Bookkeeping & Accounting All-in-One For Dummies (2015)

Book I

Basic Bookkeeping

Chapter 3

Outlining Your Financial Roadmap with a Chart of Accounts

In This Chapter

![]() Introducing the Chart of Accounts

Introducing the Chart of Accounts

![]() Looking at Balance Sheet accounts

Looking at Balance Sheet accounts

![]() Going over the Profit and Loss

Going over the Profit and Loss

![]() Creating your own Chart of Accounts

Creating your own Chart of Accounts

Can you imagine what a mess your cheque book would be if you didn’t record each cheque you write? Like us, you’ve probably forgotten to record a cheque or two on occasion, but you certainly found out quickly enough when an important payment bounced as a result. Yikes!

Keeping the books of a business can be a lot more difficult than maintaining a personal cheque book. Each business transaction must be carefully recorded to make sure that it goes into the right account. This careful bookkeeping gives you an effective tool for working out how well the business is doing financially.

As a bookkeeper, you need a roadmap to help you determine where to record all those transactions. This roadmap is called the Chart of Accounts. In this chapter, we tell you how to set up the Chart of Accounts, which includes many different accounts. We also review the types of transactions you enter into each type of account in order to track the key parts of any business - assets, liabilities, capital, income and expenses.

Getting to Know the Chart of Accounts

The Chart of Accounts is the roadmap that a business creates to organise its financial transactions. After all, you can’t record a transaction until you know where to put it! Essentially, this chart is a list of all the accounts a business has, organised in a specific order; each account has a description that includes the type of account and the types of transactions to be entered into that account. Every business creates its own Chart of Accounts based on how the business is operated, so you’re unlikely to find two businesses with the exact same Charts of Accounts.

The Chart of Accounts is the roadmap that a business creates to organise its financial transactions. After all, you can’t record a transaction until you know where to put it! Essentially, this chart is a list of all the accounts a business has, organised in a specific order; each account has a description that includes the type of account and the types of transactions to be entered into that account. Every business creates its own Chart of Accounts based on how the business is operated, so you’re unlikely to find two businesses with the exact same Charts of Accounts.

However, you find some basic organisational and structural characteristics in all Charts of Accounts. The organisation and structure are designed around two key financial reports: the Balance Sheet, which shows what your business owns and what it owes, and the Profit and Loss statement, which shows how much money your business took in from sales and how much money it spent to generate those sales. (You can find out more about Profit and Loss statements in Book IV, Chapter 1 and Balance Sheets in Book IV, Chapter 2.)

The Chart of Accounts starts with the balance sheet accounts, which include the following:

· Fixed assets: Includes all accounts that show things the business owns that have a lifespan of more than 12 months, such as buildings, furniture, plant and equipment, motor vehicles and office equipment.

· Current assets: Includes all accounts that show things the business owns and expects to use in the next 12 months, such as cash, Trade Debtors (also known as Accounts Receivable, which is money due from customers), prepayments and stock.

· Current liabilities: Includes all accounts that show debts that the business must repay over the next 12 months, such as Trade Creditors (also known as Accounts Payable, which is bills from suppliers, contractors and consultants), hire purchase and other loans, value-added tax (VAT) and income/corporation tax, accruals and credit cards payable.

· Long-term liabilities: Includes all accounts that show debts that the business must pay over a period of time longer than the next 12 months, such as mortgages repayable and longer-term loans that are repayable.

· Capital: Includes all accounts that show the owners of the business and their claims against the business’s assets, including any money invested in the business, any money taken out of the business and any earnings that have been reinvested in the business.

The rest of the chart is filled with Profit and Loss statement accounts, which include the following:

· Income: Includes all accounts that track sales of goods and services as well as revenue generated for the business by other means.

· Cost of Goods Sold: Includes all accounts that track the direct costs involved in selling the business’s goods or services.

· Expenses: Includes all accounts that track expenses related to running the businesses that aren’t directly tied to the sale of individual products or services.

When developing the Chart of Accounts, start by listing all the Asset accounts, the Liability accounts, the Capital accounts, the Revenue accounts and, finally, the Expense accounts. All these accounts feed into two statements: the Balance Sheet and the Profit and Loss statement.

In this chapter, we review the key account types found in most businesses, but this list isn’t cast in stone. You need to develop an account list that makes the most sense for how you’re operating your business and the financial information you want to track. As we explore the various accounts that make up the Chart of Accounts, we point out how the structure may differ for different types of businesses.

