Bookkeeping & Accounting All-in-One For Dummies (2015)

Book VI

Accountants: Working with the Outside World

Head online and visit www.dummies.com/extras/bookkeepingaccountingaio for some free bonus articles.

Head online and visit www.dummies.com/extras/bookkeepingaccountingaio for some free bonus articles.

In this book …

· Know how an accountant would prepare the accounts for a larger business.

· Think like an investor: see how an investor reads the accounts of a business and uses ratios.

· Work with auditors and know what they actually do.

Chapter 1

Getting a Financial Report Ready for Prime Time

In This Chapter

![]() Making sure that all the pieces fit together

Making sure that all the pieces fit together

![]() Looking at the various changes in owners’ equity

Looking at the various changes in owners’ equity

![]() Making sure that disclosure is adequate

Making sure that disclosure is adequate

![]() Touching up the numbers

Touching up the numbers

![]() Financial reporting on the Internet

Financial reporting on the Internet

![]() Dealing with financial reports’ information overload

Dealing with financial reports’ information overload

The primary financial statements of a business are:

· Profit and Loss statement: Summarises sales revenue inflows and expense outflows for the period and ends with the bottom-line profit, which is the net inflow for the period (a loss is a net outflow).

· Balance Sheet: Summarises the financial condition at the end of the period, consisting of amounts for assets, liabilities and owners’ equity at that instant in time.

· Cash flow statement: Summarises the net cash inflow (or outflow) from profit for the period plus the other sources and uses of cash during the period.

An annual financial report of a business contains more than just these three financial statements. The business manager plays an important role - which outside investors and lenders should understand. The manager should do certain critical things before the financial report is released to the outside world.

1. The manager should review with a critical eye the vital connections between the items reported in all three financial statements. All amounts have to fit together like the pieces of a jigsaw. The net cash increase (or decrease) reported at the end of the cash flow statement, for instance, has to tie in with the change in cash reported in the Balance Sheet. Abnormally high or low ratios between connected accounts should be scrutinised carefully.

2. The manager should carefully review the disclosures in the financial report (all information in addition to the financial statements) to make sure that disclosure is adequate according to financial reporting standards, and that all the disclosure elements are truthful but not damaging to the interests of the business.

This disclosure review can be compared with the notion of due diligence, which is done to make certain that all relevant information is collected, that the information is accurate and reliable, and that all relevant requirements and regulations are being complied with. This step is especially important for public corporations whose securities (shares and debt instruments) are traded on national securities exchanges.

This disclosure review can be compared with the notion of due diligence, which is done to make certain that all relevant information is collected, that the information is accurate and reliable, and that all relevant requirements and regulations are being complied with. This step is especially important for public corporations whose securities (shares and debt instruments) are traded on national securities exchanges.

3. The manager should consider whether the financial statement numbers need touching up to smooth the jagged edges off the company’s year-to-year profit gyrations or to improve the business’s short-term solvency picture. Although this can be described as putting your thumb on the scale, you can also argue that sometimes the scale is a little out of balance to begin with and the manager is adjusting the financial statements to jibe better with the normal circumstances of the business.

In discussing the third step later in the chapter, we walk on thin ice. Some topics are, shall we say, rather delicate. The manager has to strike a balance between the interests of the business on the one hand and the interests of the owners (investors) and creditors of the business on the other. The best analogy we can think of is the advertising done by a business. Advertising should be truthful but, as we’re sure you know, businesses have a lot of leeway in how to advertise their products and they have been known to engage in hyperbole. Managers exercise the same freedom in putting together their financial reports.

In discussing the third step later in the chapter, we walk on thin ice. Some topics are, shall we say, rather delicate. The manager has to strike a balance between the interests of the business on the one hand and the interests of the owners (investors) and creditors of the business on the other. The best analogy we can think of is the advertising done by a business. Advertising should be truthful but, as we’re sure you know, businesses have a lot of leeway in how to advertise their products and they have been known to engage in hyperbole. Managers exercise the same freedom in putting together their financial reports.

Reviewing Vital Connections

Business managers and investors read financial reports because these reports provide information regarding how the business is doing. When reviewing the annual financial report before releasing it outside the business, the top managers of the business should keep in mind that a financial report is designed to answer certain basic financial questions:

Business managers and investors read financial reports because these reports provide information regarding how the business is doing. When reviewing the annual financial report before releasing it outside the business, the top managers of the business should keep in mind that a financial report is designed to answer certain basic financial questions:

· Is the business making a profit or suffering a loss, and how much?

· How do assets stack up against liabilities?

· Where did the business get its capital and is it making good use of the money?

· Is profit generating cash flow?

· Did the business reinvest all its profit or distribute some of the profit to owners?

· Does the business have enough capital for future growth?

