Bookkeeping & Accounting All-in-One For Dummies (2015)

Book I

Basic Bookkeeping

Chapter 4

Looking at Ledgers

In This Chapter

![]() Understanding the value of the Nominal Ledger

Understanding the value of the Nominal Ledger

![]() Developing ledger entries

Developing ledger entries

![]() Posting entries to the ledger accounts

Posting entries to the ledger accounts

![]() Adjusting ledger entries

Adjusting ledger entries

In this chapter, we discuss the accounting ledgers. You meet the Sales Ledger, Purchase Ledger and Cashbook and discover how they interact with the Nominal Ledger. We tell you how to develop entries for the ledger and also how to enter (or post) them from the original sources. In addition, we explain how you can change already posted information or correct entries in the Nominal Ledger.

The most common ledgers include:

· Sales Ledger: This tracks day-to-day sales, and contains the accounts of debtors (customers).

· Purchases Ledger: This tracks day-to-day purchases, and contains the accounts of creditors (suppliers).

· Nominal Ledger: Sometimes called the General Ledger, this ledger is used for all the remaining accounts, such as income and expense accounts as well as including the Purchase Ledger account balance and the Sales Ledger account balance. There are also accounts for items such as stock, value-added tax (VAT) and loans. The Nominal Ledger basically contains all the transactions that a business has ever made.

· Cashbook: This tracks the daily use of cash.

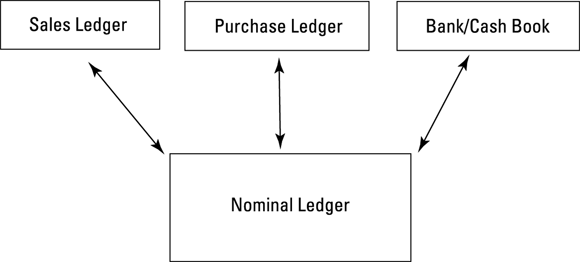

If you’re using a computerised accounting system, your ledgers are integrated (see Figure 4-1). This means that as you enter transactions into, say, your Sales Ledger, the Nominal Ledger is automatically updated. The same applies to entries that are made via your Cashbook or Purchase Ledger.

Your computerised system follows the principles of double-entry bookkeeping; so for every debit, you have a corresponding credit.

Figure 4-1: Showing how all ledgers are integrated in a computerised system.

Keeping watch: The eyes and ears of a business

The Nominal Ledger serves as the figurative eyes and ears of bookkeepers and accountants who want to know what financial transactions have taken place historically in a business. By reading the Nominal Ledger - not exactly interesting reading unless you love numbers - you can see, account by account, every transaction that has taken place in the business.

The Nominal Ledger is the master summary of your business. You can find all the transactions that ever occurred in the history of the business in the Nominal Ledger account. In just one place you can find transactions that impact Cash, Stock, Trade Debtors (Accounts Receivable), Trade Creditors (Accounts Payable) and any other account included in your business’s Chart of Accounts. (See Book I, Chapter 3 for more information about setting up the Chart of Accounts and the kinds of transactions you can find in each account.)

Developing Entries for the Ledger

In the next section, we take you through the process of entering transactions on each of the ledgers, and we look at the bookkeeping entries for all transactions. You can practise your double-entry bookkeeping at the end of this chapter, in the ‘Have a Go’ section. Because most people now use computerised accounting systems, we demonstrate the types of reports and documents that you can run off to prove your transactions. We use Sage 50 to demonstrate these reports.

You enter your transactions using source documents or other data. Source documents tend to be the following:

· Sales invoices (unless automatically generated from your accounts program)

· Sales credit notes

· Purchase invoices from your suppliers

· Purchase credit notes

· Cheque payments

· Cash receipts (from your paying-in book)

· Remittance advice slips received from customers, which usually accompany the cheque or BACs receipt confirmation

· Bank statements (to pick up other bank payments and receipts)

Posting Sales Invoices

Have a look at the bookkeeping that occurs when you post some sales invoices. Assume that the invoices aren’t paid straight away; they’re credit sales.

Using the double-entry bookkeeping rules from Book I, Chapter 2, you know the following:

Using the double-entry bookkeeping rules from Book I, Chapter 2, you know the following:

If you want to record income, you credit the Income account.

If you want to increase an asset, you debit the Asset account.

So, if you raise an invoice for £200 (ignoring VAT for the moment), then the following bookkeeping takes place:

|

Debit |

Credit |

|

|

Debtors |

£200 |

|

|

Sales |

£200 |

Every time you post a sales invoice, this same double entry takes place.

A computerised accounting system does the double entry for you, but you still need to understand the bookkeeping rules, so that you can create journals if corrections are necessary at any point in the future. See the section ‘Adjusting for Nominal Ledger Errors’, later in this chapter.

