Bookkeeping & Accounting All-in-One For Dummies (2015)

Book VI

Accountants: Working with the Outside World

Chapter 2

How Investors Read a Financial Report

In This Chapter

![]() Looking after your investments

Looking after your investments

![]() Keeping financial reports private versus making them public

Keeping financial reports private versus making them public

![]() Using ratios to understand profit performance

Using ratios to understand profit performance

![]() Using ratios to interpret financial condition and cash flow

Using ratios to interpret financial condition and cash flow

![]() Scanning footnotes and identifying the important ones

Scanning footnotes and identifying the important ones

![]() Paying attention to what the auditor has to say

Paying attention to what the auditor has to say

In reading financial reports, directors, managers, business owners and investors need to know how to navigate through the financial statements to find the vital signs of progress and problems. The financial statement ratios explained in this chapter point the way - these ratios are signposts on the financial information highway. You can also keep abreast of business affairs by reading financial newspapers and investment magazines, and investment newsletters are very popular. These sources of financial information refer to the ratios discussed in this chapter on the premise that you know what the ratios mean. Most managers or individual investors in public companies don’t have the time or expertise to study a financial report thoroughly enough to make decisions based on the report, so they rely on stockbrokers, investment advisers and publishers of credit ratings (like Standard & Poor’s) for interpretations of financial reports. The fact is that the folks who prepare financial reports have this kind of expert audience in mind; they don’t include explanations or mark passages with icons to help you understand the report.

Sure, you may have your own accountant or investment adviser on tap, so why should you bother reading this chapter if you rely on others to interpret financial reports anyway? Well, the more you understand the factors that go into interpreting a financial report, the better prepared you are to evaluate the commentary and advice of stock analysts and other investment experts. If you can at least nod intelligently while your stockbroker talks about a business’s P/E and EPS, you’ll look like a savvy investor - and may get more favourable treatment. (P/E and EPS, by the way, are two of the key ratios we explain later in the chapter.)

This chapter gives you the basics for comparing companies’ financial reports, including the points of difference between private and public companies, the important ratios that you should know about and the warning signs to look out for on audit reports. In this chapter, we also suggest how to sort through the footnotes that are an integral part of every financial report, to identify those that have the most importance to you. Believe us, the pros read the footnotes with a keen eye.

Financial Reporting by Private versus Public Businesses

The main impetus behind the continued development of generally accepted accounting principles (GAAP) has been the widespread public ownership and trading in the securities (stocks and bonds) issued by thousands of companies. The 1929 stock market crash and its aftermath plainly exposed the lack of accounting standards, as well as many financial reporting abuses and frauds. Landmark federal securities laws were passed in the US in 1933 and 1934, and a federal regulatory agency with broad powers - the Securities and Exchange Commission (SEC) - was created and given jurisdiction over trading in corporate securities. In the UK, the government has enacted a series of Companies Acts, culminating in one consolidated act in 2006, that have strengthened the protection for shareholders. Financial reports and other information must be filed with the London Stock Exchange or the relevant authorities elsewhere, such as the SEC in the US, and made available to the investing public.

The main impetus behind the continued development of generally accepted accounting principles (GAAP) has been the widespread public ownership and trading in the securities (stocks and bonds) issued by thousands of companies. The 1929 stock market crash and its aftermath plainly exposed the lack of accounting standards, as well as many financial reporting abuses and frauds. Landmark federal securities laws were passed in the US in 1933 and 1934, and a federal regulatory agency with broad powers - the Securities and Exchange Commission (SEC) - was created and given jurisdiction over trading in corporate securities. In the UK, the government has enacted a series of Companies Acts, culminating in one consolidated act in 2006, that have strengthened the protection for shareholders. Financial reports and other information must be filed with the London Stock Exchange or the relevant authorities elsewhere, such as the SEC in the US, and made available to the investing public.

Accounting standards aren’t limited to public companies whose securities are traded on public exchanges, such as the London and New York Stock Exchanges and NASDAQ. These financial accounting and reporting standards apply with equal force and authority to private businesses whose ownership shares aren’t traded in any open market. When the shareholders of a private business receive its periodic financial reports, they’re entitled to assume that the company’s financial statements and footnotes are prepared in accordance with the accounting rules in force at the time. Even following the rules leave a fair amount of wriggle room - look back to Book V, Chapter 2 if you need a refresher on this subject. So it always pays to check over the figures yourself to be sure of what’s really going on. The bare-bones content of a private business’s annual financial report includes the three primary financial statements (Balance Sheet, Profit and Loss statement, and cash flow statement) plus several footnotes. We’ve seen many private company financial reports that don’t even have a letter from the chairman - just the three financial statements plus a few footnotes and nothing more. In fact, we’ve seen financial reports of private businesses (mostly small companies) that don’t even include a cash flow statement; only the Balance Sheet and Profit and Loss statement are presented. Omitting a cash flow statement violates the rules - but the company’s shareholders and its lenders may not demand to see the cash flow statement, so the company can get away with it.

Accounting standards aren’t limited to public companies whose securities are traded on public exchanges, such as the London and New York Stock Exchanges and NASDAQ. These financial accounting and reporting standards apply with equal force and authority to private businesses whose ownership shares aren’t traded in any open market. When the shareholders of a private business receive its periodic financial reports, they’re entitled to assume that the company’s financial statements and footnotes are prepared in accordance with the accounting rules in force at the time. Even following the rules leave a fair amount of wriggle room - look back to Book V, Chapter 2 if you need a refresher on this subject. So it always pays to check over the figures yourself to be sure of what’s really going on. The bare-bones content of a private business’s annual financial report includes the three primary financial statements (Balance Sheet, Profit and Loss statement, and cash flow statement) plus several footnotes. We’ve seen many private company financial reports that don’t even have a letter from the chairman - just the three financial statements plus a few footnotes and nothing more. In fact, we’ve seen financial reports of private businesses (mostly small companies) that don’t even include a cash flow statement; only the Balance Sheet and Profit and Loss statement are presented. Omitting a cash flow statement violates the rules - but the company’s shareholders and its lenders may not demand to see the cash flow statement, so the company can get away with it.

Publicly owned businesses must comply with an additional layer of rules and requirements that don’t apply to privately owned businesses. These rules are issued by the Stock Exchange, the agency that regulates financial reporting and trading in stocks and bonds of publicly owned businesses. The Stock Exchange has no jurisdiction over private businesses; those businesses need only worry about GAAP, which don’t have many hard-and-fast rules about financial report formats. Public businesses have to file financial reports and other forms with the Stock Exchange that are made available to the public. These filings are available to the public on the London Stock Exchange’s website (www.londonstockexchange.com) or for US companies on the Securities Exchange Commission’s (SEC’s) EDGAR database at the SEC’s website (www.sec.gov/edgar/quickedgar.htm).

Publicly owned businesses must comply with an additional layer of rules and requirements that don’t apply to privately owned businesses. These rules are issued by the Stock Exchange, the agency that regulates financial reporting and trading in stocks and bonds of publicly owned businesses. The Stock Exchange has no jurisdiction over private businesses; those businesses need only worry about GAAP, which don’t have many hard-and-fast rules about financial report formats. Public businesses have to file financial reports and other forms with the Stock Exchange that are made available to the public. These filings are available to the public on the London Stock Exchange’s website (www.londonstockexchange.com) or for US companies on the Securities Exchange Commission’s (SEC’s) EDGAR database at the SEC’s website (www.sec.gov/edgar/quickedgar.htm).