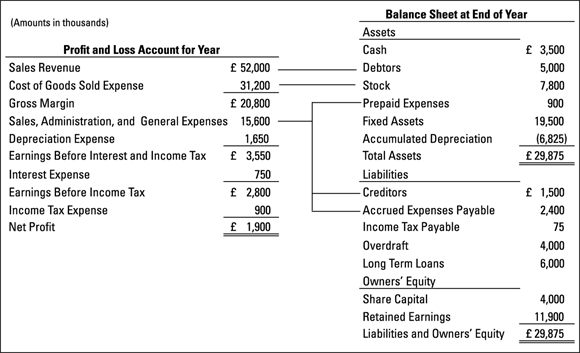

As a hypothetical but realistic business example, Figure 1-1 highlights some of the vital connections - the lines connect one or more Balance Sheet accounts with sales revenue or an expense in the Profit and Loss statement. The savvy manager or investor checks these links to see whether everything is in order or whether some danger signals point to problems. (We should make clear that these lines of connection don’t appear in actual financial reports.)

As a hypothetical but realistic business example, Figure 1-1 highlights some of the vital connections - the lines connect one or more Balance Sheet accounts with sales revenue or an expense in the Profit and Loss statement. The savvy manager or investor checks these links to see whether everything is in order or whether some danger signals point to problems. (We should make clear that these lines of connection don’t appear in actual financial reports.)

Figure 1-1: Vital connections between the Profit and Loss statement and the Balance Sheet.

In the following list, we briefly explain these five connections, mainly from the manager’s point of view. Book VI, Chapter 2 explains how investors might read a financial report and compute certain ratios. (Investors are on the outside looking in; managers are on the inside looking out.)

Note: We cut right to the chase in the following brief comments and we don’t illustrate the calculations behind the comments. The purpose here is to emphasise why managers should pay attention to these important ratios.

1. Sales Revenue and Debtors: This business’s ending balance of debtors is five weeks of its annual sales revenue. The manager should compare this ratio to the normal credit terms offered to the business’s customers. If the ending balance is too high, the manager should identify which customers’ accounts are past due and take actions to collect these amounts, or perhaps shut off future credit to these customers. An abnormally high balance of debtors may signal that some of these customers’ amounts owed to the business should be written off as uncollectable bad debts.

2. Cost of Goods Sold Expense and Stock: This business’s ending stock is 13 weeks of its annual cost of goods sold expense. The manager should compare this ratio to the company’s stock policies and objectives regarding how long stock should be held awaiting sale. If stock is too large the manager should identify which products have been in stock too long; further purchases (or manufacturing) should be curtailed. Also, the manager may want to consider sales promotions or cutting sales prices to move these products out of stock faster.

3. Sales, Administration and General (SA&G) Expenses and Prepaid Expenses: This business’s ending balance of prepaid expenses is three weeks of the total of these annual operating expenses. The manager should know what the normal ratio of prepaid expenses should be relative to the annual SA&G operating expenses (excluding depreciation expense). If the ending balance is too high, the manager should investigate which costs have been paid too far in advance and take action to bring these prepaids back down to normal.

4. Sales, Administration and General (SA&G) Expenses and Creditors: This business’s ending balance of creditors is five weeks of its annual operating expenses. Delaying payment of these liabilities is good from the cash flow point of view (refer to Book IV, Chapter 3) but delaying too long may jeopardise the company’s good credit rating with its key suppliers and vendors. If this ratio is too high, the manager should pinpoint which specific liabilities haven’t been paid and whether any of these are overdue and should be paid immediately. Or, the high balance may indicate that the company is in a difficult short-term solvency situation and needs to raise more money to pay the amounts owed to suppliers and vendors.

5. Sales, Administration and General (SA&G) Expenses and Accrued Expenses Payable: This business’s ending balance of this operating liability is eight weeks of the business’s annual operating expenses. This ratio may be consistent with past experience and the normal lag before paying these costs. On the other hand, the ending balance may be abnormally high. The manager should identify which of these unpaid costs are higher than they should be. As with creditors, inflated amounts of accrued liabilities may signal serious short-term solvency problems.

These five key connections are very important ones, but the manager should scan all basic connections to see whether the ratios pass the common sense test. For example, the manager should make a quick eyeball test of interest expense compared with interest-bearing debt. In Figure 1-1, interest expense is £750,000 compared with £10 million total debt, which indicates a 7.5 per cent interest rate. This seems okay. But if the interest expense were more than £1 million, the manager should investigate and determine why it’s so high.

There’s always the chance of errors in the accounts of a business. Reviewing the vital connections between the Profit and Loss statement items and the Balance Sheet items is a very valuable final check before the financial statements are approved for inclusion in the business’s financial report. After the financial report is released to the outside world, it becomes the latest chapter in the official financial history of the business. If the financial statements are wrong, the business and its top managers are responsible.