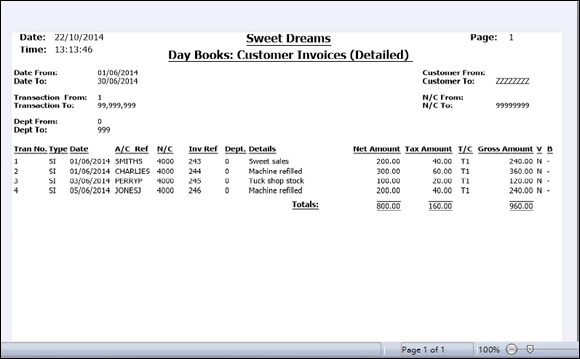

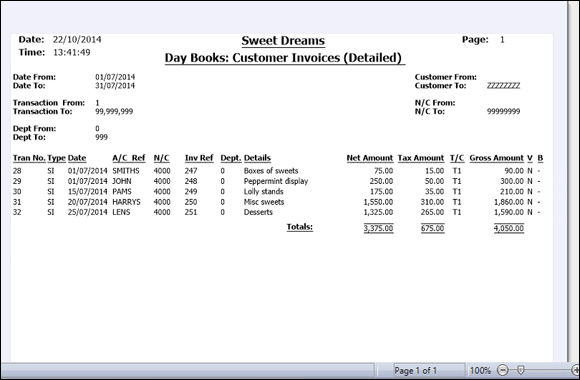

In Figure 4-2, we show you the Customer Invoices Daybook for Sweet Dreams (a fictitious company). This daybook simply provides a list of sales invoices that have been entered in Sage. If you were still operating a manual system, the same information would be reflected in the Sales journal.

In Figure 4-2, we show you the Customer Invoices Daybook for Sweet Dreams (a fictitious company). This daybook simply provides a list of sales invoices that have been entered in Sage. If you were still operating a manual system, the same information would be reflected in the Sales journal.

Figure 4-2: Showing the Customer Invoices Daybook.

Make sure that you understand the bookkeeping here: you make the following double entry based on the information shown in the Customer Invoice Daybook as shown in Figure 4-2:

|

Account |

Debit |

Credit |

|

Trade Debtors |

£960 |

|

|

Sales |

£800 |

|

|

VAT |

£160 |

Note that this entry is balanced. You increase the Trade Debtors account to show that customers owe the business money because they bought items on credit. You increase the Sales account to show that even though no cash changed hands, the business in Figure 4-2 took in revenue. You collect cash when the customers pay their bills.

You give each transaction a reference to its original source point. For example, the first invoice listed for Smith’s account has the invoice reference 243. If you went to the sales invoice file and found invoice no. 243, you’d have the original source of the transaction in your hands. This is very useful when it comes to customer queries, because you can immediately locate the invoice and check the details.

You give each transaction a reference to its original source point. For example, the first invoice listed for Smith’s account has the invoice reference 243. If you went to the sales invoice file and found invoice no. 243, you’d have the original source of the transaction in your hands. This is very useful when it comes to customer queries, because you can immediately locate the invoice and check the details.

As an aside, Sage 50 also gives each transaction a unique transaction number. It’s the first number in the first column of each report. If you need to make a correction to a transaction, this number is the way you’d identify that specific transaction and be able to amend it.

Posting Purchase Invoices

Your business needs to account for the invoices received from its suppliers. Often, you won’t pay these invoices straight away, so you post them into the Creditors Ledger (sometimes known as the Suppliers Ledger).

Using the double-entry rules as discussed in Book I, Chapter 2, you then get the following double entry:

To increase a liability, you credit the Liabilities account.

If you want to increase an asset, you debit the Asset account.

Because you’re recording a liability when you post invoices that you owe money for, you credit the Creditors Ledger. Hence, you must make the opposite debit entry to the Nominal account to which the invoice has been coded; for example, Materials Purchased.

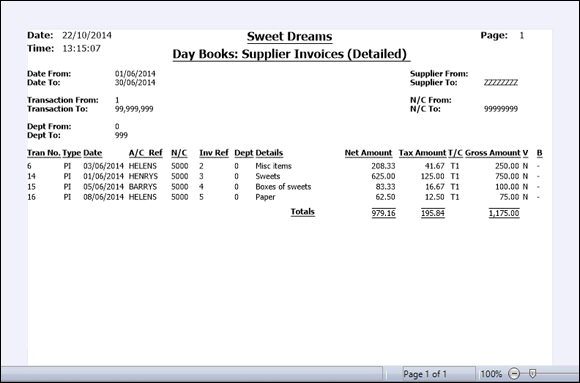

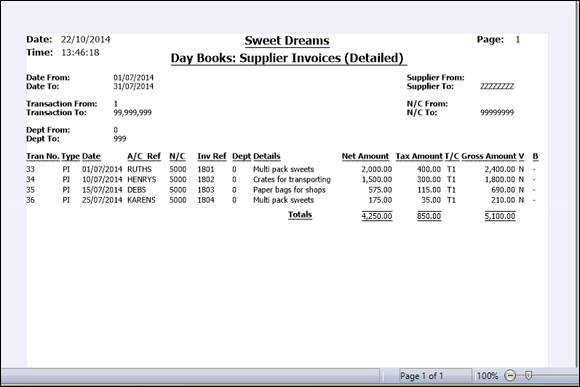

Have a look at some purchase invoices that have been entered for Sweet Dreams. See Figure 4-3.