The best known of these forms is the annual 10-K, which includes the business’s annual financial statements in prescribed formats with all the supporting schedules and detailed disclosures that the SEC requires.

Here are some (but not all) of the main financial reporting requirements that publicly owned businesses must adhere to. (Private businesses may include these items as well if they want, but they generally don’t.)

· Management discussion and analysis (MD&A) section: Presents the top managers’ interpretation and analysis of a business’s profit performance and other important financial developments over the year.

· Earnings per share (EPS): The only ratio that a public business is required to report, although most public businesses do report a few other ratios as well. See ‘Earnings per share, basic and diluted’, later in this chapter. Note that private businesses’ reports generally don’t include any ratios (but you can, of course, compute the ratios yourself).

· Three-year comparative Profit and Loss statements: See Book IV, Chapter 1 for more information about Profit and Loss statements.

Note: A publicly owned business can make the required filings with the Stock Exchange or SEC and then prepare a different annual financial report for its shareholders, thus preparing two sets of financial reports. This is common practice. However, the financial information in the two documents can’t differ in any material way. A typical annual financial report to shareholders is a glossy booklet with excellent art and graphic design including high-quality photographs. The company’s products are promoted and its people are featured in glowing terms that describe teamwork, creativity and innovation - we’re sure you get the picture. In contrast, the reports to the London Stock Exchange or SEC look like legal briefs - nothing fancy in these filings. The core of financial statements and footnotes (plus certain other information) is the same in both the Stock Exchange filings and the annual reports to shareholders. The Stock Exchange filings contain more information about certain expenses and require much more disclosure about the history of the business, its main markets and competitors, its principal officers, any major changes on the horizon and so on. Professional investors and investment managers read the Stock Exchange filings.

Most public companies solicit their shareholders’ votes in the annual election of persons to the board of directors (whom the business has nominated) and on other matters that must be put to a vote at the annual shareholders’ meeting. The method of communication for doing so is called a proxy statement - the reason being that the shareholders give their votes to a proxy, or designated person, who actually casts the votes at the annual meeting. The Stock Exchange requires many disclosures in proxy statements that aren’t found in annual financial reports issued to shareholders or in the business’s annual accounts filed at Companies House. For example, compensation paid to the top-level officers of the business must be disclosed, as well as their shareholdings. If you own shares in a public company, take the time to read through all the financial statements you receive through the post and any others you can get your hands on.

Most public companies solicit their shareholders’ votes in the annual election of persons to the board of directors (whom the business has nominated) and on other matters that must be put to a vote at the annual shareholders’ meeting. The method of communication for doing so is called a proxy statement - the reason being that the shareholders give their votes to a proxy, or designated person, who actually casts the votes at the annual meeting. The Stock Exchange requires many disclosures in proxy statements that aren’t found in annual financial reports issued to shareholders or in the business’s annual accounts filed at Companies House. For example, compensation paid to the top-level officers of the business must be disclosed, as well as their shareholdings. If you own shares in a public company, take the time to read through all the financial statements you receive through the post and any others you can get your hands on.

Analysing Financial Reports with Ratios

Financial reports have lots of numbers in them. (Duh!) The significance of many of these numbers isn’t clear unless they’re compared with other numbers in the financial statements to determine the relative size of one number to another number. One very useful way of interpreting financial reports is to compute ratios - that is, to divide a particular number in the financial report by another. Financial report ratios are also useful because they enable you to compare a business’s current performance with its past performance or with another business’s performance, regardless of whether sales revenue or net profit was bigger or smaller for the other years or the other business. In other words, using ratios cancels out size differences.

The following sections explain the ten financial statement ratios that you’re most likely to run into. Here’s a general overview of why these ratios are important:

· Gross margin ratio and profit ratio: You use these ratios to measure a business’s profit performance with respect to its sales revenue. Sales revenue is the starting point for making profit; these ratios measure the percentage of total sales revenue that is left over as profit.

· Earnings per share (EPS), price/earnings (P/E) ratio and dividend yield: These three ratios revolve around the market price of shares, and anyone who invests in publicly owned businesses should be intimately familiar with them. As an investor, your main concern is the return you receive on your invested capital. Return on capital consists of two elements:

· Periodic cash dividends distributed by the business

· Increase (or decrease) in the market price of the shares

· Dividends and market prices depend on earnings - and there you have the relationship among these three ratios and why they’re so important to you, the investor. Major newspapers report P/E ratios and dividend yields in their stock market activity tables; stockbrokers’ investment reports focus mainly on forecasts of EPS and dividend yield.

· Book value per share and return on equity (ROE): Shares for private businesses have no ready market price, so investors in these businesses use the ROE ratio, which is based on the value of their ownership equity reported in the Balance Sheet, to measure investment performance. Without a market price for the shares of a private business, the P/E ratio can’t be determined. EPS can easily be determined for a private business but doesn’t have to be reported in its Profit and Loss statement.

· Current ratio and acid-test ratio: These ratios indicate whether a business should have enough cash to pay its liabilities.

· Return on assets (ROA): This ratio is the first step in determining how well a business is using its capital and whether it’s earning more than the interest rate on its debt, which causes financial leverage gain (or loss).

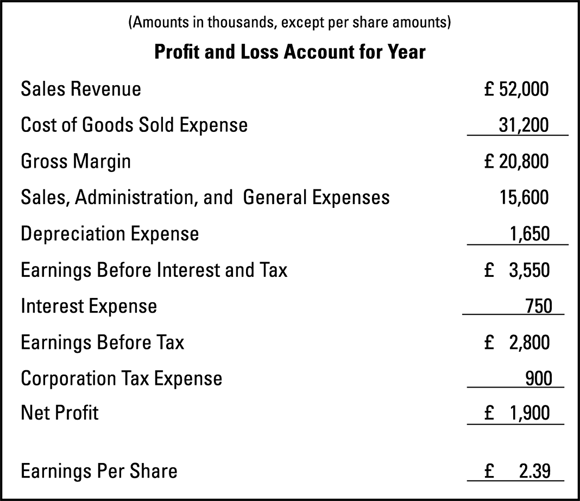

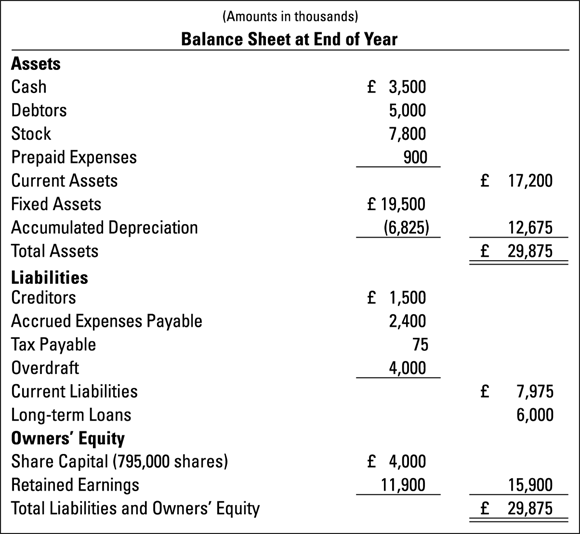

To demonstrate these ratios, we use the Profit and Loss statement (shown in Figure 2-1) and the Balance Sheet of a business (shown in Figure 2-2). Notice that a cash flow statement isn’t presented here - mainly because no ratios are calculated from data in the cash flow statement. (Refer to the sidebar, ‘The temptation to compute cash flow per share: Don’t give in!’) The footnotes to the company’s financial statements aren’t presented here, but the use of footnotes is discussed in the following sections.