Statement of Changes in Owners’ Equity and Comprehensive Income

In many situations a business needs to prepare one additional financial statement - the statement of changes in owners’ equity. Owners’ equity consists of two fundamentally different sources - capital invested in the business by the owners, and profit earned by and retained in the business. The specific accounts maintained by the business for its total owners’ equity depend on the legal organisation of the business entity. One of the main types of legal organisation of business is the company, and its owners are shareholders because the company issues ownership shares representing portions of the business. So, the title statement of changes in shareholders’ equity is used for companies. (Book V, Chapter 1 explains the corporation and other legal types of business entities.)

In many situations a business needs to prepare one additional financial statement - the statement of changes in owners’ equity. Owners’ equity consists of two fundamentally different sources - capital invested in the business by the owners, and profit earned by and retained in the business. The specific accounts maintained by the business for its total owners’ equity depend on the legal organisation of the business entity. One of the main types of legal organisation of business is the company, and its owners are shareholders because the company issues ownership shares representing portions of the business. So, the title statement of changes in shareholders’ equity is used for companies. (Book V, Chapter 1 explains the corporation and other legal types of business entities.)

First, consider the situation in which a business does not need to report this statement - to make clearer why the statement is needed. Suppose a company has only one class of share and it didn’t buy any of its own shares during the year and it didn’t record any gains or losses in owners’ equity during the year due to other comprehensive income (explained later in this section). This business doesn’t need a statement of changes in shareholders’ equity. In reading the financial report of this business you’d see in its cash flow statement whether the business raised additional capital from its owners during the year and how much in cash dividends (distributions from profit) was paid to the owners during the year. The cash flow statement contains all the changes in the owners’ equity accounts during the year.

In sharp contrast, larger businesses - especially publicly traded corporations - generally have complex ownership structures consisting of two or more classes of shares; they usually buy some of their own shares and they have one or more technical types of gains or losses during the year. So, they prepare a statement of changes in stockholders’ equity to collect together in one place all the changes affecting the owners’ equity accounts during the year. This particular ‘mini’ statement (that focuses narrowly on changes in owners’ equity accounts) is where you find certain gains and losses that increase or decrease owners’ equity but that are not reported in the Profit and Loss statement. Basically, a business has the option to bypass the Profit and Loss statement and, instead, report these gains and losses in the statement of changes in owners’ equity. In this way the gains or losses don’t affect the bottom-line profit of the business reported in its Profit and Loss statement. You have to read this financial summary of the changes in the owners’ equity accounts to find out whether the business had any of these gains or losses and the amounts of the gains or losses.

The special types of gains and losses that can be reported in the statement of owners’ equity (instead of the Profit and Loss statement) have to do with foreign currency translations, unrealised gains and losses from certain types of securities investments by the business, and changes in liabilities for unfunded pension fund obligations of the business. Comprehensive income is the term used to describe the normal content of the Profit and Loss statement plus the additional layer of these special types of gains and losses. Being so technical in nature, these gains and losses fall in a ‘twilight zone’, as it were, in financial reporting. The gains and losses can be tacked on at the bottom of the Profit and Loss statement or they can be put in the statement of changes in owners’ equity - it’s up to the business to make the choice. If you encounter these gains and losses in reading a financial report, you’ll have to study the footnotes to the financial statements to learn more information about each gain and loss.

The special types of gains and losses that can be reported in the statement of owners’ equity (instead of the Profit and Loss statement) have to do with foreign currency translations, unrealised gains and losses from certain types of securities investments by the business, and changes in liabilities for unfunded pension fund obligations of the business. Comprehensive income is the term used to describe the normal content of the Profit and Loss statement plus the additional layer of these special types of gains and losses. Being so technical in nature, these gains and losses fall in a ‘twilight zone’, as it were, in financial reporting. The gains and losses can be tacked on at the bottom of the Profit and Loss statement or they can be put in the statement of changes in owners’ equity - it’s up to the business to make the choice. If you encounter these gains and losses in reading a financial report, you’ll have to study the footnotes to the financial statements to learn more information about each gain and loss.

Keep on the lookout for the special types of gains and losses that are reported in the statement of changes in owners’ equity. A business has the option to tack such gains and losses onto the bottom of its Profit and Loss statement - below the net income line. But most businesses put these income gains and losses in their statement of changes in shareholders’ equity, or in a note or notes to their accounts. So watch out for any large amounts of gains or losses that are reported in the statement of changes in owners’ equity.

The general format of the statement of changes in shareholders’ equity includes a column for each class of stock (ordinary shares, preference shares and so on); a column for any shares of its own that the business has purchased and not cancelled; a column for retained earnings; and one or more columns for any other separate components of the business’s owners’ equity. Each column starts with the beginning balance and then shows the increases or decreases in the account during the year. For example, a comprehensive gain is shown as an increase in retained earnings and a comprehensive loss as a decrease. The purchase of its own shares is shown as an increase in the relevant column, and if the business reissued some of these shares (such as for stock options exercised by executives), the cost of these shares reissued is shown as a decrease in the column.

