Bookkeeping & Accounting All-in-One For Dummies (2015)

Book VI

Accountants: Working with the Outside World

Chapter 3

Professional Auditors and Advisers

In This Chapter

![]() Cutting the deck for a fair deal: Why audits are needed

Cutting the deck for a fair deal: Why audits are needed

![]() Interpreting the auditor’s report

Interpreting the auditor’s report

![]() Knowing what auditors catch and don’t catch

Knowing what auditors catch and don’t catch

![]() Growing beyond audits: Professional accountancy practices as advisers and consultants

Growing beyond audits: Professional accountancy practices as advisers and consultants

![]() Questioning the independence of auditors

Questioning the independence of auditors

If we’d written this chapter 50 years ago, we’d have talked almost exclusively about the role of the professional chartered or certified accountant as the auditor of the financial statements and footnotes presented in a business’s annual financial report to its owners and lenders. Back then, in the ‘good old days’, audits were a professional accountancy firm’s bread‐and‐butter service - audit fees were a large share of these firms’ annual revenue. Audits were the core function that accountants performed then. In addition to audits, accountants provided accounting and tax advice to their clients, and that was pretty much all they did.

Today, accountants do a lot more than auditing. In fact, the profession has shifted away from the expression auditing in favour of broader terms like assurance and attestation. More importantly, accountants have moved into consulting and advising clients on matters other than accounting and tax. The movement into the consulting business while continuing to do audits - often for the same clients - has caused all sorts of problems, which this chapter looks at after discussing audits by accountants.

Why Audits?

When Jane graduated from university, she went to work for a big national accountancy firm. The transition from textbook accounting theory to real‐world accounting practice came as a shock. Some of her clients dabbled in window dressing (refer to Book VI, Chapter 1), and more than a few used earnings management tactics. It was a bit of a reality check, to say the least! Jane’s experience demonstrates that not everything is pure and straight. Nevertheless, legal and ethical lines of conduct separate what is tolerated and what isn’t. If you cross the lines, you’re subject to legal sanctions and can be held liable to others. For instance, a business can deliberately deceive its investors and lenders with false or misleading numbers in its financial report. Instead of ‘What You See Is What You Get’ in its financial statements, you get a filtered and twisted version of the business’s financial affairs - more of a ‘What I Want You to See Is What You Get’ version. That’s where audits come in.

Audits are the best practical means for keeping fraudulent and misleading financial reporting to a minimum. A business having an independent accounting professional who comes in once a year to check up on its accounting system is like a person getting a physical exam once a year - the audit exam may uncover problems that the business was not aware of, and knowing that the auditors come in once a year to take a close look at things keeps the business on its toes.

Audits are the best practical means for keeping fraudulent and misleading financial reporting to a minimum. A business having an independent accounting professional who comes in once a year to check up on its accounting system is like a person getting a physical exam once a year - the audit exam may uncover problems that the business was not aware of, and knowing that the auditors come in once a year to take a close look at things keeps the business on its toes.

The basic purpose of an annual financial statement audit is to make sure that a business has followed the accounting methods and disclosure requirements required by law - in other words, to make sure that the business has stayed in the ballpark of accounting rules. After completing an audit examination, the accountant prepares a short auditor’s report stating that the business has prepared its financial statements according to the rules - or has not, as the case may be. In this way, audits are an effective means of enforcing accounting standards.

An audit by an independent accountant provides assurance (but not an iron‐clad guarantee) that the business’s financial statements follow accepted accounting methods and provide adequate disclosure. This is the main reason why accountancy firms are paid to do annual audits of financial reports. The auditor must be independent of the business being audited. The auditor can have no financial stake in the business or any other relationship with the client that may compromise his objectivity. However, the independence of auditors has come under scrutiny of late. See the section ‘From Audits to Advising’, later in the chapter.

The core of a business’s financial report is its three primary financial statements - the Profit and Loss statement, the Cash Flow statement and the Balance Sheet - and the necessary footnotes to these statements. A financial report may consist of just these statements and footnotes and nothing more. Usually, however, there’s more - in some cases, a lot more. Book VI, Chapter 1 explains the additional content of financial reports of public business corporations, such as the transmittal letter to the owners from the chief executive of the business, historical summaries, supporting schedules and listings of directors and top‐level managers - items not often included in the financial reports of private businesses.