Figure 2-1: A sample Profit and Loss statement.

Figure 2-2: A sample Balance Sheet.

Gross margin ratio

Making bottom-line profit begins with making sales and earning enough gross margin from those sales, as explained in Book V, Chapter 3. In other words, a business must set its sales prices high enough over product costs to yield satisfactory gross margins on its products, because the business has to worry about many more expenses of making sales and running the business, plus interest expense and income tax expense. You calculate the gross margin ratio as follows:

· Gross margin ÷ Sales revenue = Gross margin ratio

So a business with a £20.8 million gross margin and £52 million in sales revenue (refer to Figure 2-1) ends up with a 40 per cent gross margin ratio. Now, if the business had only been able to earn a 41 per cent gross margin, that one additional point (one point is 1 per cent) would have caused a jump in its gross margin of £520,000 (1 per cent × £52 million sales revenue) - which would have trickled down to earnings before income tax. Earnings before income tax would have been 19 per cent higher (a £520,000 bump in gross margin ÷ £2.8 million income before income tax). Never underestimate the impact of even a small improvement in the gross margin ratio!

So a business with a £20.8 million gross margin and £52 million in sales revenue (refer to Figure 2-1) ends up with a 40 per cent gross margin ratio. Now, if the business had only been able to earn a 41 per cent gross margin, that one additional point (one point is 1 per cent) would have caused a jump in its gross margin of £520,000 (1 per cent × £52 million sales revenue) - which would have trickled down to earnings before income tax. Earnings before income tax would have been 19 per cent higher (a £520,000 bump in gross margin ÷ £2.8 million income before income tax). Never underestimate the impact of even a small improvement in the gross margin ratio!

Outside investors know only the information disclosed in the external financial report that the business releases. They can’t do much more than compare the gross margin for the two- or three-yearly Profit and Loss statements included in the annual financial report. Although publicly owned businesses are required to include a management discussion and analysis (MD&A) section that should comment on any significant change in the gross margin ratio, corporate managers have wide latitude in deciding what exactly to discuss and how much detail to go into. You definitely should read the MD&A section, but it may not provide all the answers you’re looking for. You have to search further in stockbroker releases, in articles in the financial press or at the next professional business meeting you attend.

Outside investors know only the information disclosed in the external financial report that the business releases. They can’t do much more than compare the gross margin for the two- or three-yearly Profit and Loss statements included in the annual financial report. Although publicly owned businesses are required to include a management discussion and analysis (MD&A) section that should comment on any significant change in the gross margin ratio, corporate managers have wide latitude in deciding what exactly to discuss and how much detail to go into. You definitely should read the MD&A section, but it may not provide all the answers you’re looking for. You have to search further in stockbroker releases, in articles in the financial press or at the next professional business meeting you attend.

As explained in Book V, Chapter 3, managers focus on contribution margin per unit and total contribution margin to control and improve profit performance business. Contribution margin equals sales revenue minus product cost and other variable operating expenses of the business. Contribution margin is profit before the company’s total fixed costs for the period are deducted. Changes in the contribution margins per unit of the products sold by a business and changes in its total fixed costs are extremely important information in managing profit.

However, businesses don’t disclose contribution margin information in their external financial reports - they wouldn’t even think of doing so. This information is considered to be proprietary in nature; it should be kept confidential and out of the hands of its competitors. In short, investors don’t have access to information about the business’s contribution margin. Neither accounting standards nor the Stock Exchange requires that such information be disclosed. The external Profit and Loss statement discloses gross margin and operating profit, or earnings before interest and income tax expenses. However, the expenses between these two profit lines in the Profit and Loss statement aren’t separated between variable and fixed (refer to Figure 2-1).

Profit ratio

Business is motivated by profit, so the profit ratio is very important to say the least. The profit ratio indicates how much net profit was earned on each £100 of sales revenue:

· Net profit ÷ Sales revenue = Profit ratio

For example, the business in Figure 2-1 earned £1.9 million net profit from its £52 million sales revenue, so its profit ratio is 3.65 per cent, meaning that the business earned £3.65 net profit for each £100 of sales revenue.

A seemingly small change in the profit ratio can have a big impact on the bottom line. Suppose that this business had earned a profit ratio of 5 per cent instead of 3.65 per cent. That increase in the profit ratio translates into a £700,000 increase in bottom-line profit (net profit) on the same sales revenue.

Profit ratios vary widely from industry to industry. A 5-10 per cent profit ratio is common in most industries, although some high-volume retailers, such as supermarkets, are satisfied with profit ratios around 1 per cent or 2 per cent.

You can turn any ratio upside down and come up with a new way of looking at the same information. If you flip the profit ratio over to be sales revenue divided by net profit, the result is the amount of sales revenue needed to make £1 profit. Using the same example, £52 million sales revenue ÷ £1.9 million net profit = 27.37 to 1 upside-down profit ratio, which means that this business needs £27.37 in sales to make £1 profit. So you can say that net profit is 3.65 per cent of sales revenue, or you can say that sales revenue is 27.37 times net profit - but the standard profit ratio is expressed as net profit divided by sales revenue.

Earnings per share, basic and diluted

Publicly owned businesses, according to generally accepted accounting principles (GAAP), must report earnings per share (EPS) below the net profit line in their Profit and Loss statements - giving EPS a certain distinction among the ratios. Why is EPS considered so important? Because it gives investors a means of determining the amount the business earned on its share investments: EPS tells you how much net profit the business earned for each share you own. The essential equation for EPS is as follows:

· Net profit ÷ Total number of capital stock shares = EPS

For the example in Figures 2-1 and 2-2, the company’s £1.9 million net profit is divided by the 795,000 shares of stock the business has issued to compute its £2.39 EPS.

Note: Private businesses don’t have to report EPS if they don’t want to. Considering the wide range of issues covered by GAAP, you find surprisingly few distinctions between private and public businesses - these authoritative accounting rules apply to all businesses. But EPS is one area where GAAP makes an exception for privately owned businesses. EPS is extraordinarily important to the shareholders of businesses whose shares are publicly traded. These shareholders focus on market price per share. They want the total net profit of the business to be communicated to them on a per-share basis so that they can easily compare it with the market price of their shares. The shares of privately owned companies aren’t actively traded, so there’s no readily available market value for their shares. The thinking behind the rule that privately owned businesses shouldn’t have to report EPS is that their shareholders don’t focus on per share values and are more interested in the business’s total net profit performance.