In this chapter, we review the key account types found in most businesses, but this list isn’t cast in stone. You need to develop an account list that makes the most sense for how you’re operating your business and the financial information you want to track. As we explore the various accounts that make up the Chart of Accounts, we point out how the structure may differ for different types of businesses.

The Chart of Accounts is a money-management tool that helps you follow your business transactions, so set it up in a way that provides you with the financial information you need to make smart business decisions. You’re probably going to tweak the accounts in your chart annually and, if necessary, you may add accounts during the year if you find something for which you want more detailed tracking. You can add accounts during the year, but don’t delete accounts until the end of a 12-month reporting period. We discuss adding and deleting accounts from your books in Book III, Chapter 3.

The Chart of Accounts is a money-management tool that helps you follow your business transactions, so set it up in a way that provides you with the financial information you need to make smart business decisions. You’re probably going to tweak the accounts in your chart annually and, if necessary, you may add accounts during the year if you find something for which you want more detailed tracking. You can add accounts during the year, but don’t delete accounts until the end of a 12-month reporting period. We discuss adding and deleting accounts from your books in Book III, Chapter 3.

Starting with the Balance Sheet Accounts

The first part of the Chart of Accounts is made up of Balance Sheet accounts, which break down into the following three categories:

· Assets: These accounts show what the business owns. Assets include cash on hand, furniture, buildings and vehicles.

· Liabilities: These accounts show what the business owes or, more specifically, claims that lenders have against the business’s assets. For example, mortgages on buildings and long-term loans are two common types of liabilities. Also, a mortgage (a legal charge) is a good example of a claim that the lender (bank or building society) has over a business asset (in this case, the premises being bought through the mortgage).

· Capital: These accounts show what the owners put into the business and the claims the owners have against the business’s assets. For example, shareholders are business owners that have claims against the business’s assets.

The Balance Sheet accounts, and the financial report they make up, are so-called because they have to balance out. The value of the assets must be equal to the claims made against those assets. (Remember, these claims are liabilities made by lenders and capital made by owners.)

The Balance Sheet accounts, and the financial report they make up, are so-called because they have to balance out. The value of the assets must be equal to the claims made against those assets. (Remember, these claims are liabilities made by lenders and capital made by owners.)

We discuss the Balance Sheet in greater detail in Book IV, Chapter 2, including how to prepare and use it. This section, however, examines the basic components of the Balance Sheet, as reflected in the Chart of Accounts.

Tackling assets

The accounts that track what the business owns - its assets - are always the first category on the chart. The two types of asset accounts are fixed assets and current assets.

Fixed assets

Fixed assets are assets that you anticipate your business is going to use for more than 12 months. This section lists some of the most common fixed assets, starting with the key accounts related to buildings and business premises that the business owns:

· Land and Buildings: This account shows the value of the land and buildings the business owns. The initial value is based on the cost at the time of purchase, but this asset can be (and often is) revalued as property prices increase over time. Because of the virtually indestructible nature of this asset, it doesn’t depreciate at a fast rate. Depreciation is an accounting method that reduces the value of a fixed asset over time. We discuss depreciation in Book III, Chapter 3, and in Book V, Chapter 2 where we see how the accountant determines what depreciation method to use.

· Accumulated Depreciation - Land and Buildings: This account shows the cumulative amount this asset has depreciated over its useful lifespan.

· Leasehold Improvements: This account shows the value of improvements to buildings or other facilities that a business leases rather than purchases. Frequently, when a business leases a property, it must pay for any improvements necessary in order to use that property as the business requires. For example, when a business leases a shop, the space leased is likely to be an empty shell or filled with shelving and other items that don’t match the particular needs of the business. As with land and buildings, leasehold improvements depreciate as the value of the asset ages - usually over the remaining life of the lease.

· Accumulated Depreciation - Leasehold Improvements: This account tracks the cumulative amount depreciated for leasehold improvements.

The following are the types of accounts for smaller long-term assets, such as vehicles and furniture:

· Vehicles: This account shows any cars, lorries or other vehicles owned by the business. The initial value of any vehicle is listed in this account based on the total cost paid to put the vehicle into service. Sometimes this value is more than the purchase price if additions were needed to make the vehicle usable for the particular type of business. For example, when a business provides transportation for the handicapped and must add additional equipment to a vehicle in order to serve the needs of its customers, that additional equipment is added to the value of the vehicle. Vehicles also depreciate through their useful lifespan.