We have to admit that reading the statement of changes, or notes to the accounts, in shareholders’ equity can be heavy going. The professionals - stock analysts, money and investment managers and so on - carefully read through and dissect this statement, or at least they should. The average non-professional investor should focus on whether the business had a major increase or decrease in the number of shares during the year, whether the business changed its ownership structure by creating or eliminating a class of stock, and the impact of stock options awarded to managers of the business.

Making Sure that Disclosure Is Adequate

The primary financial statements (including the statement of changes in owners’ equity, if reported) are the backbone of a financial report. In fact, a financial report isn’t deserving of the name if the primary financial statements aren’t included. But, as mentioned earlier, there’s much more to a financial report than the financial statements. A financial report needs disclosures. Of course, the financial statements provide disclosure of the most important financial information about the business. The term disclosures, however, usually refers to additional information provided in a financial report. In a nutshell, a financial report has two basic parts: (1) the primary financial statements and (2) disclosures.

The chief officer of the business (usually the CEO of a publicly owned company, the president of a private corporation or the managing partner of a partnership) has the primary responsibility to make sure that the financial statements have been prepared according to prevailing accounting standards and that the financial report provides adequate disclosure. He works with the chief financial officer of the business to make sure that the financial report meets the standard of adequate disclosure. (Many smaller businesses hire an independent, qualified accountant to advise them on their financial statements and other disclosures in their financial reports.)

Types of disclosures in financial reports

For a quick survey of disclosures in financial reports - that is to say, the disclosures in addition to the financial statements - the following distinctions are helpful:

· Footnotes provide additional information about the basic figures included in the financial statements. Virtually all financial statements need footnotes to provide additional information for the account balances in the financial statements.

· Supplementary financial schedules and tables provide more details than can be included in the body of financial statements.

· A wide variety of other information may be included, some of which is required if the business is a company quoted on a stock market subject to government regulations regarding financial reporting to its shareholders and other information that’s voluntary and not strictly required legally or according to generally accepted accounting principles.

Footnotes: Nettlesome but needed

Footnotes appear at the end of the primary financial statements. Within the financial statements you see references to particular footnotes. And at the bottom of each financial statement, you find the following sentence (or words to this effect): ‘The footnotes are integral to the financial statements.’ You should read all footnotes for a full understanding of the financial statements.

Footnotes come in two types:

· One or more footnotes must be included to identify the major accounting policies and methods that the business uses. (Book V, Chapter 2 explains that a business must choose among alternative accounting methods for certain expenses, and for their corresponding operating assets and liabilities.) The business must reveal which accounting methods it uses for its major expenses. In particular, the business must identify its cost of goods sold expense (and stock) method and its depreciation methods.

· Other footnotes provide additional information and details for many assets and liabilities. Details about share option plans for key executives are the main type of footnote to the capital stock account in the owners’ equity section of the Balance Sheet.

One problem that most investors face when reading footnotes - and, for that matter, many managers who should understand their own footnotes but find them a little dense - is that footnotes often deal with complex issues (such as lawsuits) and rather technical accounting matters. Let us offer you one footnote that brings out this latter point. This footnote is taken from the recent financial report of a well-known manufacturer that uses a very conservative accounting method for determining its cost of goods sold expense and stock cost value. (Book V, Chapter 2 explains accounting methods.) We want you to read the following footnote from the 2011 Annual Report of this manufacturer and try to make sense of it (amounts are in thousands).

D. Inventories: Inventories are valued principally by the LIFO (last-in, first-out) method. If the FIFO (first-in, first-out) method had been in use, inventories would have been £2,000 million and £1,978 million higher than reported at December 31, 2010 and 2011, respectively.

Yes, these amounts are in millions of pounds. The company’s stock cost value at the end of 2010 would have been £2 billion higher if the FIFO method had been used. Of course, you have to have some idea of the difference between the two methods, which we explain in Book V, Chapter 2.

You may wonder how different the company’s annual profits would have been if the alternative method had been in use. A manager can ask the accounting department to do this analysis. But as an outside investor, you would have to compute these amounts. Businesses disclose which accounting methods they use but they don’t have to disclose how different annual profits would have been if the alternative method had been used - and very few do.

Other disclosures in financial reports

The following discussion includes a fairly comprehensive list of the various types of disclosures found in annual financial reports of larger, publicly owned businesses - in addition to footnotes. A few caveats are in order. First, not every public company includes every one of the following items, although the disclosures are fairly common. Second, the level of disclosure by private businesses - after you get beyond the financial statements and footnotes - is much less than in public companies. Third, tracking the actual disclosure practices of private businesses is difficult because their annual financial reports are circulated only to their owners and lenders. A private business may include any or all of the following disclosures, but by and large it’s not legally required to do so. The next section further explains the differences between private and public businesses regarding disclosure practices in their annual financial reports.