The auditor’s opinion covers the financial statements and the accompanying footnotes. The auditor, therefore, doesn’t express an opinion on whether the chairman’s letter to the shareholders is a good letter - although if the chairman’s claims contradicted the financial statements, the auditor would comment on the inconsistency. In short, auditors audit the financial statements and their footnotes but don’t ignore the additional information included in annual financial reports.

Although the large majority of audited financial statements are reliable, a few slip through the audit net. Auditor approval isn’t a 100 per cent guarantee that the financial statements contain no erroneous or fraudulent numbers, or that the statements and their footnotes provide all required disclosures, as the all‐too‐frequent Enron‐like events attest.

Who’s Who in the World of Audits

To become a qualified accountant, a person usually has to hold a degree, pass a rigorous national exam, have audit experience and satisfy continuing education requirements. Many accountants operate as sole practitioners, but many form partnerships (also called firms). An accountancy firm has to be large enough to assign enough staff auditors to the client so that all audit work can be completed in a relatively short period - financial reports are generally released about four to six weeks after the close of the fiscal year. Large businesses need large accountancy firms, and very large global business organisations need very large international accountancy firms. The public accounting profession consists of four very large international firms, known as ‘The Big Four’: PricewaterhouseCoopers, Deloitte, KPMG and Ernst & Young. There are also several good‐sized second‐tier national firms, often with international network arrangements, many regional firms, small local firms and sole practitioners.

All businesses whose ownership units (shares) are traded in public markets in the UK, the US and most other countries with major stock markets are required to have annual audits by independent auditors. Every stock you see listed on the LSE (London Stock Exchange), the NYSE (New York Stock Exchange), NASDAQ (National Association of Securities Dealers Automated Quotations) and other stock‐trading markets must be audited by an outside accountancy firm. Accountancy firms are legally organised as limited liability partnerships, so you see LLP after their names. For businesses that are legally required to have audits done, the annual audit is a cost of doing business; it’s the price they pay for going into public markets for their capital and for having their shares traded in a public marketplace - which provides liquidity for their shares.

Banks and other lenders may insist on audited financial statements. We’d say that the amount of a bank loan, generally speaking, has to be more than £5 million or £10 million before a lender will insist that the business pay for the cost of an audit. If outside non‐manager investors - for example, venture capital providers or business angels - have much invested in a business, they almost certainly insist on an annual audit to be carried out by a substantial firm such as those listed earlier.

Instead of an audit, which they couldn’t realistically afford, many smaller businesses have an outside accountant come in regularly to look over their accounting methods and give advice on their financial reporting. Unless an accountant has done an audit, he has to be very careful not to express an opinion on the external financial statements. Without a careful examination of the evidence supporting the account balances, the accountant is in no position to give an opinion on the financial statements prepared from the accounts of the business.

In the grand scheme of things, most audits are a necessary evil that doesn’t uncover anything seriously wrong with a business’s accounting system and the accounting methods it uses to prepare its financial statements. Overall, the financial statements end up looking virtually the same as they’d have looked without an audit. Still, an audit has certain side benefits. In the course of doing an audit, an accountant watches for business practices that could stand some improvement and is alert to potential problems. And fraudsters beware: accountants may face legal action if they fail to report any dodgy dealings they discover.

The auditor usually recommends ways in which the client’s internal controls can be strengthened. For example, an auditor may discover that accounting employees aren’t required to take holidays and let someone else do their jobs while they’re gone. The auditor would recommend that the internal control requiring holidays away from the office be strictly enforced. Book II, Chapter 1 explains that good internal controls are extremely important in an accounting system.

The auditor usually recommends ways in which the client’s internal controls can be strengthened. For example, an auditor may discover that accounting employees aren’t required to take holidays and let someone else do their jobs while they’re gone. The auditor would recommend that the internal control requiring holidays away from the office be strictly enforced. Book II, Chapter 1 explains that good internal controls are extremely important in an accounting system.