· Accumulated Depreciation - Vehicles: This account shows the depreciation of all vehicles owned by the business.

· Furniture and Fixtures: This account shows any furniture or fixtures purchased for use in the business. The account includes the value of all chairs, desks, store fixtures and shelving needed to operate the business. The value of the furniture and fixtures in this account is based on the cost of purchasing these items. Businesses depreciate these items during their useful lifespan.

· Accumulated Depreciation - Furniture and Fixtures: This account shows the accumulated depreciation of all furniture and fixtures.

· Plant and Equipment: This account shows equipment that was purchased for use for more than 12 months, such as process-related machinery, computers, copiers, tools and cash registers. The value of the equipment is based on the cost to purchase these items. Equipment is also depreciated to show that over time it gets used up and must be replaced.

· Accumulated Depreciation - Plant and Equipment: This account tracks the accumulated depreciation of all the equipment.

The following accounts show the fixed assets that you can’t touch (accountants refer to these assets as intangible assets), but that still represent things of value owned by the business, such as start-up costs, patents and copyrights. The accounts that track them include:

· Start-up Costs: This account shows the initial start-up expenses to get the business off the ground. Many such expenses can’t be set off against business profits in the first year. For example, special licences and legal fees must be written off over a number of years using a method similar to depreciation, called amortisation, which is also tracked.

· Amortisation - Start-up Costs: This account shows the accumulated amortisation of these costs during the period in which they’re being written-off.

· Patents: This account shows the costs associated with patents, which are grants made by governments that guarantee to the inventor of a product or service the exclusive right to make, use and sell that product or service over a set period of time. Like start-up costs, patent costs are amortised. The value of this asset is based on the expenses the business incurs to get the right to patent its product.

· Amortisation - Patents: This account shows the accumulated amortisation of a business’s patents.

· Copyrights: This account shows the costs incurred to establish copyrights, the legal rights given to an author, playwright, publisher or any other distributor of a publication or production for a unique work of literature, music, drama or art.

· Goodwill: This account is needed only if a business buys another business for more than the actual value of its tangible assets. Goodwill reflects the intangible value of this purchase for things like business reputation, store locations, customer base and other items that increase the value of the business bought. The value of goodwill isn’t everlasting and so, like other intangible assets, must be amortised.

· Research and Development: This account shows the investment the business has made in future products and services, which may not see the light of day for several years. These costs are written off (amortised) over the life of the products and services as and when they reach the marketplace.

If you hold a lot of assets that aren’t of great value, you can also set up an Other Assets account to show those assets that don’t have significant business value. Any asset you show in the Other Assets account that you later want to show individually can be shifted to its own account. We discuss adjusting the Chart of Accounts in Book III, Chapter 3.

Current assets

Current assets are the key assets that your business uses up within a 12-month period and are likely not to be there the next year. The accounts that reflect current assets on the Chart of Accounts are

· Current account: This account is the business’s primary bank account for operating activities, such as depositing receipts and paying expenses. Some businesses have more than one account in this category; for example, a business with many divisions may have an account for each division.

· Deposit account: This account is used for surplus cash. Any cash not earmarked for an immediate plan is deposited in an interest-earning savings account. In this way, the cash earns interest while the business decides what to do with it.

· Cash on Hand: This account is used to record any cash kept at retail stores or in the office. In retail stores, cash must be kept in registers in order to provide change to customers. In the office, petty cash is often kept for immediate cash needs that pop up from time to time. This account helps you keep track of the cash held outside the various bank and deposit accounts.

· Trade Debtors: This account shows the customers who still owe you money if you offer your products or services to customers on credit (by which we mean your own credit system).

Trade Debtors isn’t used to show purchases made on other types of credit cards, because your business gets paid directly by banks, not customers, when customers use credit cards. Check out Book II, Chapter 2 to read more about this scenario and the corresponding type of account.

· Stock: This account shows the value of the products you have on hand to sell to your customers. The value of the assets in this account varies depending upon the way you decide to track the flow of stock into and out of the business. We discuss stock valuation and recording in greater detail in Book II, Chapter 3.