The business in the example is too small to be publicly owned. So we turn here to a larger public company example. This publicly owned company reports that it earned £1.32 billion net profit for the year just ended. At the end of the year, this company has 400 million shares outstanding, which refers to the number of shares that have been issued and are owned by its shareholders. Thus, its EPS is £3.30 (£1.32 billion net profit ÷ 400 million stock shares). But here’s a complication: the business is committed to issuing additional capital shares in the future for share options that the company has granted to its managers, and it has borrowed money on the basis of debt instruments that give the lenders the right to convert the debt into its capital stock. Under terms of its management share options and its convertible debt, the business could have to issue 40 million additional capital shares in the future. Dividing net profit by the number of shares outstanding plus the number of shares that could be issued in the future gives the following computation of EPS:

· £1.32 billion net profit ÷ 440 million capital stock shares = £3.00 EPS

This second computation, based on the higher number of shares, is called the diluted earnings per share. (Diluted means thinned out or spread over a larger number of shares.) The first computation, based on the number of shares actually outstanding, is called basic earnings per share. Publicly owned businesses have to report two EPS figures - unless they have a simple capital structure that doesn’t require the business to issue additional shares in the future. Generally, publicly owned companies have complex capital structures and have to report two EPS figures. Both are reported at the bottom of the Profit and Loss statement. So the company in this example reports £3.30 basic EPS and £3.00 diluted EPS. Sometimes it’s not clear which of the two EPS figures is being used in press releases and in articles giving investment advice. Fortunately, The Financial Times and most other major financial publications leave a clear trail of both EPS figures.

Calculating basic and diluted EPS isn’t always as simple as our examples may suggest. An accountant would have to adjust the EPS equation for the following complicating things that a business may do:

· Issue additional shares during the year and buy back some of its shares (shares of its stock owned by the business itself that aren’t formally cancelled are called treasury stock).

· Issue more than one class of share, causing net profit to be divided into two or more pools - one pool for each class of share.

· Go through a merger (business combination) in which a large number of shares are issued to acquire the other business.

The shareholders should draw comfort from the fact that the top management of many businesses in which they invest are probably just as anxiously reviewing EPS performance as they are. This extract from Tesco’s annual accounts reveals much:

Annual bonuses based on achieving stretching EPS growth targets and specific corporate objectives.

Annual bonuses are paid in shares. On award, the Executive can elect to defer receipt of the shares for a further two years, which is encouraged, with additional matching share awards.

Longer-term bonus based on a combination of relative total shareholder return, and the achievement of stretching EPS growth targets and specific corporate objectives. Longer-term bonuses are paid in shares, which must be held for a further four years. Executive Directors are encouraged to hold shares for longer than four years with additional matching share awards. Further details are provided below.

Share options are granted to Executive Directors at market value and can only be exercised if EPS growth exceeds Retail Price Index (RPI) plus 9 per cent over any three years from grant.

Executive Directors are required to build and hold a shareholding with a value at least equal to their basic salary; full participation in the Executive Incentive scheme is conditional upon meeting this target.

Price/earnings (P/E) ratio

The price/earnings (P/E) ratio is another ratio that’s of particular interest to investors in public businesses. The P/E ratio gives you an idea of how much you’re paying in the current price for the shares for each pound of earnings, or net profit, being earned by the business. Remember that earnings prop up the market value of shares, not the book value of the shares that’s reported in the Balance Sheet. (Read on for the book value per share discussion.)

The P/E ratio is, in one sense, a reality check on just how high the current market price is in relation to the underlying profit that the business is earning. Extraordinarily high P/E ratios are justified only when investors think that the company’s EPS has a lot of upside potential in the future.

The P/E ratio is calculated as follows:

· Current market price of stock ÷ Most recent trailing 12 months diluted EPS = P/E ratio

If the business has a simple capital structure and doesn’t report a diluted EPS, its basic EPS is used for calculating its P/E ratio. (See the earlier section ‘Earnings per share, basic and diluted’.)

Assume that the stock shares of a public business with a £3.65 diluted EPS are selling at £54.75 in the stock market. Note: From here forward, we’ll use the briefer term EPS in reference to P/E ratios; we assume you understand that it refers to diluted EPS for businesses with complex capital structures and to basic EPS for businesses with simple capital structures.

The actual share price bounces around day to day and is subject to change on short notice. To illustrate the P/E ratio, we use this price, which is the closing price on the latest trading day in the stock market. This market price means that investors trading in the stock think that the shares are worth 15 times diluted EPS (£54.75 market price ÷ £3.65 diluted EPS = 15). This value may be below the broad market average that values shares at, say, 20 times EPS. The outlook for future growth in its EPS is probably not too good.

Market cap - not a cap on market value

One investment number you see a lot in the financial press is the market cap. No, this doesn’t refer to a cap, or limit, on the market value of a company’s capital shares. The term is shorthand for market capitalisation, which refers to the total market value of the business that is determined by multiplying the stock’s current market price by the total number of shares issued by the company. Suppose a company’s stock is selling at £50 per share in the stock market and it has 200 million shares outstanding. Its market cap is £10 billion. Another business may be willing to pay higher than £50 per share for the company. Indeed, many acquisitions and mergers involve the acquiring company paying a hefty premium over the going market price of the shares of the company being acquired.

Dividend yield

The dividend yield tells investors how much cash flow income they’re receiving on their investment. (The dividend is the cash flow income part of investment return; the other part is the gain or loss in the market value of the investment over the year.)

Suppose that a stock of a public company that is selling for £60 paid £1.20 cash dividends per share over the last year. You calculate dividend yield as follows:

· £1.20 annual cash dividend per share ÷ £60 current market price of stock = 2% dividend yield

You use dividend yield to compare how your stock investment is doing to how it would be doing if you’d put that money in corporate or Treasury bonds, gilt-edged stock (UK government borrowings) or other debt securities that pay interest. The average interest rate of high-grade debt securities has recently been three to four times the dividend yields on most public companies; in theory, market price appreciation of the shares over time makes up for that gap. Of course, shareholders take the risk that the market value won’t increase enough to make their total return on investment rate higher than a benchmark interest rate. (At the time of writing, this yield gap has shrunk to nothing and is causing an agonising reappraisal of the value of equities in relation to debt as an investment medium.)

Assume that long-term government gilt-edged stock is currently paying 6 per cent annual interest, which is 4 per cent higher than the business’s 2 per cent dividend yield in the example just discussed. If this business’s shares don’t increase in value by at least 4 per cent over the year, its investors would have been better off investing in the debt securities instead. (Of course, they wouldn’t have had all the perks of a share investment, like those heartfelt letters from the chairman and those glossy financial reports.) The market price of publicly traded debt securities can fall or rise, so things get a little tricky in this sort of investment analysis.

Book value per share

Book value per share is one measure, but it’s certainly not the only amount, used for determining the value of a privately owned business’s shares. The asset values that a business records in its books (also known as its accounts) are not the amounts that a business could get if it put its assets up for sale. Book values of some assets are generally lower than what the cost would be for replacing the assets if a disaster (such as a flood or a fire) wiped out the business’s stock or equipment. Recording current market values in the books is really not a practical option. Until a seller and a buyer meet and haggle over price, trying to determine the market price for a privately owned business’s shares is awfully hard.

You can calculate book value per share for publicly owned businesses too. However, market value is readily available, so shareholders (and investment advisers and managers) don’t put much weight on book value per share. EPS is the main factor that affects the market prices of stock shares of public companies - not the book value per share. We should add that some investing strategies, known as value investing, search out companies that have a high book value per share compared to their going market prices. But by and large, book value per share plays a secondary role in the market values of stock shares issued by public companies.