Warren Buffett’s annual letter to shareholders

We have to call your attention to one notable exception to the generally self-serving and slanted writing found in the letter to shareholders by the chief executive officer of the business in annual financial reports. The annual letter to stockholders of Berkshire Hathaway, Inc. is written by Warren Buffett, the chairman and CEO. Mr Buffett has become very well known - he’s called the ‘Oracle of Omaha’. In the annual ranking of the world’s richest people by Forbes magazine he’s near the top of the list - right behind people like Bill Gates, the co-founder of Microsoft. If you’d invested £1,000 with him in 1960, your investment would be worth well over £1 million today. Even in the recent financial meltdown Berkshire Hathaway stock delivered a return of nearly 80 per cent over the period 2000-2011 compared to a negative 12 per cent return for the S&P 500. Mr Buffett’s letters are the epitome of telling it like it is; they’re very frank and quite humorous.

You can go to the website of the company (www.berkshirehathaway.com) and download his most recent letter. You’ll learn a lot about his investing philosophy and the letters are a delight to read.

Public corporations typically include most of the following disclosures in their annual financial reports to their shareholders:

· Cover (or transmittal) letter): A letter from the chief executive of the business to the shareholders.

· Highlights table: A short table that presents the shareholder with a financial thumbnail sketch of the business.

· Management discussion and analysis (MD&A): Deals with the major developments and changes during the year that affected the financial performance and situation of the business.

· Segment information: The sales revenue and operating profits are reported for the major divisions of the organisation or for its different markets (international versus domestic, for example).

· Historical summaries: Financial history that extends back beyond the years (usually three but can be up to five or six) included in the primary financial statements.

· Graphics: Bar charts, trend charts and pie charts representing financial conditions; photos of key people and products.

· Promotional material: Information about the company, its products, its employees and its managers, often stressing an over-arching theme for the year.

· Profiles: Information about members of top management and the board of directors.

· Quarterly summaries of profit performance and share prices and dividends: Shows financial performance for all four quarters in the year and share price ranges for each quarter.

· Management’s responsibility statement: A short statement that management has primary responsibility for the accounting methods used to prepare the financial statements and for providing the other disclosures in the financial report.

· Independent auditor’s report: The report from the accounting firm that performed the audit, expressing an opinion on the fairness of the financial statements and accompanying disclosures. (Book VI, Chapter 3 discusses the nature of audits.) Public companies are required to have audits; private businesses may or may not have their annual financial reports audited, depending on their size.

· Company contact information: Information on how to contact the company, the website address of the company, how to get copies of the reports filed with the London Stock Exchange, the Securities Exchange Commission, the stock transfer agent and registrar of the company, and other information.

Managers of public corporations rely on lawyers, auditors and their financial and accounting officers to make sure that everything that should be disclosed in the business’s annual financial reports is included and that the exact wording of the disclosures isn’t misleading, inaccurate or incomplete. This is a tall order. The field of financial reporting disclosure changes constantly. Laws and authoritative accounting standards have to be observed. Inadequate disclosure in an annual financial report is just as serious as using wrong accounting methods for measuring profit and for determining values for assets, liabilities and owners’ equity. A financial report can be misleading because of improper accounting methods or because of inadequate or misleading disclosure. Both types of deficiencies can lead to nasty lawsuits against the business and its managers.

Companies House provides forms showing how the Companies Act requires Balance Sheets and Profit and Loss statements to be laid out. To access the guidance, go to www.companieshouse.gov.uk/forms/introduction.shtml . All the statutory forms are available on request and free of charge.

Keeping It Private versus Going Public

Compared with their big brothers and sisters, privately owned businesses provide very little additional disclosures in their annual financial reports. The primary financial statements and footnotes are pretty much all you get.

The annual financial reports of publicly owned corporations include all, or nearly all, of the disclosure items listed earlier. Somewhere in the range of 3,000 companies are publicly owned, and their shares are traded on the London Stock Exchange, NASDAQ or other stock exchanges. Publicly owned companies must file annual financial reports with the Stock Exchange, which is the agency that makes and enforces the rules for trading in securities and for the financial reporting requirements of publicly owned corporations. These filings are available to the public on the London Stock Exchange’s website (www.londonstockexchange.com) or for US companies on the SEC’s EDGAR database at the SEC’s website (www.sec.gov/edgar/searchedgar/cik.htm).

Both privately held and publicly owned businesses are bound by the same accounting rules for measuring profit, assets, liabilities and owners’ equity in annual financial reports to the owners of the business and in reports that are made available to others (such as the lenders to the business). There aren’t two different sets of accounting rules - one for private companies and another one for public businesses. The accounting measurement and valuation rules are the same for all businesses. However, disclosure requirements and practices differ greatly between private and public companies.

Publicly owned businesses live in a fish bowl. When a company goes public with an IPO (initial public offering of shares), it gives up a lot of the privacy that a closely held business enjoys. Publicly owned companies whose shares are traded on national stock exchanges live in glass houses. In contrast, privately owned businesses lock their doors regarding disclosure. Whenever a privately owned business releases a financial report to its bank in seeking a loan, or to the outside non-management investors in the business, it should include its three primary financial statements and footnotes. But beyond this, it has much more leeway and doesn’t have to include the additional disclosure items listed in the preceding section.