· Prepayments: This account shows goods or services you pay for in advance: the payment is credited as it gets used up each month. For example, say that you prepay your property insurance on a building that you own one year in advance. Each month you reduce the amount that you prepaid by one-twelfth as the prepayment is used up. We discuss prepayments in Book III, Chapter 3.

Depending upon the type of business you’re setting up, you may have other current Asset accounts to set up. For example, say that you’re starting a service business in consulting. You’re likely to have an account called Consulting Fees for tracking cash collected for those services.

Laying out your liabilities

After you deal with assets, the next stop on the bookkeeping journey is the accounts that show what your business owes to others. These others can include suppliers from whom you buy products or supplies, financial institutions from which you borrow money and anyone else who lends money to your business. Like assets, you lump liabilities into current liabilities and long-term liabilities.

Current liabilities

Current liabilities are debts due in the next 12 months. Some of the most common types of current liabilities accounts that appear on the Chart of Accounts are as follows:

· Trade Creditors: This account shows money that the business owes to suppliers, contractors and consultants that must be paid in less than 12 months. Most of these liabilities must be paid in 30 to 90 days from initial invoicing.

· Value-Added Tax (VAT): This account shows your VAT liability. You may not think of VAT as a liability, but because the business collects the tax from the customer and doesn’t pay it immediately to HM Customs & Revenue, the taxes collected become a liability. Of course you’re entitled to offset the VAT that the business has been charged on its purchases before making a net payment. A business usually collects VAT throughout the month and then pays the net amount due on a quarterly basis. We discuss paying VAT in greater detail in Book III, Chapter 1.

· Accrued Payroll Taxes: This account shows payroll taxes, such as Pay As You Earn (PAYE) and National Insurance, collected from employees and the business itself, which have to be paid over to HM Revenue & Customs. Businesses don’t have to pay these taxes over immediately and may pay payroll taxes on a monthly basis. We discuss how to handle payroll taxes in Book III, Chapter 2.

· Credit Cards Payable: This account shows all credit card accounts for which the business is liable. Most businesses use credit cards as short-term debt and pay them off completely at the end of each month, but some smaller businesses carry credit card balances over a longer period of time. In Chart of Accounts, you can set up one Credit Card Payable account, but you may want to set up a separate account for each card your business holds to improve your ability to track credit card usage.

The way you set up your current liabilities - and how many individual accounts you establish - depends upon the level of detail that you want to use to track each type of liability.

Long-term liabilities

Long-term liabilities are debts due in more than 12 months. The number of long-term liability accounts you maintain on your Chart of Accounts depends on your debt structure. For example, if you’ve several different loans, then set up an account for each one. The most common type of long-term liability accounts is Loans Payable. This account tracks any long-term loans, such as a mortgage on your business building. Most businesses have separate Loans Payable accounts for each of their long-term loans. For example, you can have Loans Payable - Mortgage Bank for your building and Loans Payable - Vehicles for your vehicle loan.

In addition to any separate long-term debt that you may want to track in its own account, you may also want to set up an account called Other Liabilities. You can use this account to track types of debt that are so insignificant to the business that you don’t think they need their own accounts.

Controlling the capital

Every business is owned by somebody. Capital accounts track owners’ contributions to the business as well as their share of ownership. For a limited company, ownership is tracked by the sale of individual shares because each stockholder owns a portion of the business. In smaller businesses owned by one person or a group of people, capital is tracked using capital and drawing accounts. Here are the basic capital accounts that appear in the Chart of Accounts:

· Ordinary Share Capital: This account reflects the value of outstanding ordinary shares sold to investors. A business calculates this value by multiplying the number of shares issued by the value of each share of stock. Only limited companies need to establish this account.

· Retained Earnings: This account tracks the profits or losses accumulated since a business opened. At the end of each year, the profit or loss calculated on the Profit and Loss statement is used to adjust the value of this account. For example, if a business made a £100,000 profit after tax in the past year, the Retained Earnings account is increased by that amount; if the business lost £100,000, that amount is subtracted from this account. Any dividends paid to shareholders reduce the profit figure transferred to Retained Earnings each year.

· Capital: This account is only necessary for small, unincorporated businesses, such as sole traders or partnerships. The Capital account reflects the amount of initial money the business owner contributed to the business as well as any additional contributions made after initial start-up. The value of this account is based on cash contributions and other assets contributed by the business owner, such as equipment, vehicles or buildings. When a small company has several different partners, each partner gets his own Capital account to track his contributions.