Although book value per share is generally not a good indicator of the market value of a private business’s shares, you do run into this ratio, at least as a starting point for haggling over a selling price. Here’s how to calculate book value per share:

· Total owners’ equity ÷ Total number of stock shares = Book value per share

The business shown in Figure 2-2 has issued 795,000 shares: its £15.9 million total owners’ equity divided by its 795,000 shares gives a book value per share of £20. If the business sold off its assets exactly for their book values and paid all its liabilities, it would end up with £15.9 million left for the shareholders, and it could therefore distribute £20 per share. But the company won’t go out of business and liquidate its assets and pay off its liabilities. So book value per share is a theoretical value. It’s not totally irrelevant, but it’s not all that definitive, either.

Return on equity (ROE) ratio

The return on equity (ROE) ratio tells you how much profit a business earned in comparison to the book value of shareholders’ equity. This ratio is useful for privately owned businesses, which have no way of determining the current value of owners’ equity (at least not until the business is actually sold). ROE is also calculated for public companies, but, just like book value per share, it plays a secondary role and isn’t the dominant factor driving market prices. (Earnings are.) Here’s how you calculate this key ratio:

· Net profit ÷ Owners’ equity = ROE

The owners’ equity figure is at book value, which is reported in the company’s Balance Sheet.

The owners’ equity figure is at book value, which is reported in the company’s Balance Sheet.

The business whose Profit and Loss statement and Balance Sheet are shown in Figures 2-1 and 2-2 earned £1.9 million net profit for the year just ended and has £15.9 million owners’ equity. Therefore, its ROE is 11.95 per cent (£1.9 million net profit ÷ £15.9 million owners’ equity = 11.95 per cent). ROE is net profit expressed as a percentage of the amount of total owners’ equity of the business, which is one of the two sources of capital to the business, the other being borrowed money, or interest-bearing debt. (A business also has non-interest-bearing operating liabilities, such as creditors.) The cost of debt capital (interest) is deducted as an expense to determine net profit. So net profit ‘belongs’ to the owners; it increases their equity in the business, so it makes sense to express net profit as the percentage of improvement in the owners’ equity.

Gearing or leverage

Your company’s liquidity keeps you solvent from day to day and month to month, and we come to that next when we look at the current ratio and acid test. But what about your ability to pay back long-term debt year after year? Two financial ratios indicate what kind of shape you’re in over the long term.

If you’ve read this chapter from the beginning, you may be getting really bored with financial ratios by now, but your lenders - bankers and bondholders, if you have them - find these long-term ratios to be incredibly fascinating, for obvious reasons.

The first ratio gauges how easy it is for your company to continue making interest payments on the debt:

· Times interest earned = Earnings before interest and taxes ÷ Interest expense

Don’t get confused - earnings before any interest expense and taxes are paid (EBIT) is really just the profit that you have available to make those interest payments in the first place. Figure 2-1, for example, shows an EBIT of £3.55Million and an interest expense of £750,000 this year for a times-interest-earned ratio of 4.73. In other words, this business can meet its interest expense 4.73 times over.

You may also hear the same number called an interest coverage. Lenders get mighty nervous if this ratio ever gets anywhere close to 1.0, because at that point, every last penny of profits goes for interest payments on the long-term debt.

The second ratio tries to determine whether the principal amount of your debt is in any danger:

· Debt-to-equity ratio = Long-term liabilities ÷ Owners’ equity

The debt-to-equity ratio says a great deal about the general financial structure of your company. After all, you can raise money to support your company in only two ways: borrow it and promise to pay it back with interest, or sell pieces of the company and promise to share all the rewards of ownership. The first method is debt; the second, equity.

Figure 2-2, for example, shows a debt-to-equity ratio of £6,000 divided by £15,900, or 0.38. This ratio means that the company has around three times more equity financing than it does long-term debt.

Lenders love to see lots of equity supporting a company’s debt because then they know that the money they loan out is safer. If something goes wrong with the company, they can go after the owners’ money. Equity investors, on the other hand, actually want to take on some risk. They like to see relatively high debt-to-equity ratios because that situation increases their leverage and (as the following section points out) can substantially boost their profits. So the debt-to-equity ratio that’s just right for your company depends not only on your industry and how stable it is, but also on who you ask.

Current ratio

The current ratio is a test of a business’s short-term solvency - its capability to pay off its liabilities that come due in the near future (up to one year). The ratio is a rough indicator of whether cash on hand plus the cash flow from collecting debtors and selling stock will be enough to pay off the liabilities that will come due in the next period.

As you can imagine, lenders are particularly keen on punching in the numbers to calculate the current ratio. Here’s how they do it:

· Current assets ÷ Current liabilities = Current ratio

Note: Unlike with most of the other ratios, you don’t multiply the result of this equation by 100 and represent it as a percentage.

Businesses are expected by their creditors to maintain a minimum current ratio (2.0, meaning a 2-to-1 ratio, is the general rule) and may be legally required to stay above a minimum current ratio as stipulated in their contracts with lenders. The business in Figure 2-2 has £17.2 million in current assets and £7,975,000 in current liabilities, so its current ratio is 2.16 and it shouldn’t have to worry about lenders coming by in the middle of the night to break its legs.

How much working capital, ready or nearly ready money do you need to ensure survival? Having the liquid assets available when you absolutely need them to meet short-term obligations is called liquidity. You don’t have to have cash in the till to be liquid. Debtors (that is, people who owe you money and can be reasonably expected to cough up soon) and stock ready to be sold are both part of your liquid assets. You can use several financial ratios to test a business’s liquidity, including the current ratio and the acid test. You can monitor these ratios year by year and measure them against your competitors’ ratios and the industry averages.

Acid-test ratio

Most serious investors and lenders don’t stop with the current ratio for an indication of the business’s short-term solvency - its capability to pay the liabilities that will come due in the short term. Investors also calculate the acid-test ratio (also known as the quick ratio or the pounce ratio), which is a more severe test of a business’s solvency than the current ratio. The acid-test ratio excludes stock and prepaid expenses, which the current ratio includes, and limits assets to cash and items that the business can quickly convert to cash. This limited category of assets is known as quick or liquid assets.

You calculate the acid-test ratio as follows:

· Liquid assets ÷ Total current liabilities = Acid-test ratio

Note: Unlike most other financial ratios, you don’t multiply the result of this equation by 100 and represent it as a percentage.

For the business example shown in Figure 2-2, the acid-test ratio is as follows:

|

Cash |

£3,500,000 |

|

Marketable securities |

none |

|

Debtors |

5,000,000 |

|

Total liquid assets |

£8,500,000 |

|

Total current liabilities |

£7,975,000 |

|

Acid-test ratio |

1.07 |

A 1.07 acid-test ratio means that the business would be able to pay off its short-term liabilities and still have a little bit of liquid assets left over. The general rule is that the acid-test ratio should be at least 1.0, which means that liquid assets equal current liabilities. Of course, falling below 1.0 doesn’t mean that the business is on the verge of bankruptcy, but if the ratio falls as low as 0.5, that may be cause for alarm.

This ratio is also known as the pounce ratio to emphasise that you’re calculating for a worst-case scenario, where a pack of wolves (more politely known as creditors) has pounced on the business and is demanding quick payment of the business’s liabilities. But don’t panic. Short-term creditors don’t have the right to demand immediate payment, except under unusual circumstances. This is a very conservative way to look at a business’s capability to pay its short-term liabilities - too conservative in most cases.