What an Auditor Does before Giving an Opinion

An auditor does two basic things: examines evidence and gives an opinion about the financial statements. The lion’s share of audit time is spent on examining evidence supporting the transactions and accounts of the business. A very small part of the total audit time is spent on writing the auditor’s report, in which the auditor expresses an opinion on the financial statements and footnotes.

This list gives you an idea of what the auditor does ‘in the field’ - that is, on the premises of the business being audited:

This list gives you an idea of what the auditor does ‘in the field’ - that is, on the premises of the business being audited:

· Evaluates the design and operating dependability of the business’s accounting system and procedures.

· Evaluates and tests the business’s internal accounting controls that are established to deter and detect errors and fraud.

· Identifies and critically examines the business’s accounting methods - especially whether the methods conform to generally accepted accounting rules, which are the touchstones for all businesses.

· Inspects documentary and physical evidence for the business’s revenues, expenses, assets, liabilities and owners’ equities - for example, the auditor counts products held in stock, observes the condition of those products and confirms bank account balances directly with the banks.

The purpose of all the audit work (examining evidence) is to provide a convincing basis for expressing an opinion on the business’s financial statements, attesting that the company’s financial statements and footnotes (as well as any directly supporting tables and schedules) can be relied upon - or not, in some cases. The auditor puts that opinion in the auditor’s report.

The auditor’s report is the only visible part of the audit process to financial statement readers - the tip of the iceberg. All the readers see is the auditor’s one‐page report (which is based on the evidence examined during the audit process, of course).

What’s in an Auditor’s Report

The audit report, which is included in the financial report near the financial statements, serves two useful purposes:

· It reassures investors and creditors that the financial report can be relied upon or calls attention to any serious departures from established financial reporting standards and principles.

· It prevents (in the large majority of cases, anyway) businesses from issuing sloppy or fraudulent financial reports. Knowing that your report will be subject to an independent audit really keeps you on your toes!

The large majority of audit reports on financial statements give the business a clean bill of health, or a clean opinion. At the other end of the spectrum, the auditor may state that the financial statements are misleading and shouldn’t be relied upon. This negative audit report is called an adverse opinion. That’s the big stick that auditors carry: they have the power to give a company’s financial statements an adverse opinion, and no business wants that. Notice that we say here that the audit firms ‘have the power’ to give an adverse opinion. In fact, the threat of an adverse opinion almost always motivates a business to give way to the auditor and change its accounting or disclosure in order to avoid getting the kiss of death of an adverse opinion. An adverse audit opinion, if it were actually given, states that the financial statements of the business are misleading and, by implication, fraudulent. The London Stock Exchange (LSE) and the US’s Security & Exchange Commission (SEC) don’t tolerate adverse opinions; they’d stop trading in the company’s shares if the company received an adverse opinion from its auditor.

The large majority of audit reports on financial statements give the business a clean bill of health, or a clean opinion. At the other end of the spectrum, the auditor may state that the financial statements are misleading and shouldn’t be relied upon. This negative audit report is called an adverse opinion. That’s the big stick that auditors carry: they have the power to give a company’s financial statements an adverse opinion, and no business wants that. Notice that we say here that the audit firms ‘have the power’ to give an adverse opinion. In fact, the threat of an adverse opinion almost always motivates a business to give way to the auditor and change its accounting or disclosure in order to avoid getting the kiss of death of an adverse opinion. An adverse audit opinion, if it were actually given, states that the financial statements of the business are misleading and, by implication, fraudulent. The London Stock Exchange (LSE) and the US’s Security & Exchange Commission (SEC) don’t tolerate adverse opinions; they’d stop trading in the company’s shares if the company received an adverse opinion from its auditor.

Between the two extremes of a clean opinion and an adverse opinion, an auditor’s report may point out a flaw in the company’s financial statements - but not a fatal flaw that would require an adverse opinion. These are called qualified opinions.