· Drawing: This account is only necessary for businesses that aren’t incorporated. The Drawing account tracks any money that a business owner takes out of the business. If the business has several partners, each partner gets his own Drawing account to track what he takes out of the business.

Keeping an Eye on the Profit and Loss Statement Accounts

The Profit and Loss statement is made up of two types of accounts:

· Expenses: These accounts track all costs that a business incurs in order to keep itself afloat.

· Revenue: These accounts track all income coming into the business, including sales, interest earned on savings and any other methods used to generate income.

The bottom line of the Profit and Loss statement shows whether your business made a profit or a loss for a specified period of time. We discuss how to prepare and use a Profit and Loss statement in greater detail in Book IV, Chapter 1.

This section examines the various accounts that make up the Profit and Loss statement portion of the Chart of Accounts.

Recording the profit you make

Accounts that show revenue coming into the business are first up in the Profit and Loss statement section of the Chart of Accounts. If you choose to offer discounts or accept returns, then that activity also falls within the revenue grouping. The most common income accounts are

· Sales of Goods or Services: This account, which appears at the top of every Profit and Loss statement, shows all the money that the business earns selling its products, services or both.

· Sales Discounts: This account shows any reductions to the full price of merchandise (necessary because most businesses offer discounts to encourage sales).

· Sales Returns: This account shows transactions related to returns, when a customer returns a product.

When you examine a Profit and Loss statement from a business other than the one you own or are working for, you usually see the following accounts summarised as one line item called Revenue or Net Revenue. Because not all income is generated by sales of products or services, other income accounts that may appear on a Chart of Accounts include the following:

· Interest Income: This account shows any income earned by collecting interest on a business’s savings accounts. If the business lends money to employees or to another business and earns interest on that money, that interest is recorded in this account as well.

· Other Income: This account shows income that a business generates from a source other than its primary business activity. For example, a business that encourages recycling and earns income from the items recycled records that income in this account.

Recording the cost of sales

Of course, before you can sell a product, you must spend money to buy or make that product. The type of account used to track the money spent on products that are sold is called a Cost of Goods Sold account. The most common cost of goods sold accounts are

· Purchases: This account shows the purchases of all items you plan to sell.

· Purchase Discount: This account shows the discounts you may receive from suppliers when you pay for your purchase quickly. For example, a business may give you a 2 per cent discount on your purchase when you pay the bill in 10 days rather than wait until the end of the 30-day payment period.

· Purchase Returns: This account shows the value of any returns when you’re unhappy with a product you bought.

· Freight Charges: This account shows any charges related to shipping items that you purchase for later sale. You may or may not want to keep this detail.

· Other Sales Costs: This account is a catch-all account for anything that doesn’t fit into one of the other Cost of Goods Sold accounts.

Acknowledging the other costs

Expense accounts take the cake for the longest list of individual accounts. Anything you spend on the business that can’t be tied directly to the sale of an individual product falls under the Expense account category. For example, advertising a sale isn’t directly tied to the sale of any one product, so the costs associated with advertising fall under the Expense account category.

The Chart of Accounts mirrors your business operations, so you decide how much detail you want to keep in your expense accounts. Most businesses have expenses that are unique to their operations, so your list is likely to be longer than the one we present here. However, you also may find that you don’t need some of these accounts. Small businesses typically have expense headings that mirror those required by HM Revenue & Customs on its self-assessment returns.

On your Chart of Accounts, the Expense accounts don’t have to appear in any specific order, so we list them alphabetically. The most common Expense accounts are

· Advertising: This account shows all expenses involved in promoting a business or its products. Expenditure on newspaper, television, magazine and radio advertising is recorded here, as well as any costs incurred to print flyers and mailings to customers. Also, when a business participates in community events such as cancer walks or craft fairs, associated costs appear in this account.

· Amortisation: This account is similar to the Depreciation account (see later in this list) and shows the ongoing monthly charge for the current financial year for all your intangible assets.

· Bank Service Charges: This account shows any charges made by a bank to service a business’s bank accounts.

· Depreciation: This account shows the ongoing monthly depreciation charge for the current financial year for all your fixed assets - buildings, cars, vans, furniture and so on. Of course, when the individual depreciation values are large for each fixed asset category, you may open up individual depreciation accounts.

· Dues and Subscriptions: This account shows expenses related to business-club membership or subscriptions to magazines for the business.