Keeping track of stock and debtor levels

Two other areas that effect liquidity need to be monitored carefully: how fast your stock is selling out (if your business requires holding goods for sale), and how fast your customers are paying up.

Here’s the ratio for stock levels:

· Stock turnover = Cost of goods sold ÷ Stock

Stock turnover tells you something about how liquid your stocks really are. This ratio divides the cost of goods sold, as shown in your yearly Profit and Loss statement, by the average value of your stock. If you don’t know the average, you can estimate it by using the stock figure listed in the Balance Sheet at the end of the year.

For the business represented in Figures 2-1 and 2-2, the stock turnover is £31,200 ÷ £7,800, or 4.0. This ratio means that this business turns over its stock four times each year. Expressed in days, the business carries a 91.25-day (365 ÷ 4.0) supply of stock.

Is a 90-day plus inventory good or bad? It depends on the industry and even on the time of year. A car dealer who has a 90-day supply of cars at the height of the season may be in a strong stock position, but the same stock position at the end of the season could be a real weakness. As Just In Time (JIT) supply chains and improved information systems make business operations more efficient across all industries, stock turnover is on the rise, and the average number of days that stock of any kind hangs around continues to shrink.

What about debtor levels?

· Debtor turnover = Sales on credit ÷ Debtors

Debtor turnover tells you something about liquidity by dividing the sales that you make on credit by the average debtors. If an average isn’t available, you can use the debtors from a Balance Sheet.

If the business represented in Figures 2-1 and 2-2 makes 80 per cent of its sales on credit, its debtor turnover is (£52,000 multiplied by 0.8) divided by £5,000, or 8.3. In other words, the company turns over its debtors 8.3 times per year, or once every 44 days, on average. That’s not too bad: payment terms are 30 days. But remember, unlike fine wine, debtors don’t improve with age.

Return on assets (ROA) ratio

One factor affecting the bottom-line profit of a business is whether it used debt to its advantage. For the year, a business may have realised a financial leverage gain - it earned more profit on the money it borrowed than the interest paid for the use of that borrowed money. So a good part of its net profit for the year may be due to financial leverage. The first step in determining financial leverage gain is to calculate a business’s return on assets (ROA) ratio, which is the ratio of EBIT (earnings before interest and tax) to the total capital invested in operating assets.

Here’s how to calculate ROA:

· EBIT ÷ Net operating assets = ROA

Note: This equation calls for net operating assets, which equals total assets less the non-interest-bearing operating liabilities of the business. Actually, many stock analysts and investors use the total assets figure because deducting all the non-interest-bearing operating liabilities from total assets to determine net operating assets is, quite frankly, a nuisance. But we strongly recommend using net operating assets because that’s the total amount of capital raised from debt and equity.

Compare ROA with the interest rate: if a business’s ROA is 14 per cent and the interest rate on its debt is 8 per cent, for example, the business’s net gain on its debt capital is 6 per cent more than what it’s paying in interest. There’s a favourable spread of 6 points (one point = 1 per cent), which can be multiplied by the total debt of the business to determine how much its total earnings before income tax is traceable to financial leverage gain.

In Figure 2-2, notice that the company has £10 million total interest-bearing debt (£4 million short-term plus £6 million long-term). Its total owners’ equity is £15.9 million. So its net operating assets total is £25.9 million (which excludes the three short-term non-interest-bearing operating liabilities). The company’s ROA, therefore, is

· £3.55 million earnings before interest and tax ÷ £25.9 million net operating assets = 13.71% ROA

The business earned £1,371,000 (rounded) on its total debt - 13.71 per cent ROA times £10 million total debt. The business paid only £750,000 interest on its debt. So the business had £621,000 financial leverage gain before income tax (£1,371,000 less £750,000). Put another way, the business paid 7.5 per cent interest on its debt but earned 13.71 per cent on this money for a favourable spread of 6.21 points - which, when multiplied by the £10 million debt, yields the £621,000 pre-tax financial gain for the year.

ROA is a useful earnings ratio, aside from determining financial leverage gain (or loss) for the period. ROA is a capital utilisation test - how much profit before interest and tax was earned on the total capital employed by the business. The basic idea is that it takes money (assets) to make money (profit); the final test is how much profit was made on the assets. If, for example, a business earns £1 million EBIT on £20 million assets, its ROA is only 5 per cent. Such a low ROA signals that the business is making poor use of its assets and will have to improve its ROA or face serious problems in the future.

Using combined ratios

You wouldn’t use a single ratio to decide whether one vehicle was a better or worse buy than another. Miles per Gallon (MPG), Miles per hour (MPH), annual depreciation percentage and residual value proportion are just a handful of the ratios that you’d want to review. So it is with a business. You can use a combination of ratios to form an opinion on the financial state of affairs at any one time.

The best known of these combination ratios is the Altman Z-Score (www.creditguru.com/CalcAltZ.shtml) that uses a combined set of five financial ratios derived from eight variables from a company’s financial statements linked to some statistical techniques to predict a company’s probability of failure. Entering the figures into the onscreen template at this website produces a score and an explanatory narrative giving a view on the businesses financial strengths and weaknesses.

Appreciating the limits of ratios

A danger with ratios is to believe that because you have a precise number, you have a right figure to aim for. For example, a natural feeling with financial ratios is to think that high figures are good ones, and an upward trend represents the right direction. This theory is, to some extent, encouraged by the personal feeling of wealth that having a lot of cash engenders.

Unfortunately, no general rule exists on which way is right for financial ratios. In some cases a high figure is good; in others, a low figure is best. Indeed, in some circumstances, ratios of the same value aren’t as good as each other. Look at the two working capital statements in Table 2-1.

Table 2-1 Difficult Comparisons

|

1 |

2 |

|||

|

Current Assets |

||||

|

Stock |

10,000 |

22,990 |

||

|

Debtors |

13,000 |

100 |

||

|

Cash |

100 |

23,100 |

10 |

23,100 |

|

Less Current Liabilities |

||||

|

Overdraft |

5,000 |

90 |

||

|

Creditors |

1,690 |

6,690 |

6,690 |

6,690 |

|

Working Capital |

16,410 |

16,410 |

||

|

Current Ratio |

3.4:1 |

3.4:1 |

The amount of working capital in examples 1 and 2 is the same, £16,410, as are the current assets and current liabilities, at £23,100 and £6,690 respectively. It follows that any ratio using these factors would also be the same. For example, the current ratios in these two examples are both identical, 3.4:1, but in the first case there’s a reasonable chance that some cash will come in from debtors, certainly enough to meet the modest creditor position. In the second example there’s no possibility of useful amounts of cash coming in from trading, with debtors at only £100, while creditors at the relatively substantial figure of £6,600 will pose a real threat to financial stability.

So in this case the current ratios are identical, but the situations being compared are not. In fact, as a general rule, a higher working capital ratio is regarded as a move in the wrong direction. The more money a business has tied up in working capital, the more difficult it is to make a satisfactory return on capital employed, simply because the larger the denominator, the lower the return on capital employed.

In some cases the right direction is more obvious. A high return on capital employed is usually better than a low one, but even this situation can be a danger signal, warning that higher risks are being taken. And not all high profit ratios are good: sometimes a higher profit margin can lead to reduced sales volume and so lead to a lower return on capital employed (ROCE).