Figure 4-3: Supplier Invoices Daybook for Sweet Dreams.

In Figure 4-3 Sweet Dreams has posted four purchase invoices for the gross value of £1,175.

Because this report is a Sage daybook report, you can see the nominal code that Sweet Dreams’s bookkeeper, Kate, used when she entered the invoices. In this case, 5000 is the nominal code used for all invoices, which happens to be the nominal code for the Materials Purchased account.

So, the double entry that Kate made for these combined transactions is as follows:

|

Account |

Debit |

Credit |

|

Materials Purchased |

£979.16 |

|

|

VAT |

£195.84 |

|

|

Creditors Ledger |

£1,175.00 |

Like the entry for the Sales account, this entry is balanced. The Trade Creditors account is increased to show that money is due to suppliers, and the Materials Purchased account is also increased to show that more supplies were purchased.

Note: An invoice reference number is shown on the daybook report. This relates to the sequential invoice number given to each purchase invoice. For example, the invoice posted for Henry’s has a reference of 3. If you were to select the purchase invoice file and locate invoice number 3, you’d find the original purchase invoice for Henry’s. This is especially important in the event of a supplier query. It provides an easy method of locating the exact invoice.

Entering Items into the Nominal Ledger

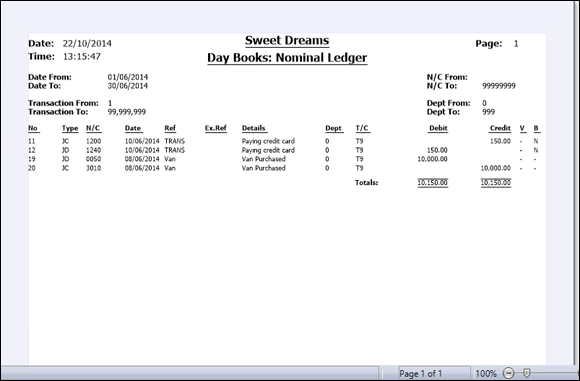

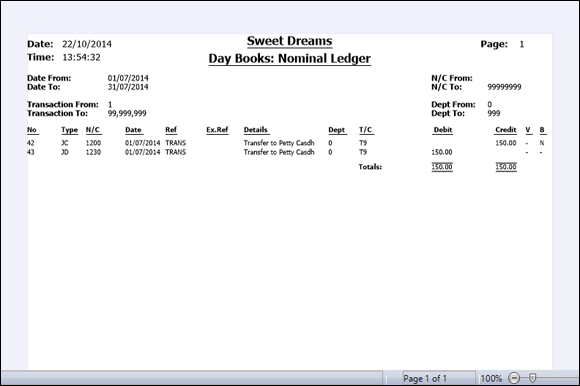

Many transactions don’t impact the Sales Ledger or the Purchase Ledger, but they still have to be accounted for. The Nominal Ledger, as stated before, is the master ledger and is a place where all transactions can be found.

Figure 4-4 shows an example of a Nominal Ledger Daybook from Sage. You can see two separate transactions noted here, each with a debit entry and a credit entry.

Figure 4-4: Showing the Nominal Daybook report for Sweet Dreams

Neither of these transactions has impacted the Purchase Ledger or the Sales Ledger, which is why they show up here.

The first two lines show a transfer between two different bank accounts. Basically, a payment has been made from account 1200, which happens to be the Current account, and the payment has been made to 1240, which is a Credit Card account.

The second two entries show a journal that was carried out by Kate, the bookkeeper for Sweet Dreams. They show a van, which was purchased for the business using capital introduced by the owner of the company.

Cashbook Transactions

Everyone likes to be paid, and that includes suppliers. You use the Cashbook to post all transactions that relate to payments or receipts to the business.

Sage uses separate daybooks for Customer Receipts and Other Income Received, as well as Supplier Payments and Other Payments Made.

This section shows you copies of all the relevant daybooks and the bookkeeping entries that are associated with each daybook.

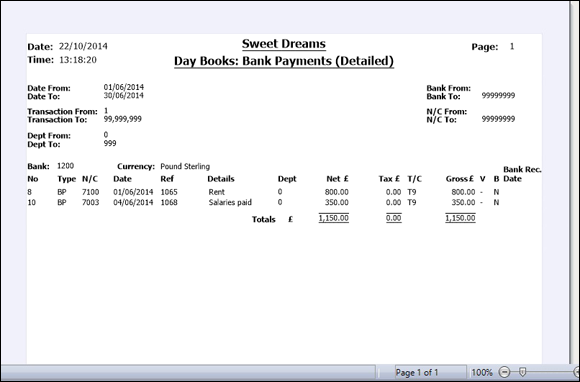

Bank payments

Businesses always make payments to people other than suppliers. For example, they might have salaries, loans, interest and other types of charges to pay. These payments are made from the Bank account or Cashbook, but impact the Nominal Ledger, as part of the double-entry process.

We demonstrate some bank payments that have been made by Sweet Dreams in Figure 4-5. You’ll notice that we’ve printed the Bank Payments Daybook report. If you’d made any payments using cash, you’d also have to print out the Cash Payments Daybook report.