· Equipment Rental: This account records expenses related to renting equipment for a short-term project; for example, a business that needs to rent a van to pick up new fixtures for its shop records that van rental in this account.

· Insurance: This account shows insurance costs. Many businesses break this account down into several accounts such as Building Insurance, Public Liability Insurance and Car Insurance.

· Legal and Accounting: This account shows the cost of legal or accounting advice.

· Miscellaneous Expenses: This account is a catch-all account for expenses that don’t fit into one of a business’s established accounts. If certain miscellaneous expenses occur frequently, a business may choose to add an account to the Chart of Accounts and move related expenses into that new account by subtracting all related transactions from the Miscellaneous Expenses account and adding them to the new account. With this shuffle, you need to carefully balance out the adjusting transaction to avoid any errors or double counting.

· Office Expenses: This account shows any items purchased in order to run an office. For example, office supplies such as paper and pens or business cards fit in this account. As with miscellaneous expenses, a business may choose to track certain office expense items in its own accounts. For example, when you find that your office is using a lot of copy paper and you want to track that separately, set up a Copy Paper Expense account. Just be sure that you really need the detail because a large number of accounts can get unwieldy and hard to manage.

· Payroll Taxes: This account records any taxes paid related to employee payroll, such as PAYE, Statutory Sick Pay (SSP) and maternity/paternity pay.

· Postage: This account shows any expenditure on stamps, express package shipping and other shipping. If your business does a large amount of shipping through suppliers such as UPS or Federal Express, you may want to track that spending in separate accounts for each supplier. This option is particularly helpful for small businesses that sell over the Internet or through mail-order sales.

· Profit (or Loss) on Disposal of Fixed Assets: This account records any profit when a business sells a fixed asset, such as a car or furniture. Make sure that you only record revenue remaining after subtracting the accumulated depreciation from the original cost of the asset.

· Rent: This account records rental costs for a business’s office or retail space.

· Salaries and Wages: This account shows any money paid to employees as salary or wages.

· Telephone: This account shows all business expenses related to the telephone and telephone calls.

· Travel and Entertainment: This account records any expenditure on travel or entertainment for business purposes. To keep a close watch some businesses separate these expenses into several accounts, such as Travel and Entertainment - Meals; Travel and Entertainment - Travel; and Travel and Entertainment - Entertainment.

· Utilities: This account shows utility costs, such as electricity, gas and water.

· Vehicles: This account shows expenses related to the operation of business vehicles.

Setting Up Your Chart of Accounts

You can use all the lists of accounts provided in this chapter to set up your business’s own Chart of Accounts. No secret method exists for creating your own chart - just make a list of the accounts that apply to your business.

When first setting up your Chart of Accounts, don’t panic if you can’t think of every type of account you may need for your business. You can easily add to the Chart of Accounts at any time. Just add the account to the list and distribute the revised list to any employees who use the Chart of Accounts for recording transactions into the bookkeeping system. (Employees who code invoices or other transactions and indicate the account to which those transactions are to be recorded need a copy of your Chart of Accounts as well, even if they aren’t involved in actual bookkeeping.)

The Chart of Accounts usually includes at least three columns:

· Account: Lists the account names.

· Type: Lists the type of account - Asset, Liability, Capital, Income, Cost of Goods Sold or Expense.

· Description: Contains a description of the type of transaction that is to be recorded in the account.

Many businesses also assign numbers to the accounts, to be used for coding charges. If your company uses a computerised system, the computer automatically assigns the account number. For example, Sage 50 Accounts provides you with a standard Chart of Accounts that you can adapt to suit your business. Sage also allows you to completely customise your Chart of Accounts to codes that suit your business; however, most businesses find that the standard Chart of Accounts is sufficient. A typical numbering system is as follows:

· Asset accounts: 0010 to 1999

· Liability accounts: 2000 to 2999

· Capital accounts: 3000 to 3999

· Sales and Cost of Goods Sold accounts: 4000 to 6999

· Expense accounts: 7000 to 9999

This numbering system matches the one used by some computerised accounting systems, so you can easily make the transition if you decide to automate your books using a computerised accounting system in the future.

One major advantage of a computerised accounting system is the number of different Charts of Accounts that have been developed based on the type of business you plan to run. When you get your computerised system, whichever accounting software you decide to use, you can review the list of chart options included with that software for the type of business you run, delete any accounts you don’t want and add any new accounts that fit your business plan.