The following sections look at the most common type of audit report: the clean opinion, in which the auditor certifies that the business’s financial statements conform to the rules and are presented fairly, and the other kind of opinion, which is not quite so squeaky clean!

True and fair: A clean opinion

If the auditor finds no serious problems, the audit firm states that the accounts give a true and fair view of the state of affairs of the company. In the US, the auditor gives the financial report an unqualified opinion, which is the correct technical name, but most people call it a clean opinion. This expression has started to make its way in UK accounting parlance as the auditing business becomes more international. The clean‐opinion audit report runs to about 100 words and three paragraphs, with enough defensive legal language to make even a seasoned accountant blush. This is a clean, or unqualified, opinion in the standard three‐paragraph format:

In our opinion:

The financial statements give a true and fair view of the state of affairs of the company and the Group at 22 February 2012 and of the profit and cash flows of the Group for the year then ended;

The financial statements have been properly prepared in accordance with the Companies Act 1985; and

Those parts of the Directors’ remuneration report required by Part 3 of Schedule 7A to the Companies Act 1985 have been properly prepared in accordance with the Companies Act 1985.

|

1st paragraph |

We did the audit, but the financial statements are the responsibility of management; we just express an opinion on them. |

|

2nd paragraph |

We carried out audit procedures that provide us a reasonable basis for expressing our opinion, but we didn’t necessarily catch everything. |

|

3rd paragraph |

The company’s financial statements conform to generally accepted accounting principles and aren’t misleading. |

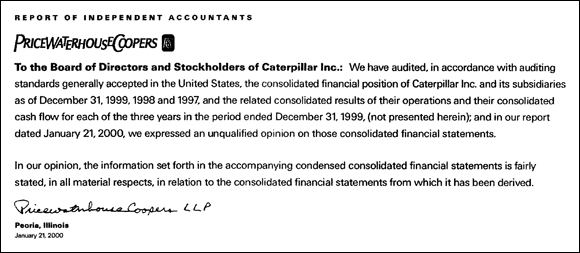

Figure 3‐1 presents a clean opinion but in a one‐paragraph format - given by PricewaterhouseCoopers on one of Caterpillar’s financial statements. For many years, Price Waterhouse (as it was known before its merger with Coopers) was well known for its maverick one‐paragraph audit report.

Figure 3‐1: A one‐paragraph audit report.

Other kinds of audit opinions

An audit report that does not give a clean opinion may look very similar to a clean‐opinion audit report to the untrained eye. Some investors see the name of an audit firm next to the financial statements and assume that everything is okay - after all, if the auditor had seen a problem, the cops would have pounced on the business and put everyone in jail, right? Well, not exactly.

How do you know when an auditor’s report may be something other than a straightforward, no‐reservations clean opinion? Look for a fourth paragraph; that’s the key. Many audits require the audit firm to add additional, explanatory language to the standard, unqualified (clean) opinion.

How do you know when an auditor’s report may be something other than a straightforward, no‐reservations clean opinion? Look for a fourth paragraph; that’s the key. Many audits require the audit firm to add additional, explanatory language to the standard, unqualified (clean) opinion.

One modification to an auditor’s report is very serious - when the audit firm expresses the view that it has substantial doubts about the capability of the business to continue as a going concern. A going concern is a business that has sufficient financial wherewithal and momentum to continue its normal operations into the foreseeable future and would be able to absorb a bad turn of events without having to default on its liabilities. A going concern doesn’t face an imminent financial crisis or any pressing financial emergency. A business could be under some financial distress, but overall still be judged a going concern. Unless there is evidence to the contrary, the auditor assumes that the business is a going concern.

One modification to an auditor’s report is very serious - when the audit firm expresses the view that it has substantial doubts about the capability of the business to continue as a going concern. A going concern is a business that has sufficient financial wherewithal and momentum to continue its normal operations into the foreseeable future and would be able to absorb a bad turn of events without having to default on its liabilities. A going concern doesn’t face an imminent financial crisis or any pressing financial emergency. A business could be under some financial distress, but overall still be judged a going concern. Unless there is evidence to the contrary, the auditor assumes that the business is a going concern.