A private business may have its financial statements audited by a professional accounting firm. If so, the audit report is included in the business’s annual financial report. The very purpose of having an audit is to reassure shareholders and potential investors in the business that the financial statements can be trusted. But as we look up and down the preceding list of disclosure items we don’t see any other absolutely required disclosure item for a privately held business. The large majority of closely held businesses guard their financial information like Fort Knox.

The less information divulged in the annual financial report, the better - that’s the thinking of closely held businesses. And we don’t entirely disagree. The shareholders don’t have the liquidity for their shares that shareholders of publicly held corporations enjoy. The market prices of public companies are everything, so information is made publicly available so that market prices are fairly determined. The shares of privately owned businesses are rarely traded, so there’s not such an urgent need for a complete package of information.

A private company could provide all the disclosures given in the preceding list - there’s certainly no law against this. But usually they don’t. Investors in private businesses can request confidential reports from managers at the annual shareholders’ meetings, but doing so isn’t practical for a shareholder in a large public corporation.

Nudging the Numbers

This section discusses two accounting tricks that business managers and investors should know about. We don’t endorse either technique, but you should be aware of both of them. In some situations, the financial statement numbers don’t come out exactly the way the business wants. Accountants use certain tricks of the trade - some would say sleight-of-hand - to move the numbers closer to what the business prefers. One trick improves the appearance of the short-term solvency of the business, in particular the cash balance reported in the Balance Sheet at the end of the year. The other device shifts profit from one year to the next to make for a smoother trend of net income from year to year.

Not all businesses use these techniques, but the extent of their use is hard to pin down because no business would openly admit to using these manipulation methods. The evidence is fairly convincing, however, that many businesses use these techniques. We’re sure you’ve heard the term loopholes applied to income tax accounting. Well, some loopholes exist in financial statement accounting as well.

Fluffing up the cash balance by ‘window dressing’

Suppose you manage a business and your accountant has just submitted to you a preliminary, or first draft, of the year-end Balance Sheet for your review. Your preliminary Balance Sheet includes the following:

|

Preliminary Balances, Before Window Dressing |

|||

|

Cash |

£0 |

Creditors |

£235,000 |

|

Debtors |

£486,000 |

Accrued expenses payable |

£187,000 |

|

Stock |

£844,000 |

Income tax payable |

£58,000 |

|

Overdraft |

£200,000 |

||

|

Prepaid expenses |

£72,000 |

||

|

Current assets |

£1,402,000 |

Current liabilities |

£680,000 |

You start reading the numbers when something strikes you: a zero cash balance? How can that be? Maybe your business has been having some cash flow problems and you’ve intended to increase your short-term borrowing and speed up collection of debtors to help the cash balance. But that plan doesn’t help you right now, with this particular financial report that you must send out to your business’s investors and your banker. Folks generally don’t like to see a zero cash balance - it makes them kind of nervous, to put it mildly, no matter how you try to cushion it. So what do you do to avoid alarming them?

Your accountant is probably aware of a technique known as window dressing, a very simple method for making the cash balance look better. Suppose your financial year-end is October 31. Your accountant takes the cash receipts from customers paying their bills that are actually received on November 1, 2 and 3, and records them as if these cash collections had been received on October 31. After all, the argument can be made that the customers’ cheques were in the mail - that money is yours, as far as the customers are concerned, so your reports should reflect that cash inflow.

What impact does window dressing have? It reduces the amount in Debtors and increases the amount in Cash by the same amount - it has absolutely no effect on the profit figure. It just makes your cash balance look a touch better. Window dressing can also be used to improve other accounts’ balances, which we don’t go into here. All these techniques involve holding the books open to record certain events that take place after the end of the financial year (the ending Balance Sheet date) to make things look better than they actually were at the close of business on the last day of the year.

Sounds like everybody wins, doesn’t it? Your investors don’t panic and your job is safe. We have to warn you, though, that window dressing may be the first step on a slippery slope. A little window dressing today and tomorrow, who knows? Maybe giving the numbers a nudge will lead to serious financial fraud. Any way you look at it, window dressing is deceptive to your investors, who have every right to expect that the end of your fiscal year as stated on your financial reports is truly the end of your fiscal year. Think about it this way: if you’ve invested in a business that has fudged this data, how do you know what other numbers on the report are suspect?

Smoothing the rough edges off profit

Managers strive to make their numbers and to hit the milestone markers set for the business. Reporting a loss for the year, or even a dip below the profit trend line, is a red flag that investors view with alarm.

Managers can do certain things to deflate or inflate profit (the net profit) recorded in the year that are referred to as profit-smoothing techniques. Profit smoothing is also called income smoothing. Profit smoothing isn’t nearly as serious as cooking the books, or juggling the books, which refers to deliberate, fraudulent accounting practices such as recording sales revenue that hasn’t happened or not recording expenses that have happened. Cooking the books is very serious; managers can go to jail for fraudulent financial statements. Profit smoothing is more like a white lie that’s told for the good of the business, and perhaps for the good of managers as well. Managers know that there’s always some noise in the accounting system. Profit smoothing muffles the noise.