If you’re setting up your Chart of Accounts manually, be sure to leave a lot of room between accounts to add new accounts. For example, number your Trade Debtors account 1100 and then start your bank accounts from 1200. If you’ve a number of bank accounts, you can number them 1210, 1220, 1230 and so on. That leaves you plenty of room to add new bank accounts as well as petty cash. The same applies to your revenue accounts: you need to allow plenty of room in your codes for your business to grow. For example, 4000 may be Retail Sales from your shop, but you may start to develop an online presence and need a code to track online sales, perhaps 4050. You can add further codes for foreign online sales as opposed to UK online sales. Don’t be too rigid in your choice of codes - leave as large a gap as possible between codes to give you maximum flexibility.

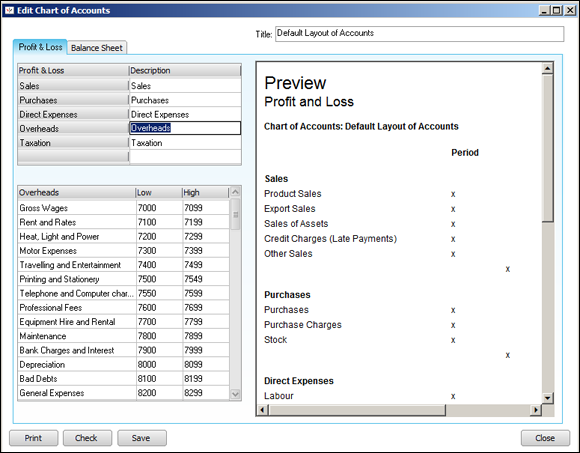

Figure 3-1 is a sample Chart of Accounts developed using Sage 50 Accounts, the accounts package we use throughout this book. This sample chart highlights the standard overhead accounts that Sage has already set up for you.

© 2012 Sage (UK) Limited. All rights reserved.

Figure 3-1: The top portion of a sample Chart of Accounts showing overheads.

Have a Go

1. Describe three types of current assets and state in which financial statement you’d find them.

2. In which financial statement would you expect to see expenses?

List five different types of expenses.

3. In which financial statement would you find current liabilities?

Describe some of the entries you might find there.

4. In which financial statement would you expect to find capital?

As well as capital introduced by the owner, what else would you expect to see there?

5. Think about the current assets you need to track for your business, and write down the accounts in this section.

6. Think about the Fixed Asset accounts you need to track for your business, and write down the accounts for those assets in this section.

7. Think about the Current Liabilities accounts you need to track for your business, and write down the accounts for those liabilities in this section.

8. Think about the Long-term Liabilities accounts you need to track for your business, and write down the accounts for those liabilities in this section.

9. Think about the Capital accounts you need to track for your business, and write down the accounts you need in this section.

10. Think about the Revenue accounts you need to track for your business, and write down those accounts in this section.

11. Think about the Cost of Goods Sold accounts you need to track for your business, and write down those accounts in this section.

12. Think about the Expense accounts you need to track for your business, and write down those accounts in this section.

Answering the Have a Go Questions

1. You can find current assets in the Balance Sheet.

The usual types of current assets are

· Stock

· Debtors

· Cash at bank

· Cash in hand

· Prepayments

See the previous section ‘Current assets’ for descriptions.

2. You can find expenses in the Profit and Loss statement.

Typical expenses can be

· Wages

· Office stationery

· Telephone costs

· Rent and rates

· Heat, light and power

· Fuel expenses

Find more examples in ‘Acknowledging the other costs’.

3. You can find current liabilities in the Balance Sheet.

Typical items include:

· Trade Creditors (suppliers you owe money to)

· Accrued expenses (costs you’ve incurred but you may not have an invoice for)

· HM Revenue & Customs payments due such as PAYE/NI and VAT

· Overdrafts

We go into more detail in the section ‘Laying out your liabilities’.

4. You find capital in the Balance Sheet.

As well as capital introduced, you also find drawings (cash taken out of the business for personal use), dividends and retained profits (profits made from previous periods, but retained in the business). If your business is structured as a company, then you also have ordinary share capital, which reflects each individual’s share of the company.

5-12. The remaining exercises in this chapter don’t have right or wrong answers.

You need to set up your Chart of Accounts with accounts that match how your business operates.