Figure 4-5: Bank Payments Daybook report.

You can see that Sweet Dreams has paid rent and some salaries. These payments have been made from the Bank account. You can see from the report that the Bank account nominal code used is 1200 (which is the default Bank account for Sage). You can also see that the nominal codes used for Rent and Salaries are 7100 and 7003 respectively.

The double-entry bookkeeping that has taken place is as follows:

|

Nominal Code |

Account |

Debit |

Credit |

|

7100 |

Rent |

£800 |

|

|

7003 |

Salaries |

£350 |

|

|

1200 |

Bank |

£1,150 |

This Nominal Ledger summary balances out at £1,150 each for the debits and credits. The Bank account is decreased to show the cash outlay; the Rent and Salaries Expense accounts are increased to show the additional expenses.

Looking at the Bank Payments Daybook, you can also see a reference column. The numbers in the reference column refer to the cheque number used to make that payment. For example, cheque number 1065 was used to pay the rent.

Whether you use a computerised or a manual system, always use references to point towards the original source of the data. In this example, a cheque stub reference has been used.

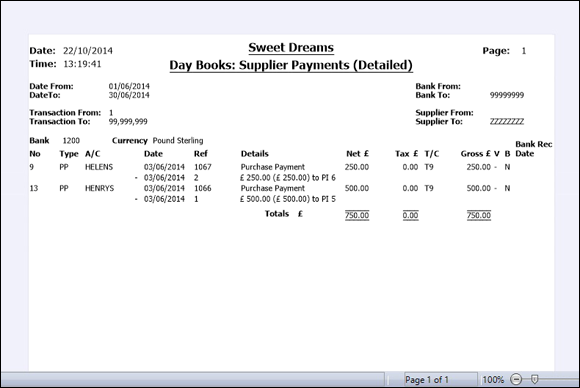

Supplier payments

When businesses pay their suppliers, unless they’ve paid cash immediately, the two accounts that are affected are the Supplier (Creditors) Ledger and the Bank account.

Figure 4-6 shows an example of the Supplier Payments Daybook for Sweet Dreams.

Figure 4-6: Supplier Payment Daybook.

You can see from the daybook report that Sweet Dreams has paid two suppliers in June 2014. It’s paid Helen’s £250 and Henry’s £500. Therefore, Sweet Dreams has taken a total of £750 out of the bank to pay suppliers. The double entry for these two transactions can be summarised as follows:

|

Nominal Code |

Account |

Debit |

Credit |

|

2100 |

Creditors |

£750 |

|

|

1200 |

Bank |

£750 |

You can see that the bank has been credited, because you’re reducing an asset (that is, cash), and the Creditors Account has been debited, because you’re reducing a liability. Think back to your double-entry rules if you’re not sure.

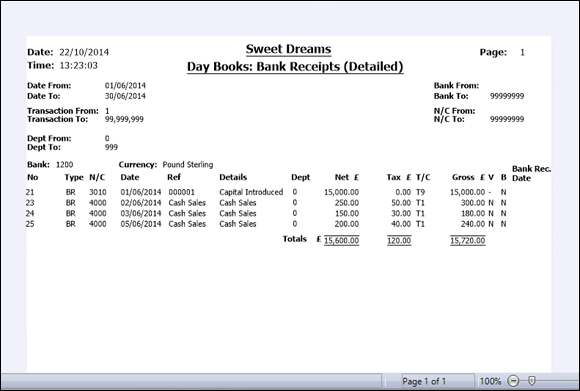

Bank receipts

A business receives money from a variety of sources, not just from its customers. For example, in a new business, the owners of the business may decide to introduce capital into the business to help pay the bills for the first few months until sales pick up. Perhaps they receive start-up grants, or receive interest from savings accounts. Figure 4-7 shows the daybook report for Bank Received for Sweet Dreams.

Figure 4-7: Bank Receipt Daybook Report for Sweet Dreams.

You may have noticed that some cash sales are listed here. This is money taken at the tills and paid directly into the bank account for Sweet Dreams. The owner has also introduced £15,000 of capital.

The transactions that are posted to the Nominal Ledger can be summarised as follows:

|

Nominal Code |

Account |

Debit |

Credit |

|

1200 |

Bank |

£15,720 |

|

|

4000 |

Sales |

£600 |

|

|

3050 |

Capital Introduced |

£15,000 |

|

|

2201 |

VAT |

£120 |

Both sides total £15,720, so the books are in balance.

Once again, you can apply double-entry rules. You debit the bank, because an asset (the bank) is being increased, due to the money being paid in. You credit the Sales account because it’s an Income account, and you also credit the Capital Introduced account, because the amount is a liability for the business. The reason is that the business technically owes the owner this money. You also credit VAT, because VAT is a liability and is money owed to HM Revenue & Customs.