In general, business performance as measured by ratios is best thought of as lying within a range; liquidity (current ratio), for example, staying between 1.2:1 and 1.8:1. A change in either direction may represent a cause for concern.

The temptation to compute cash flow per share: Don’t give in!

Businesses are prohibited from reporting a cash flow per share number on their financial reports. The accounting rule book specifically prohibits very few things, and cash flow per share is on this small list of contraband. Why? Because - and this is somewhat speculative on our part - the powers that be were worried that the cash flow number would usurp net profit as the main measure for profit performance. Indeed, many writers in the financial press were talking up the importance of cash flow from profit, so we see the concern on this matter. Knowing how important EPS is for market value of stocks, the authorities declared a similar per share amount for cash flow out of bounds and prohibited it from being included in a financial report. Of course, you could compute it quite easily - the rule doesn’t apply to how financial statements are interpreted, only to how they’re reported.

Should we dare give you an example of cash flow per share? Here goes: a business with £42 million cash flow from profit and 4.2 million total capital stock shares would end up with £10 cash flow per share. Shhh. One final sidebar, and you can call it quits — okay?

The Biz/ed (www.bized.co.uk/compfact/ratios/index.htm) website contains free tools that calculate financial ratios from company accounts. It also provide useful introductions to ratio analysis and definitions of each ratio and the formula used to calculate it.

By registering (for free) with the ProShare website (go to www.proshareclubs.co.uk and click on ‘Research Centre’ and ‘Performance Tables’), you have access to a number of tools that crunch public company ratios for you. Select the companies you want to look at, and then the ratios you’re most interested in (EPS, P/E, ROI, Dividend Yield and so on). All is revealed within a couple of seconds. You can then rank the companies by performance in more or less any way you want. You can find more comprehensive tools on the Internet, on the websites of share traders for example, but ProShare is a great site to cut your teeth on - and the price is right!

Frolicking through the Footnotes

Reading the footnotes in annual financial reports is no picnic. The investment pros have to read them, because in providing consultation to their clients they’re required to comply with due diligence standards, or because of their legal duties and responsibilities of managing other peoples’ money.

We suggest you do a quick read-through of the footnotes and identify the ones that seem to have the most significance. Generally, the most important footnotes are those dealing with the following matters:

· Share options awarded by the business to its executives: The additional shares issued under share options dilute (thin out) the earnings per share of the business, which in turn puts downside pressure on the market value of its shares, everything else being the same.

· Pending legal actions, litigation and investigations by government agencies: These intrusions into the normal affairs of the business can have enormous consequences.

· Segment information for the business: Most public businesses have to report information for the major segments of the organisation - sales and operating profit by territories or product lines. This gives a better glimpse of the different parts making up the whole business. (However, segment information may be reported elsewhere in an annual financial report than in the footnotes.)

These are just three of the many important pieces of information you should look for in footnotes. But you have to stay alert for other critical matters that a business may disclose in its footnotes - scan each and every footnote for potentially important information. You may find a footnote that discusses a major lawsuit against the business, for example, that makes the shares too risky for your portfolio.

Checking for Ominous Skies on the Audit Report

The value of analysing a financial report depends directly and entirely on the accuracy of the report’s numbers. Top management wants to present the best possible picture of the business in its financial report (which is understandable, of course). The managers have a vested interest in the profit performance and financial condition of the business.

Independent auditors are like umpires in the financial reporting process. The auditor comes in, does an audit of the business’s accounting system and procedures, and gives a report that’s attached to the company’s financial statements. You should check the audit report included with the financial report. Publicly owned businesses are required to have their annual financial reports audited by an independent accountancy firm, and many privately owned businesses have audits done too because they know that an audit report adds credibility to the financial report.

What if a private business’s financial report doesn’t include an audit report? Well, you have to trust that the business prepared accurate financial statements that follow generally accepted accounting principles and that the footnotes to the financial statements provide adequate disclosure.

Unfortunately, the audit report gets short shrift in financial statement analysis, maybe because it’s so full of technical terminology and accountant doublespeak. But even though audit reports are a tough read, anyone who reads and analyses financial reports should definitely read the audit report. Book VI, Chapter 3 provides a lot more information on audits and the auditor’s report.

The auditor judges whether the business used accounting methods and procedures in accordance with accepted accounting principles. In most cases, the auditor’s report confirms that everything is hunky-dory, and you can rely on the financial report. However, sometimes an auditor waves a yellow flag - and in extreme cases, a red flag. Here are the two most important warnings to watch out for in an audit report:

· The business’s capability to continue normal operations is in doubt because of what are known as financial exigencies, which may mean a low cash balance, unpaid overdue liabilities or major lawsuits that the business doesn’t have the cash to cover.

· One or more of the methods used in the report isn’t in line with the prevailing accounting body rules, leading the auditor to conclude that the numbers reported are misleading or that disclosure is inadequate.

Although auditor warnings don’t necessarily mean that a business is going down the tubes, they should turn on that light bulb in your head and make you more cautious and sceptical about the financial report. The auditor is questioning the very information on which the business’s value is based, and you can’t take that kind of thing lightly.

In very small businesses it’s likely that the accounts won’t be independently audited and their accounts come with a rather alarming caveat, running something like this: These accounts have been prepared on the basis of information provided by the owners and have not been independently verified. A full audit is an expensive process and few businesses that don’t have to will go to the expense and trouble just to be told what they probably already know anyway.

Just because a business has a clean audit report doesn’t mean that the financial report is completely accurate and above board. As discussed in Book VI, Chapter 3, auditors don’t necessarily catch everything. Keep in mind that the accounting rules are pretty flexible, leaving a company’s accountants with room for interpretation and creativity that’s just short of cooking the books (deliberately defrauding and misleading readers of the financial report). Window dressing and profit smoothing - two common examples of massaging the numbers - are explained in Book VI, Chapter 1.

Finding Financial Facts

Understanding how to calculate financial ratios and how to interpret that data is all fine and dandy, but before you can do anything useful you need to get a copy of the accounts in the first place. Seeing the accounts for your own business shouldn’t be too much of a problem. If you’re the boss, the accounts should be on your desk right now; if you’re not the boss, try snuggling up to the accounts department. If they’re too coy to let you have today’s figures, the latest audited accounts are in the public domain anyway filed away at Companies House (www.companieshouse.gov.uk), as required by law.

Public company accounts

Most companies make their glossy annual financial reports available to download from their websites, which you can find by typing the company name into an Internet search engine. You need to have Adobe Acrobat Reader on your computer to open the files. No problem, though: Adobe Acrobat Reader is free and you can easily download the program from Adobe’s website (http://get.adobe.com/uk/reader).

Yahoo has direct online links to several thousand public company reports and accounts and performance ratios at http://uk.finance.yahoo.com . (Enter the name of the company you’re looking for in the box on the left of the screen under Investing. It appears after you’ve entered about three letters; click and follow the threads). Paying this site a visit saves you the time and trouble of hunting down company websites.

Private company accounts

Finding financial information on private companies is often a time-consuming and frustrating job. Not for nothing do these companies call themselves ‘private’. Businesses, and particularly smaller businesses, can be very secretive about their finances and have plenty of tricks to hide information from prying eyes. Many smaller businesses can elect to file abbreviated accounts with Companies House that provide only the barest details. The accounts of very small companies don’t need to be audited, so the objective reliability of the scant data given may be questionable. Having said that, tens of thousands of private companies file full and generally reliable accounts.