But in some cases, the auditor may see unmistakable signs that a business is in deep financial waters and may not be able to convince its creditors and lenders to give it time to work itself out of its present financial difficulties. The creditors and lenders may force the business into involuntary bankruptcy, or the business may make a pre‐emptive move and take itself into voluntary bankruptcy. The equity owners (shareholders of a company) may end up holding an empty bag after the bankruptcy proceedings have concluded. (This is one of the risks that shareholders take.) If an auditor has serious concerns about whether the business is a going concern, these doubts are spelled out in the auditor’s report.

Auditors also point out any accounting methods that are inconsistent from one year to the next, whether their opinion is based in part on work done by another audit firm, on limitations on the scope of their audit work, on departures from the rules (if they’re not serious enough to warrant an adverse opinion) or on one of several other more technical matters. Generally, businesses - and auditors too - want to end up with a clean bill of health; anything less is bound to catch the attention of the people who read the financial statements. Every business wants to avoid that sort of attention if possible.

Do Audits Always Catch Fraud?

Business managers and investors should understand one thing: having an audit of a business’s financial statements doesn’t guarantee that all fraud, embezzlement, theft and dishonesty will be detected. Audits have to be cost‐effective; auditors can’t examine every transaction that occurred during the year. Instead, auditors carefully evaluate businesses’ internal controls and rely on sampling - they examine only a relatively small portion of transactions closely and in depth. The sample may not include the transactions that would tip off the auditor that something is wrong, however. Perpetrators of fraud and embezzlement are usually clever in concealing their wrongdoing and often prepare fake evidence to cover their tracks.

Looking for errors and fraud

Auditors look in the high‐risk areas where fraud and embezzlement are most likely to occur and in areas where the company’s internal controls are weak. But again, auditors can’t catch everything. High‐level management fraud is extraordinarily difficult to detect because auditors rely a great deal on management explanations and assurances about the business. Top‐level executives may lie to auditors, deliberately mislead them and conceal things that they don’t want auditors to find out about. Auditors have a particularly difficult time detecting management fraud.

Under tougher auditing standards adopted recently, auditors have to develop a detailed and definite plan to search for indicators of fraud, and they have to document the search procedures and findings in their audit working papers. Searching is one thing, but actually finding fraud is quite another. In many cases high‐level management fraud went on for some time before it was discovered, usually not by auditors. The new auditing standard was expected to lead to more effective audit procedures that would reduce undetected fraud.

Unfortunately, it doesn’t appear that things have improved. Articles in the financial press since then have exposed many cases of accounting and management fraud that weren’t detected or, if known about, weren’t objected to by the auditors. This is most disturbing. It’s difficult to understand how these audit failures and breakdowns happened. The trail of facts is hard to follow in each case, especially by just reading what’s reported in the press. Nevertheless, we’d say that two basic reasons explain why audits fail to find fraud.

First, business managers are aware that an audit relies on a very limited sampling from the large number of transactions. They know that only a needle‐in‐the‐haystack chance exists of fraudulent transactions being selected for an in‐depth examination by the auditor. Second, managers are in a position to cover their tracks - to conceal evidence and to fabricate false evidence. In short, well‐designed and well‐executed management fraud is extraordinarily difficult to uncover by ordinary audit procedures. Call this audit evidence failure; the auditor didn’t know about the fraud.

In other situations, the auditor did know what was going on but didn’t act on it - call this an audit judgement failure. In these cases, the auditor was overly tolerant of wrong accounting methods used by the client. The auditor may have had serious objections to the accounting methods, but the client persuaded the auditor to go along with the methods.

What happens when auditors spot fraud

In the course of doing an audit, the audit firm may make the following discoveries:

· Errors in recording transactions: These honest mistakes happen from time to time because of inexperienced bookkeepers, or poorly trained accountants, or simple failure to pay attention to details. No one is stealing money or other assets or defrauding the business. Management wants the errors corrected and wants to prevent them from happening again.

· Theft, embezzlement and fraud against the business: This kind of dishonesty takes advantage of weak internal controls or involves the abuse of positions of authority in the organisation that top management didn’t know about and wasn’t involved in. Management may take action against the guilty parties.