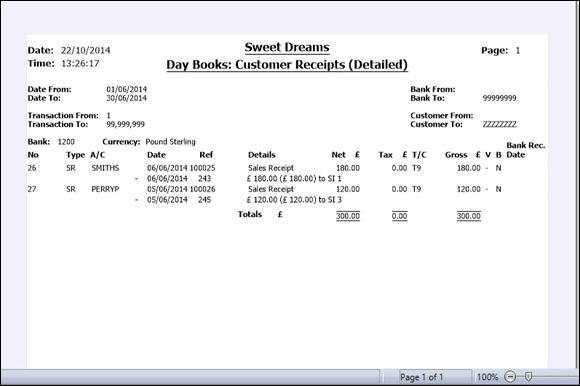

Customer receipts

Obviously, you hope to be paid quite often! If you’re doing a good job as a bookkeeper, you know how much money is owed to the business at any one time. You also know who’s behind with their payments. We discuss how you can find out who owes you money in Book II, Chapter 2.

Receipts from customers can come in several formats. They’re cash received, cheques received or a BACs payment received directly into your bank account. Either way, the money has to be accounted for.

Figure 4-8 shows an example of a Customer Receipts Daybook for Sweet Dreams.

Figure 4-8: Customer Receipts Daybook for Sweet Dreams.

You can see that Sweet Dreams has a couple of cheques received from customers. S. Smith paid £180 and has the reference 100025 against the sales receipt. This refers to the paying-in slip number used when paying the cheque into the bank. This is especially useful when you come to reconcile your bank account later in the accounting process. Underneath, the reference 243 is the invoice number that’s being paid.

You can also see that P. Perry sent a cheque for £120. The paying-in slip reference was 100026 and the invoice being paid was 245.

This transaction can be summarised as follows:

|

Nominal Code |

Account |

Debit |

Credit |

|

1200 |

Bank account |

£300 |

|

|

1100 |

Debtors Ledger |

£300 |

Following your double-entry rules, you can see that the Bank account has been debited, because you’re increasing an asset, namely the Bank account balance. The Debtors Ledger has been credited, because you’re also reducing an asset, namely Debtors. The books still balance, because an equal and opposite entry has been made in the accounts.

Introducing Control Accounts

So far we’ve discussed how you enter transactions into your bookkeeping system, and we’ve demonstrated the double-entry bookkeeping associated with each of the transactions.

At the end of the month, check that the Sales Ledger, the Purchase Ledger and the Nominal Ledger are in agreement. The easiest way to do this check is to perform Control account reconciliations.

‘What on earth are these?’ we hear you say!

Well, don’t panic, they’re quite straightforward, particularly in a computerised accounting system, where the double entry is all done for you!

In performing a Control account reconciliation, all you’re doing is checking that the Nominal Ledger agrees with both the Debtors (Customers) and Creditors (Suppliers) Ledgers.

Debtors Control account

This account totals all the Sales Invoices, Sales Credit Notes and Customer receipts for the month and is held in the Nominal Ledger.

The Debtors Control account shows you how much is owing to your business by your customers. It can be reconciled against the Aged Debtors report for the same period to ensure accuracy of your information. This would be known as a Debtors Control account reconciliation.

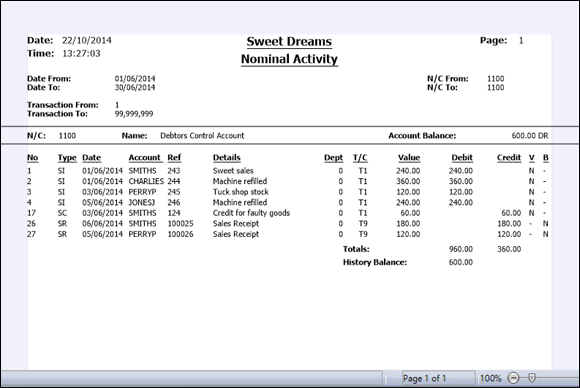

Figure 4-9 shows you an example of Sweet Dreams Debtors Control account for the month of June 2014.

Figure 4-9: Debtors Control account for Sweet Dreams.

You can access the account via the Nominal Ledger and print off a nominal activity report for the month of June. See Figure 4-9.

You can see that the account balance is £600 - this sum is the total amount owed by debtors at 30 June 2014. The Debtors Control account details all the transactions that have taken place in the month of June. You can see that Kate, the Sweet Dreams bookkeeper, has raised sales invoices, created a credit note and recorded a couple of receipts from Smiths for £180, and Perry for £120.

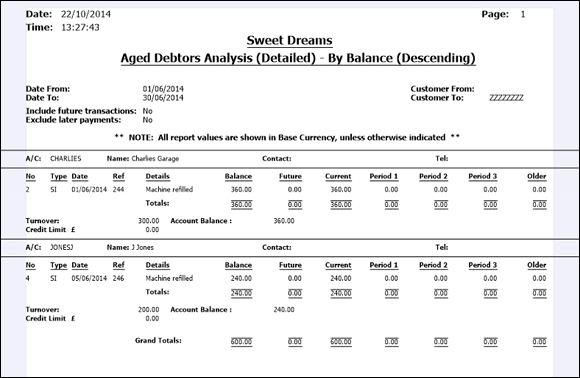

If you want to verify the amount in the Sales Ledger, you can run an Aged Debtor report that shows all outstanding invoices for the month. We’ve run the report for Sweet Dreams for June 2014 (the same period as the nominal activity report shown in Figure 4-9).