Two fruitful sources of private company accounts exist:

· Companies House (www.companieshouse.gov.uk) is the official repository of all company information in the UK. Its WebCHeck service offers a free Company Names and Address Index that covers 2 million companies, searchable either by company name or by company registration numbers. You can use WebCHeck to purchase (at a cost of £1 per document) a company’s latest accounts that give details of sales, profits, margins, directors, shareholders and bank borrowings.

· Keynote (www.keynote.co.uk) offers business ratios and trends for 140 industry sectors and provides information to assess accurately the financial health of each industry sector. This service enables you to find out how profitable a business sector is and how successful the main companies operating in each sector are. Executive summaries are free, but expect to pay between £400 and £600 for most reports.

Scoring credit

If all you want is a quick handle on whether a company is likely to be around long enough to pay its bills, including a dividend to shareholders, then a whole heap of information exists about credit status for both individual sole traders and companies of varying complexity. Expect to pay anywhere from £5 for basic information up to £200 for a very comprehensive picture of a company’s credit status, so you can avoid trading unknowingly with individuals or businesses that pose a credit risk.

Experian (www.ukexperian.com), Dun & Bradstreet (www.dnb.com), Creditgate.com (www.creditgate.com) and Credit Reporting (www.creditreporting.co.uk) are the major agencies compiling and selling credit histories and small-business information. Between them they offer a comprehensive range of credit reports instantly available online that include advice about credit limits.

Using FAME (Financial Analysis Made Easy)

FAME (Financial Analysis Made Easy) is a powerful database that contains information on 7 million companies in the UK and Ireland. Typically, the following information is included: contact information including phone, email and web addresses plus main and other trading addresses; activity details; 29 Profit and Loss statement and 63 Balance Sheet items; cash flow and ratios; credit score and rating; security and price information (listed companies only); names of bankers, auditors, previous auditors and advisers; details of holdings and subsidiaries (including foreign holdings and subsidiaries); names of current and previous directors with home addresses and shareholder indicator; heads of department; and shareholders. You can compare each company with detailed financials with its peer group based on its activity codes and the software lets you search for companies that comply with your own criteria, combining as many conditions as you like. FAME is available in business libraries and on CD from the publishers, who also offer a free trial (www.bvdinfo.com/Products/Company-Information/National/FAME.aspx).

Looking beyond financial statements

Investors can’t rely solely on the financial report when making investment decisions. Analysing a business’s financial statements is just one part of the process. You may need to consider these additional factors, depending on the business you’re thinking about investing in:

· Industry trends and problems

· National economic and political developments

· Possible mergers, friendly acquisitions and hostile takeovers

· Turnover of key executives

· International markets and currency exchange ratios

· Supply shortages

· Product surpluses

Whew! This kind of stuff goes way beyond accounting, obviously, and is just as significant as financial statement analysis when you’re picking stocks and managing investment portfolios. A good book for new investors to read is Investing For Dummies by Tony Levene (John Wiley & Sons).

Have a Go

Use the following Profit and Loss statement and Balance Sheet for Company A to answer the questions in this Have a Go section.

|

Company A Ltd. |

||

|

Profit and Loss Account |

£000s |

|

|

Sales revenue |

110,000 |

|

|

Cost of goods sold |

(62,400) |

|

|

Gross margin |

47,600 |

|

|

Sales, admin and general expenses |

31,200 |

|

|

Depreciation expense |

3,300 |

|

|

Earnings before interest and tax |

13,100 |

|

|

Interest expenses |

1,500 |

|

|

Earnings before tax |

11,600 |

|

|

Corporation tax payable |

1,800 |

|

|

Net profit |

9,800 |

|

|

Earnings per share £6.16 (9,800,000 ÷ 1,590,000 shares) |

||

|

Balance Sheet |

£000s |

|

|

Fixed Assets |

39,000 |

|

|

Accumulated depreciation |

13,650 |

25,350 |

|

Current Assets |

||

|

Stock |

15,600 |

|

|

Debtors |

10,000 |

|

|

Cash |

7,000 |

|

|

Prepaid expenses |

1,500 |

|

|

£34,400 |

||

|

Current Liabilities |

||

|

Creditors |

3,000 |

|

|

Accrued expenses |

4,800 |

|

|

Tax payable |

150 |

|

|

Overdraft |

8,000 |

|

|

15,950 |

||

|

Net current assets |

18,450 |

|

|

Total assets less current liabilities |

43,800 |

|

|

Long-term liabilities |

12,000 |

|

|

31,800 |

||

|

Capital |

||

|

Share capital |

8,000 |

|

|

Retained earnings |

23,800 |

|

|

31,800 |

1. Calculate the gross profit margin for Company A.

2. Calculate the net profit ratio for Company A.

3. What is the earnings per share (EPS)?

4. What is the price earnings ratio (P/E ratio), given that the market value of the shares is £21?

5. Suppose the stock of a public company is selling at £50 and it offers cash dividends per share of 75p. What is the dividend yield?

6. Calculate the return on equity for Company A.

7. Calculate the current ratio for Company A.

8. Calculate the acid ratio for Company A.

9. Calculate the stock turnover for Company A.

10. Calculate the debtors turnover for Company A. Assume that 80 per cent of sales are on credit.

Answering the Have a Go Questions

1. You calculate the gross profit margin as follows:

· Gross margin ÷ Sales revenue × 100

· = 47,600 ÷ 110,000 × 100

· = 43.27%

2. You calculate the net profit ratio as follows:

· Net Profit ÷ Sales Revenue × 100

· = 9,800 ÷ 110,000 × 100

· = 8.91%

3. You calculate the earnings per share as follows:

· Net profit ÷ Total number of shares

· = 9,800,000 ÷ 1,590,000

· = £6.16

4. You calculate the P/E ratio as follows:

· Market value of share ÷ EPS

· = 21 ÷ 6.16

· = £3.41

5. You calculate the dividend yield as follows:

· Annual cash dividend ÷ Current market price per share

· = 75p ÷ 50

· = 1.5%

6. You calculate return on equity as follows:

· Net profit ÷ Owners equity

· = 9,800 ÷ 31,800

· = 30.8%

7. You calculate the current ratio as follows:

· Current assets ÷ Current liabilities

· = 34,400 ÷ 15,950

· = 2.156

Businesses are expected to have a current ratio of approximately 2:1, so this is fine.

8. You calculate the acid ratio as follows:

· Cash + Debtors ÷ Current liabilities

· = 17,000 (7,000 + 10,000) ÷ 15,950

· = 1.06

The company would be able to pay off its short-term liabilities, so this result is fine.

9. You calculate the stock turnover as follows:

· Cost of goods sold ÷ stock

· = 62,400 ÷ 15,600

· = 4

This means that the business is turning over its stock four times a year. Expressed in days, you’d say that the business carries 91.25 days’ worth of stock (365 ÷ 4).

10. You calculate the debtors turnover as follows:

· Sales on credit ÷ Debtors

· = 88,000 (110,000 × 0.8) ÷ 10,000

· = 8.8

This means that the company turns over its debt 8.8 times a year, or once every 41 days (365 ÷ 8.8).