· Accounting fraud (also called financial fraud or financial reporting fraud): This refers to top‐level managers who know about and approve the use of misleading and invalid accounting methods for the purpose of disguising the business’s financial problems or artificially inflating profit. Often, managers benefit from these improper accounting methods - by propping up the market price of the company’s shares to make their stock options more valuable, for example.

· Management fraud: In the broadest sense this includes accounting fraud, but in a more focused sense it refers to high‐level business managers engaging in illegal schemes to line their pockets at the business’s expense or knowingly violating laws and regulations that put the business at risk of large criminal or civil penalties. A manager may conspire with competitors to fix prices or divide the market, for example. Accepting kickbacks or bribes from customers is an example of management fraud - although most management fraud is more sophisticated than taking under‐the‐table payments.

When the first two types of problems are discovered, the auditor’s follow‐up is straightforward. Errors are corrected, and the loss from the crime against the business is recorded. (Such a loss may be a problem if it’s so large that the auditor thinks it should be disclosed separately in the financial report but the business disagrees and doesn’t want to call attention to the loss.) In contrast, the auditor is between a rock and a hard place when accounting or management fraud is uncovered.

When an auditor discovers accounting or management fraud, the business has to clean up the fraud mess as best it can - which often involves recording a loss. Of course, the business should make changes to prevent the fraud from occurring again. And it may request the resignations of those responsible or even take legal action against those employees. Assuming that the fraud loss is recorded and reported correctly in the financial statements, the auditor then issues a clean opinion on the financial statements. But auditors can withhold a clean opinion and threaten to issue a qualified or adverse opinion if the client does not deal with the matter in a satisfactory manner in its financial statements. That’s the auditor’s real clout.

The most serious type of accounting fraud occurs when profit is substantially overstated, with the result that the market value of the corporation’s shares was based on inflated profit numbers. Another type of accounting fraud occurs when a business is in deep financial trouble but its Balance Sheet disguises the trouble and makes things look much better than they really are. The business may be on the verge of financial failure, but the Balance Sheet gives no clue. When the fraud comes out into the open, the market value takes a plunge, and the investors call their lawyers and sue the business and the auditor.

Investing money in a business or shares issued by a public business involves many risks. The risk of misleading financial statements is just one of many dangers that investors face. A business may have accurate and truthful financial statements but end up in the tank because of bad management, bad products, poor marketing or just bad luck.

All in all, audited financial statements that carry a clean opinion (the best possible auditor’s report) are reliable indicators for investors to use - especially because auditors are held accountable for their reports and can be sued for careless audit procedures. (In fact, accountancy firms have had to pay many millions of pounds in malpractice lawsuit damages over the past 30 years, and Arthur Andersen was actually driven out of business.) Auditors usually handle clients for years, if not decades - PricewaterhouseCoopers LLP have been Sainsbury’s auditors since 1995 - so if anyone knows where the bodies are it’s the auditor. Therefore, don’t overlook the audit report as a tool for judging the reliability of a business’s financial statements. When you read the auditor’s report on the annual financial statements from your pension fund manager, hopefully you’ll be very reassured! That’s your retirement money they’re talking about, after all.

Auditors and the Rules

In the course of doing an audit, the accountant often catches certain accounting methods used by the client that violate the prevailing approved and authoritative methods and standards laid down by law that businesses must follow in preparing and reporting financial statements. All businesses are subject to these ground rules. An auditor calls to the attention of the business any departures from the rules, and he helps the business make adjustments to put its financial statements back on the right track. Sometimes a business may not want to make the changes that the auditor suggests because its profit numbers would be deflated. Professional standards demand that the auditor secure a change (assuming that the amount involved is material). If the client refuses to make a change to an acceptable accounting method, the accountant warns the financial report reader in the auditor’s report.

Auditors don’t allow their good names to be associated with financial reports that they know are misleading if they can possibly help it. Every now and then we read in the financial press about an audit firm walking away from a client (‘withdraws from the engagement’ is the official terminology). As mentioned earlier in this chapter, everything the auditor learns in the course of an audit is confidential and can’t be divulged beyond top management and the board of directors of the business. A confidential relationship exists between the auditor and the client - although it’s not equal to the privileged communication between lawyers and their clients.