Figure 4-10: An Aged Debtor report for Sweet Dreams for June 2014.

Here, you can see that the total amount outstanding at 30 June 2014 was £600, as agreed with the Debtors Control account balance of the same period.

This proves that the Nominal Ledger and the Sales Ledger are in agreement. This is an important reconciliation you need to do at the end of each month, and should always form part of your bookkeeping routine.

Creditors Control account

Similarly, the Creditors Control account shows you how much you owe your suppliers. This can be reconciled against the Aged Creditors report, to verify the accuracy of your information.

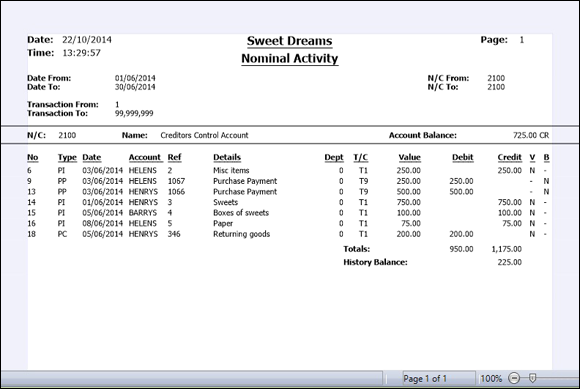

Figure 4-11 shows an example of Sweet Dreams’s Creditors Control account for the month of June 2014. You can see that the balance is £725, made up of a number of purchase invoices, a credit note and a couple of payments.

Figure 4-11: Creditors Control account for Sweet Dreams for June 2014.

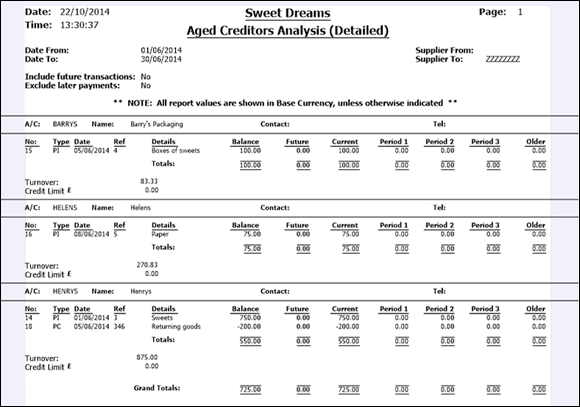

You can check that the information contained in the Nominal Ledger (Creditors Control account) is accurate by running an Aged Creditors report from the Creditors Ledger.

See Figure 4-12 for an example of an Aged Creditors report for Sweet Dreams for the month of June 2014.

Figure 4-12: Aged Creditor Report for Sweet Dreams for June 2014.

You can see that the balance on the Aged Creditors report is also £725, so the two reports reconcile.

In performing both of the preceding reconciliations, you’re checking that the Nominal Ledger agrees with both the Debtors (customers) and Creditors (suppliers) Ledgers.

Understanding How the Ledgers Impact the Accounts

The three accounts - Cash, Trade Debtors and Trade Creditors - are part of the Balance Sheet, which we explain fully in Book IV, Chapter 2. Asset accounts on the Balance Sheet usually carry debit balances because they reflect assets (in this case, cash) that the business owns. Cash and Trade Debtors are Asset accounts. Liability and Capital accounts usually carry credit balances because Liability accounts show claims made by creditors (in other words, money the business owes to financial institutions, suppliers or others), and Capital accounts show claims made by owners (in other words, how much money the owners have put into the business). Trade Creditors is a Liability account.

Here’s how these accounts impact the balance of the business:

|

Assets |

= |

Liabilities |

+ |

Capital |

|

Cash |

Trade Creditors |

|||

|

Trade Debtors |

(Usually credit balance) |

|||

|

(Usually debit balance) |

Here’s how these accounts affect the balances of the business.

The Sales account (see Figure 4-13) isn’t a Balance Sheet account. Instead, the Sales account is used to develop the Profit and Loss statement, which shows whether or not a business made a profit in the period being examined. A profit means that you earned more through sales than you paid out in costs or expenses. Expense and cost accounts usually carry a debit balance.

Figure 4-13: The Sales account for Sweet Dreams as shown in the Nominal Ledger.

(For the low-down on Profit and Loss statements, see Book IV, Chapter 1.) Credits and debits are pretty straightforward in the Sales account: credits increase the account and debits decrease it. Fortunately, the Sales account usually carries a credit balance, which means that the business has income.

The Profit and Loss statement’s bottom line figure shows whether or not the business made a profit. When the business makes a profit, the Sales account credits exceed Expense and Cost account debits. The profit is in the form of a credit, which gets added to the Capital account called Retained Earnings, which tracks how much of your business’s profits are reinvested to grow the business. When the business loses money and the bottom line of the Profit and Loss statement shows that costs and expenses exceeded sales, the number is a debit. That debit is subtracted from the balance in Retained Earnings, to show the reduction to profits reinvested in the business.

