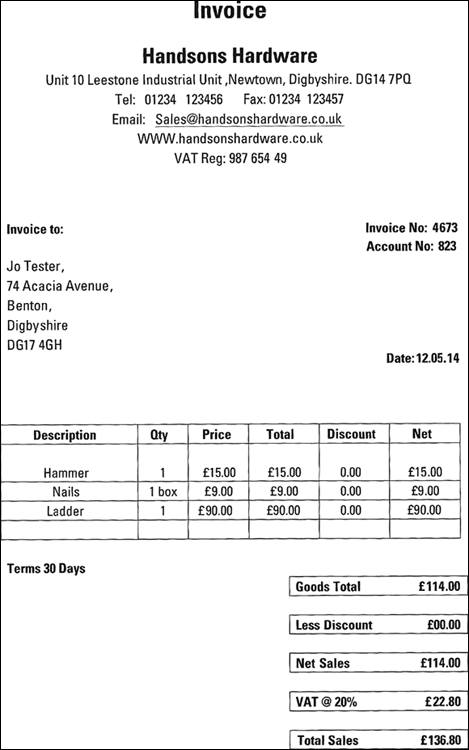

3. Using the invoice shown in Figure 2-11, how would you record this credit transaction in your books, if you were the bookkeeper for Handson’s Hardware?

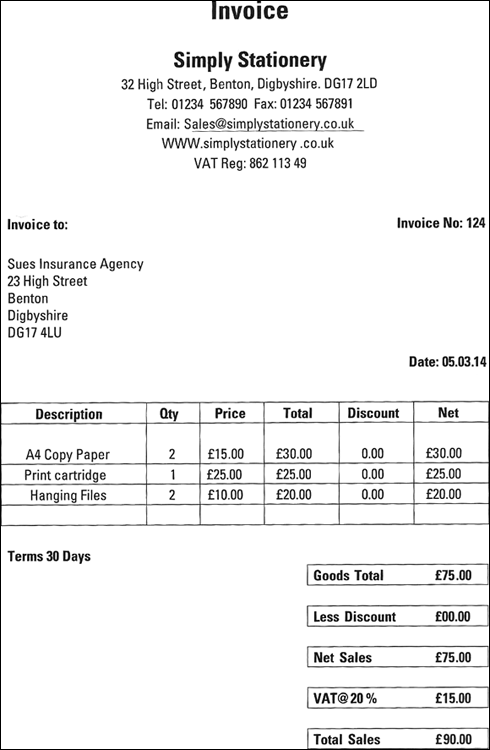

4. Using the invoice shown in Figure 2-12, how would you record this credit transaction in your books, if you were a bookkeeper for this office supply business?

5. Use the information in the cash register summary that follows to complete the blank cash summary form. Also, assume that the cash register had £100 at the beginning of the day and £426 at the end of the day. Is there a difference between how much should be in the register and how much is actually in there?

Cash Register Summary for Jane Doe on 15/3/2014

|

Item |

Quantity |

Price |

Total |

|

|

Paper |

20 boxes |

£15.00 |

£300.00 |

|

|

Print cartridges |

10 |

£25.00 |

£250.00 |

|

|

Envelopes |

10 boxes |

£7.00 |

£70.00 |

|

|

Pens |

20 boxes |

£8.00 |

£160.00 |

|

|

Subtotal |

£780.00 |

|||

|

VAT @ 20 % |

£156.00 |

|||

|

Total cash sales |

£336.00 |

|||

|

Total credit card sales |

£200.00 |

|||

|

Total credit account sales |

£400.00 |

|||

|

Total sales |

£936.00 |

Cash Register: _____ Date: _____

|

Receipts |

Sales |

Cash in Register |

|

Beginning cash |

_____ |

|

|

Cash sales |

_____ |

|

|

Credit card sales |

_____ |

|

|

Credit account sales |

_____ |

|

|

Total sales |

_____ |

|

|

Minus credit sales |

_____ |

|

|

Total cash received |

_____ |

|

|

Total cash that should be in register |

_____ |

|

|

Actual cash in register |

_____ |

|

|

Difference |

_____ |

6. How would you record the following transaction in your books, if you were a bookkeeper for an office supply business? Design a sales invoice using the information supplied and show the bookkeeping transactions. Be as creative as you like with the name and address of the office supply business. Use the examples of previous sales invoices shown in Figures 2-3 and 2-6 to help you with the design of the invoice.

Sales Receipt for 05/03/2014

|

Item |

Quantity |

Price |

Total |

|

Paper |

2 boxes |

£15.00 |

£30.00 |

|

Print cartridge |

1 |

£15.00 |

£15.00 |

|

Hanging files |

2 boxes |

£5.00 |

£10.00 |

|

Subtotal |

£55.00 |

||

|

Sales discount @ 20% |

£11.00 |

||

|

Sales after discount |

£44.00 |

||

|

VAT @ 20% |

£8.80 |

||

|

Total cash sale |

£52.80 |

7. How would you record the following credit transaction in your books, if you were a bookkeeper for this office supply business?