Managers of publicly owned companies whose shares are actively traded are under intense pressure to keep profits steadily rising. Security analysts who follow a particular company make profit forecasts for the business, and their buy-hold-sell recommendations are based largely on these earnings forecasts. If a business fails to meet its own profit forecast or falls short of analysts’ forecasts, the market price of its shares suffers. Share option and bonus incentive compensation plans are also strong motivations for achieving the profit goals set for the business.

The evidence is fairly strong that publicly owned businesses engage in some degree of profit smoothing. Frankly, it’s much harder to know whether private businesses do so. Private businesses don’t face the public scrutiny and expectations that public corporations do. On the other hand, key managers in a private business may have incentive bonus arrangements that depend on recorded profit. In any case, business investors and managers should know about profit smoothing and how it’s done.

Most profit smoothing involves pushing revenue and expenses into other years than they would normally be recorded. For example, if the president of a business wants to report more profit for the year, he can instruct the chief accountant to accelerate the recording of some sales revenue that normally wouldn’t be recorded until next year, or to delay the recording of some expenses until next year that normally would be recorded this year. The main reason for smoothing profit is to keep it closer to a projected trend line and make the line less jagged.

Book V, Chapter 2 explains that managers choose among alternative accounting methods for several important expenses. After making these key choices the managers should let the accountants do their jobs and let the chips fall where they may. If bottom-line profit for the year turns out to be a little short of the forecast or target for the period, so be it. This hands-off approach to profit accounting is the ideal way. However, managers often use a hands-on approach - they intercede (one could say interfere) and override the normal accounting for sales revenue or expenses.

Both managers who do it and investors who rely on financial statements in which profit smoothing has been done should definitely understand one thing - these techniques have robbing-Peter-to-pay-Paul effects. Accountants refer to these as compensatory effects. The effects on next year’s statement simply offset and cancel out the effects on this year. Less expense this year is counterbalanced by more expense next year. Sales revenue recorded this year means less sales revenue recorded next year.

Two profit histories

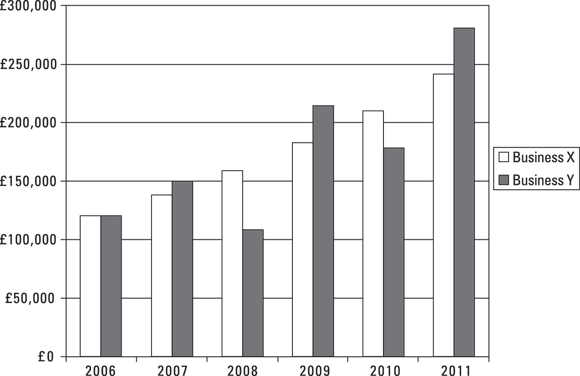

Figure 1-2 shows, side by side, the annual profit histories of two different companies over six years. Business X shows a nice, steady, upward trend of profit. Business Y, in contrast, shows somewhat of a rollercoaster ride over the six years. Both businesses earned the same total profit for the six years - in this case, £1,050,449. Their total six-year profit performance is the same, down to the last pound. Which company would you be more willing to risk your money in? We suspect that you’d prefer Business X because of the steady, upward slope of its profit history.

Figure 1-2: Comparison of two annual profit histories.

Question: Does Figure 1-2 really show two different companies - or are the two profit histories actually alternatives for the same company? The year-by-year profits for Business X could be the company’s smoothed profit, and the annual profits for Business Y could be the actual profit of the same business - the profit that would have been recorded if smoothing techniques had not been applied.

For the first year in the series, 2006, no profit smoothing occurred. Actual profit is on target. For each of the next five years, the two profit numbers differ. The under-gap or over-gap of actual profit compared with smoothed profit for the year is the amount of revenue or expenses manipulation that was done in the year. For example, in 2007 actual profit would have been too high, so the company moved some expenses that normally would be recorded the following year into 2007. In contrast, in 2008 actual profit was running too low, so the business took action to put off recording some expenses until 2011.

If a business has a particularly bad year, all the profit-smoothing tricks in the world won’t close the gap. But several smoothing techniques are available for filling the potholes and straightening the curves on the profit highway.

Profit-smoothing techniques

One common technique for profit smoothing is deferred maintenance. Many routine and recurring maintenance costs required for vehicles, machines, equipment and buildings can be put off, or deferred, until later. These costs aren’t recorded to expense until the actual maintenance is done, so putting off the work means that no expense is recorded. Or a company can cut back on its current year’s outlays for market research and product development. Keep in mind that most of these costs will be incurred next year, so the effect is to rob Peter (make next year absorb the cost) to pay Paul (let this year escape the cost).