When your business earns a profit at the end of the accounting period, the Retained Earnings account increases thanks to a credit from the Sales account. When you lose money, your Retained Earnings account decreases.

Because the Retained Earnings account is a Capital account and Capital accounts usually carry credit balances, Retained Earnings usually carries a credit balance as well.

Adjusting for Nominal Ledger Errors

Your entries in the Nominal Ledger aren’t cast in stone. If necessary, you can always change or correct an entry with an adjusting entry. Four of the most common reasons for Nominal Ledger adjustments are

· Depreciation: A business shows the ageing of its assets through depreciation. Each year, you write off a portion of the original cost of an asset as an expense, and you note that change as an adjusting entry.

· Prepaid expenses: You allocate expenses that are paid up front, such as a year’s worth of insurance, by the month using an adjusting entry. You usually make this type of adjusting entry as part of the closing process at the end of an accounting period. We show you how to develop entries related to prepaid expenses in Book III, Chapter 3.

· Adding an account: You can add accounts by way of adjusting entries at any time during the year. If you’re creating the new account to track transactions separately that at one time appeared in another account, you must move all transactions already in the books to the new account. You do this transfer with an adjusting entry to reflect the change.

· Deleting an account: Only delete an account at the end of an accounting period.

We talk more about adjusting entries and how you can use them in Book III, Chapter 3.

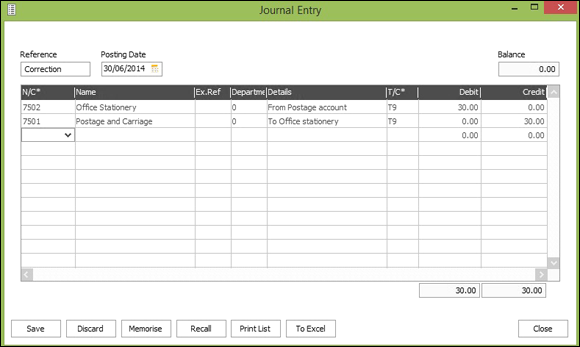

Sometimes, you may simply make a mistake and need to journal a balance from one account to another. For example, you may have coded paper that you bought into the postage account in error. In order to correct this mistake, you need to carry out the following correction:

|

Debit |

Credit |

|

|

Office Stationery |

£30 |

|

|

Postage |

£30 |

To correct the postage account

The double entry has now corrected both accounts, but you need to have knowledge of the bookkeeping rules set out in Book I, Chapter 2 to feel confident to be able to carry out this nominal adjustment. In Sage 50, you would use a nominal journal to complete this transaction, as shown in Figure 4-14.

Figure 4-14: Showing a correcting journal entry.

Have a Go

Grab a piece of paper and have a go at practising how to create your own entries and how to post them to the Nominal Ledger.

1. In which ledger would you record the purchase of new furniture for a business on credit?

2. In which ledger would you record the payment of invoices with cash?

3. In which ledger would you record the sale of goods to a customer on credit?

4. Using the information in Figure 4-15, how would you develop an entry for the Nominal Ledger to record transactions from the Sales Ledger for the month of July?

5. Using the information from Figure 4-16, how would you develop an entry for the Nominal Ledger to record purchase invoices posted for the month of July? Assume that the invoices aren’t going to be paid straight away.

6. On 1 July, Kate the bookkeeper transfers £150 from the business Current Bank account to the Petty Cash account. Can you confirm the double entry that takes place in the accounts system? Which accounts are debited and which are credited and why?

7. Kate writes some cheques out as follows:

|

Chq No. |

Details |

Amount |

|

1069 |

Rent |

£800 |

|

1070 |

Salaries |

£500 |

8. Can you confirm the double entry that takes place for these two transactions?

9. On 31 July, Kate decided to pay the following suppliers:

|

Supplier |

Chq No. |

Amount |

|

Barry’s Packaging |

1071 |

£100 |

|

Helen’s |

1072 |

£75 |

|

Henry’s |

1073 |

£550 |

10. Can you confirm the double entry that takes place in the accounting system?

11. Kate receives a grant on 1 July for £200. She pays this grant into the business current account. Can you confirm the double entry that takes place and say why?

12. On 15 July, Kate receives a cheque from her customer J. Jones for £140. Can you confirm the double entry that takes place in the accounts system and explain why?

13. At the end of the month, Kate runs a copy of her Trial Balance and sees that a large balance has been coded to Materials Purchased. Using her Sage reports, she can see a couple of items that have been coded to Materials Purchased incorrectly.

The following two items, need to be taken out of materials purchased and coded to the following accounts:

|

Office Stationery |

£62.50 |

|

Distribution Costs |

£1,500 |

Can you confirm the double entry that needs to take place to correct the accounts?

Figure 4-15: Customer Invoice Daybook for Sweet Dreams for July 2014.

Figure 4-16: The Supplier Invoices Day Book for Sweet Dreams for July 2014.

Answering the Have a Go Questions

1. The purchase of new furniture for the business would actually be an asset and not a cost, for the purpose of purchasing or manufacturing items for sale.