Sales Summary for 05/03/2014

|

Item |

Quantity |

Price |

Total |

|

Paper |

10 boxes |

£15.00 |

£150.00 |

|

Print cartridges |

5 |

£15.00 |

£75.00 |

|

Hanging files |

7 boxes |

£5.00 |

£35.00 |

|

Envelopes |

10 boxes |

£7.00 |

£70.00 |

|

Pens |

20 boxes |

£8.00 |

£160.00 |

|

Subtotal |

£490.00 |

||

|

Sales discount @ 20% |

£98.00 |

||

|

Sales after discount |

£392.00 |

||

|

VAT @ 20% |

£78.40 |

||

|

Total cash sales |

£145.40 |

||

|

Total credit card sales |

£150.00 |

||

|

Total credit account sales |

£175.00 |

||

|

Total sales |

£470.40 |

8. A customer returns a pair of trousers she bought for £35 using a credit card. She has a receipt showing when she made the original purchase. The rate of VAT is 20 per cent. How would you record this transaction in the books?

9. On 15 December, Jean Jones, a customer of Simply Stationery, returns a filing cabinet she bought on 1 December for £75 on credit. She’s already been issued with a sales invoice, but hasn’t paid for it yet. Design a credit note for this transaction and state how you’d record the transaction in the books.

Note: The rate of VAT is 20 per cent.

10. You discover, after compiling your Aged Debtors report for 30 June 2014, that you’ve an account that’s more than six months past due for a total of £125.65. Your company policy is that you write off bad debt when an account is more than six months late. How would you record this transaction in your books?

Figure 2-9: Sales Receipt for Handson’s Hardware on 25/2/2014.

Figure 2-10: Sales Receipt for Simply Stationery on 05/03/2014.

Figure 2-11: Sales invoice for Handson’s Hardware.

Figure 2-12: Sales invoice for Simply Stationery.

Answering the Have a Go Questions

1. Handson’s Hardware would record the sales receipts transactions as follows:

|

Debit |

Credit |

|

|

Bank account |

£72.00 |

|

|

Sales |

£60.00 |

|

|

VAT |

£12.00 |

2. Cash receipts for 25/2/2014

3. Simply Stationery would record the sales receipts information as follows:

|

Debit |

Credit |

|

|

Bank account |

£54.00 |

|

|

Sales |

£45.00 |

|

|

VAT |

£9.00 |

4. Cash receipts for 05/03/14

5. You’d record the sales invoice details as follows:

|

Debit |

Credit |

|

|

Debtors |

£136.80 |

|

|

Sales |

£114.00 |

|

|

VAT |

£22.80 |

6. Credit receipts for 12/05/2014

7. You’d record the sales invoice details as follows:

|

Debit |

Credit |

|

|

Debtors |

£90.00 |

|

|

Sales |

£75.00 |

|

|

VAT |

£15.00 |

8. Credit receipts for 05/03/2014

9. Here’s how you’d complete the cash-out form.

Cash Register: Jane Doe, 15/3/2014

|

Receipts |

Sales |

Cash in Register |

|

Beginning cash |

£100.00 |

|

|

Cash sales |

£336.00 |

|

|

Credit card sales |

£200.00 |

|

|

Business credit sales |

£400.00 |

|

|

Total sales |

£936.00 |

|

|

Minus sales on credit |

(£600.00) |

|

|

Total cash received |

£336.00 |

|

|

Total cash that should be in register |

£436.00 |

|

|

Actual cash in register |

£426.00 |

|

|

Difference |

Shortage of £10.00 |

The manager would need to investigate why the till was down by £10.

10. You can use Figures 2-3 and 2-6 to guide you in designing your invoice for these transactions.

The bookkeeping entry is as follows:

|

Debit |

Credit |

|

|

Bank account |

£52.80 |

|

|

Sales Discount |

£11.00 |

|

|

Sales |

£55.00 |

|

|

VAT |

£8.80 |

Cash receipts for 05/03/14

11. The entry would be:

|

Debit |

Credit |

|

|

Bank account |

£295.40 |

|

|

Debtors |

£175.00 |

|

|

Sales Discount |

£98.00 |

|

|

Sales |

£490.00 |

|

|

VAT |

£78.40 |

12. Cash receipts for 05/03/14

13. The entry would be:

|

Debit |

Credit |

|

|

Sales Returns and Allowance |

£29.17 |

|

|

VAT |

£5.83 |

|

|

Bank account |

£35.00 |

14. Even though the customer is receiving a credit on her credit card, you show this refund by crediting your Bank account. Remember, when a customer uses a credit card, the card is processed by the bank and cash is deposited in the business’s bank account.

15. The double-entry bookkeeping would be:

|

Debit |

Credit |

|

|

Sales Returns and Allowances |

£60.00 |

|

|

VAT |

£15.00 |

|

|

Debtors |

£75.00 |

16. The entry would look like this:

|

Debit |

Credit |

|

|

Bad Debt |

£125.65 |

|

|

Debtors |

£125.65 |

17. Accounts written off for bad debt as at 30/06/14