If an auditor discovers a problem, he has the responsibility to move up the chain of command in the business organisation to make sure that one level higher than the source of the problem is informed of the problem. But the board of directors is the end of the line. The auditor doesn’t inform the LSE, the SEC or another regulatory agency of any confidential information learned during the audit.

However, most outside observers will work on the ‘no smoke without fire’ principle. No firm, yet alone an accountancy partnership with their partnership profit share on the line, willingly gives up a lucrative client.

Auditors, on the other hand, are frequently being replaced, often for cost reasons - auditing is a negotiable deal too - but also because the firm being audited may have simply outgrown the auditor. This happens fairly frequently when a business is going for a public listing of its shares. The guy round the corner, who was cheap and competent, cuts no ice with the big wheels at the LSE and the placing houses that have to sell the shares. They want a big name auditor to help the PR push.

We can’t exaggerate the importance of reliable financial statements that are prepared according to uniform standards and methods for measuring profit and putting values on assets, liabilities and owners’ equity. Not to put too fine a point on it, the flow of capital into businesses and the market prices of shares traded in the public markets (the LSE, the NYSE and over the NASDAQ network) depend on the information reported in financial statements.

Smaller, privately owned businesses would have a difficult time raising capital from owners and borrowing money from banks if no one could trust their financial statements. Generally accepted accounting principles, in short, are the gold standard for financial reporting. When financial reporting standards have been put into place, how are the standards enforced? To a large extent, the role of auditors is to do just that - to enforce the rules. The main purpose of having annual audits, in other words, is to keep businesses on the straight‐and‐narrow path and to prevent businesses from issuing misleading financial statements. Auditors are the guardians of the financial reporting rules. We think most business managers and investors agree that financial reporting would be in a sorry state if auditors weren’t around.

From Audits to Advising

If accountant Rip van Winkle woke up today after his 20‐year sleep, he’d be shocked to find that accountancy firms make most of their money not from doing audits but from advising clients. A recent advertisement by an international accountancy firm listed the following services: ‘assurance, business consulting, corporate finance, eBusiness, human capital, legal services, outsourcing, risk consulting and tax services’. (Now, if the firm could only help you with your back problems!) Do you see audits in this list? No? Well, it’s under the first category - assurance. Why have accountancy firms moved so far beyond audits into many different fields of consulting?

We suspect that many businesses don’t view audits as adding much value to their financial reports. True, having a clean opinion by an auditor on financial statements adds credibility to a financial report. At the same time, managers tend to view the audit as an intrusion, and an override on their prerogatives regarding how to account for profit and how to present the financial report of the business. Most audits, to be frank about it, involve a certain amount of tension between managers and the audit firm. After all, the essence of an audit is to second‐guess the business’s accounting methods and financial reporting decisions. So it’s quite understandable that accountancy firms have looked to other types of services they can provide to clients that are more value‐added and less adversarial - and that are more lucrative.

Nevertheless, many people have argued that accountancy firms should get out of the consulting and advising business - at least to the same clients they audit. For the first years of this millennium, things seemed to be moving in this direction, and new legislation gave them a none‐too‐gentle prod. Arthur Andersen only just split its consultancy business off before it went under itself. Luckily, it changed the name of the consulting business from Andersen to Accenture, ditching a fair amount of the bad odour that attached itself to the accountancy practice’s name. Now the pendulum is swinging back and big accountancy firms are pushing an integrated approach, arguing that clients don’t want to have to explain largely the same business facts to different teams of ‘visiting firemen’. Although the Big Four are back in the consulting game, figures from the Management Consultancies Association suggest that accountancy firms have only 16 per cent of the market for consultancy services, right now at least.

Sometimes we take the pessimistic view that in the long run accountants will abandon audits and do only taxes and consulting. Who will do audits then? Well, a team of governmental auditors could take over the task - but we don’t think this would be too popular.