Therefore, the following double entry would take place:

|

Account |

Debit |

Credit |

|

Office Furniture |

£xx |

|

|

Creditors Ledger |

£xx |

The rules of double entry applied are

To increase an asset (Office Furniture), you debit the Asset account.

To increase a liability (Creditors Ledger), you credit the Liability account.

2. Cashbook.

All cash payments are entered into the Cashbook as a cash payment.

3. Sales Ledger: all sales are tracked in the Sales Ledger.

4. The double entry would be as follows:

|

Account |

Debit |

Credit |

|

Trade Debtors |

£4,050 |

|

|

Sales |

£3,375 |

|

|

VAT |

£675 |

5. The double entry would be as follows:

|

Account |

Debit |

Credit |

|

Materials Purchased |

£4,250 |

|

|

VAT |

£850 |

|

|

Trade Creditors |

£5,100 |

6. The double entry that takes place is as follows:

|

Account |

Debit |

Credit |

|

Petty Cash account |

£150 |

|

|

Bank Current account |

£150 |

7. The double entry rules that have been applied are

8. If you want to increase an Asset account (for example, Petty Cash), you debit that account.

9. To decrease an Asset account (for example, Bank Current account) you credit that account.

10. See Figure 4-17 for the Nominal Daybook report to see confirmation of the double entry that has taken place.

11. You can see that Sage 50 has debited nominal code 1230 (Petty Cash) and credited nominal code 1200 (Bank Current Account).

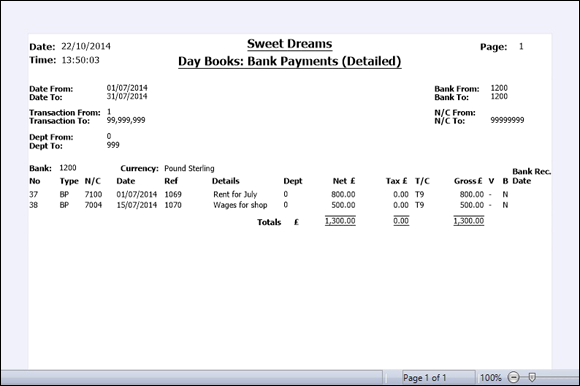

12. The double entry that should take place when the bank payments are shown below. You can also see the entries shown in Figure 4-18.

|

Account |

Debit |

Credit |

|

Rent |

£800 |

|

|

Wages |

£500 |

|

|

Bank |

£1,300 |

13. The double entry rules that have been adhered to are as follows:

14. To record an expense (such as Rent or Wages), you debit the Expense account.

15. To decrease an asset (in this case the Bank account), you credit the Asset account.

16. Notice that the cheque numbers have been used in the reference field, thus allowing the transaction to be traced back to the original source document.

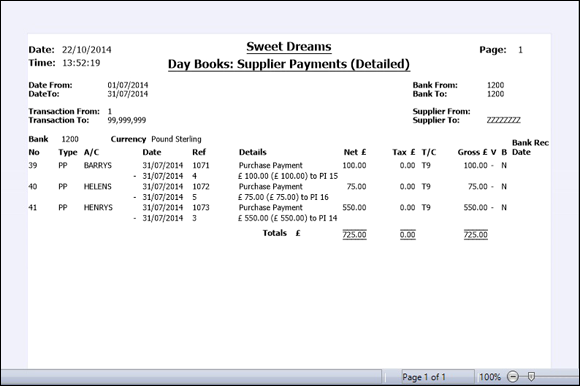

17. The double entry that takes place is as follows:

|

Account |

Debit |

Credit |

|

Creditors Ledger |

£725 |

|

|

Bank |

£725 |

18. The double entry rules used are as follows:

19. To decrease a liability (Trade Creditors), you must debit the account.

20. To decrease an asset (Bank Current account), you must credit the account.

21. You can see these transactions demonstrated in the Supplier Payments Daybook shown in Figure 4-19 .

22. The double entry should be as follows:

|

Account |

Debit |

Credit |

|

Bank |

£200 |

|

|

Other Income |

£200 |

23. The double entry rules are as follows:

24. To increase an asset (Bank Current account), you debit the Asset account.

25. To record income, you credit the Income account.

26. The double entry that takes place is as follows:

|

Account |

Debit |

Credit |

|

Bank |

£140 |

|

|

Debtors Ledger |

£140 |

27. The double entry rules that are applied are as follows:

28. To increase an asset (such as Bank), the account is debited.

29. To decrease an asset (such as Debtors), the account is credited.

30. The double entry that needs to take place to correct the materials purchased code is as follows:

|

Account |

Debit |

Credit |

|

Office Stationery |

£62.50 |

|

|

Distribution Costs |

£1,500 |

|

|

Materials Purchased |

£1,562.50 |

31. This now corrects the appropriate codes.

Figure 4-17: The Nominal Daybook for Sweet Dreams for July 2014.

Figure 4-18: The Bank Payment Day Book for Sweet Dreams for July 2014.

Figure 4-19: Supplier Payments Day Book for Sweet Dreams for July 2014.