A business can ease up on its rules regarding when slow-paying customers are decided to be bad debts (uncollectable debtors). A business can put off recording some of its bad debts expense until next year. A fixed asset out of active use may have very little or no future value to a business. Instead of writing off the non-depreciated cost of the impaired asset as a loss this year, the business may delay the write-off until next year.

So, managers have control over the timing of many expenses, and they can use this discretion for profit smoothing. Some amount of expenses can be accelerated into this year or deferred to next year in order to make for a smoother profit trend. Of course, in its external financial report a business doesn’t divulge the extent to which it has engaged in profit smoothing. Nor does the independent auditor comment on the use of profit-smoothing techniques by the business - unless the auditor thinks that the company has gone too far in massaging the numbers and that its financial statements are misleading.

Sticking to the accounting conventions

Over time, a generally accepted approach to the boundaries of acceptable number nudging has been arrived at. This hinges on the use of three conventions: conservatism, materiality and consistency.

Conservatism

Accountants are often viewed as merchants of gloom, always prone to taking a pessimistic point of view. The fact that a point of view has to be taken at all is the root of the problem. The convention of conservatism means that given a choice the accountant takes the figure that will result in a lower end profit. This might mean, for example, taking the higher of two possible expense figures. Few people are upset if the profit figure at the end of the day is higher than earlier estimates. The converse is never true.

Materiality

A strict interpretation of depreciation could lead to all sorts of trivial paperwork. For example, pencil sharpeners, staplers and paper clips, all theoretically items of fixed assets, should be depreciated over their working lives. This is obviously a useless exercise and in practice these items are written off when they’re bought.

Clearly, the level of materiality is not the same for all businesses. A multinational may not keep meticulous records of every item of machinery under £1,000. For a small business this may represent all the machinery it has.

Consistency

Even with the help of those concepts and conventions, there’s a fair degree of latitude in how you can record and interpret financial information. You need to choose the methods that give the fairest picture of how the firm is performing and stick with them. Keeping track of events in a business that’s always changing its accounting methods is very difficult. This doesn’t mean that you’re stuck with one method forever. Any change, however, is an important step.

Browsing versus Reading Financial Reports

Very few people have the time to carefully read all the information in an annual financial report - even if the report is relatively short.

Annual financial reports are long and dense documents - like lengthy legal contracts in many ways. Pick up a typical annual financial report of a public corporation: you’d need many hours (perhaps the whole day) to thoroughly read everything in the report. You’d need at least an hour or two just to read and absorb the main points in the report. How do investors in a business deal with the information overload of annual financial reports put out by businesses?

An annual financial report is like the Sunday edition of The Times or The Telegraph. Hardly anyone reads every sentence on every page of these Sunday papers - most people pick and choose what they want to read. Investors read annual financial reports like they read Sunday newspapers. The information is there if you really want to read it, but most readers pick and choose which information they have time to read.

Annual financial reports are designed for archival purposes, not for a quick read. Instead of addressing the needs of investors and others who want to know about the profit performance and financial condition of the business - but have only a very limited amount of time to do so - accountants produce an annual financial report that is a voluminous financial history of the business. Accountants leave it to the users of annual reports to extract the main points from an annual report. So, financial statement readers use relatively few ratios and other tests to get a feel for the financial performance and position of the business. Some businesses (and non-profit organisations in reporting to their members and other constituencies) don’t furnish an annual financial report. They know that few people have the time or the technical background to read through their annual financial reports. Instead, they provide relatively brief summaries that are boiled-down versions of their official financial statements. Typically, these summaries don’t provide footnotes or the other disclosures that are included in annual financial reports. These condensed financial statements, without footnotes, are provided by several non-profit organisations - credit unions, for instance. If you really want to see the complete financial report of the organisation you can ask its headquarters to send you a copy.

You should keep in mind that annual financial reports do not report everything of interest to owners, creditors and others who have a financial interest in the business. Annual reports, of course, come out only once a year - usually two months or so after the end of the company’s fiscal (accounting) year. You have to keep abreast of developments during the year by reading financial newspapers or through other means. Also, annual financial reports present the ‘sanitised’ version of events; they don’t divulge scandals or other negative news about the business.

Finally, not everything you may like to know as an investor is included in the annual financial report. For example, for US companies, information about salaries and incentive compensation arrangements with the top-level managers of the business are disclosed in the proxy statement, not in the annual financial report of the business. A proxy statement is the means by which the corporation solicits the votes of shareholders on issues that require their approval - one of which is compensation packages of top-level managers. In the US, proxy statements are filed with the SEC and are available on its EDGAR database, www.sec.gov/edgar/searchedgar/cik.htm . In the UK this information would usually appear in the body of the main report under the heading ‘Report of the Directors on Remuneration’.

The quality of financial reports varies from company to company. The Investor Relations Society (go to www.irs.org.uk and click on ‘IR Best Practice’) makes an award each year to the company producing the best (in other words, ‘complete’ and ‘clear’) set of reports and accounts.