Bookkeeping & Accounting All-in-One For Dummies (2015)

Book I

Basic Bookkeeping

Chapter 2

Getting Down to Bookkeeping Basics

In This Chapter

![]() Keeping business records

Keeping business records

![]() Getting to know the lingo

Getting to know the lingo

![]() Navigating the accounting cycle

Navigating the accounting cycle

![]() Understanding accrual accounting

Understanding accrual accounting

![]() Making sense of double-entry bookkeeping

Making sense of double-entry bookkeeping

![]() Clarifying debits and credits

Clarifying debits and credits

All businesses need to keep track of their financial transactions, which is why bookkeeping and bookkeepers are so important. Without accurate records, how can you tell whether your business is making a profit or taking a loss?

In this chapter, we cover the key aspects of bookkeeping: we introduce you to the language of bookkeeping, familiarise you with how bookkeepers manage the accounting cycle and show you how to understand the more complex type of bookkeeping - double-entry bookkeeping.

Bookkeeping: The Record-Keeping of the Business World

Bookkeeping, the methodical way in which businesses track their financial transactions, is rooted in accounting. Accounting is the total structure of records and procedures used to record, classify and report information about a business’s financial transactions. Bookkeeping involves the recording of that financial information into the accounting system while maintaining adherence to solid accounting principles.

The bookkeeper’s job is to work day in and day out to ensure that she records transactions accurately. Bookkeepers need to be detail-oriented and love working with numbers, because they deal with numbers and accounts all day long.

Bookkeepers don’t need to belong to any recognised professional body, such as the Institute of Chartered Accountants of England and Wales. You can recognise a chartered accountant by the letters ACA after the name, which indicates that she is an Associate of the Institute of Chartered Accountants. If she’s been qualified much longer, she may use the letters FCA, which indicate that the accountant is a Fellow of the Institute of Chartered Accountants.

Of course, both Scotland and Ireland have their own chartered accountant bodies with their own designations. Other accounting qualifications exist, offered by the Institute of Chartered Management Accountants (ACMA and FCMA), the Institute of Chartered Certified Accountants (ACCA and FCMA) and the Chartered Institute of Public Finance Accountants (CIPFA).

The Association of Accounting Technicians offers a bookkeeping certificate (ABC) programme that provides a good grounding in this subject. In reality, most bookkeepers tend to be qualified by experience.

If you’re after an accountant to help your business, use the appropriate chartered accountant or a chartered certified accountant because they have the most relevant experience.

If you’re after an accountant to help your business, use the appropriate chartered accountant or a chartered certified accountant because they have the most relevant experience.

On starting up their businesses, many small-business owners serve as their own bookkeepers until the business is large enough to hire a dedicated person to keep the books. Few small businesses have accountants on the payroll to check the books and prepare official financial reports; instead, they have bookkeepers (on the payroll or hired on a self-employed basis) who serve as the outside accountants’ eyes and ears. Most businesses do seek out an accountant, usually a chartered accountant (ACA or FCA), but they do so typically to submit annual accounts to the Inland Revenue, which is now part of HM Revenue & Customs.

In many small businesses today, a bookkeeper enters the business transactions on a daily basis while working inside the business. At the end of each month or quarter, the bookkeeper sends summary reports to the accountant, who then checks the transactions for accuracy and prepares financial statements such as the Profit and Loss (see Book IV, Chapter 1), and Balance Sheet (see Book IV, Chapter 2) statements.

In most cases, the accounting system is initially set up with the help of an accountant. The aim is to ensure that the system uses solid accounting principles and that the analysis it provides is in line with that required by the business, the accountant and HM Revenue & Customs. That accountant periodically reviews the system’s use to make sure that staff are handling transactions properly.

Accurate financial reports are the only way to ensure that you know how your business is doing. Your business develops these reports using the information that you, as the bookkeeper, enter into your accounting system. If that information isn’t accurate, your financial reports are meaningless: remember, ‘garbage in, garbage out’.

Accurate financial reports are the only way to ensure that you know how your business is doing. Your business develops these reports using the information that you, as the bookkeeper, enter into your accounting system. If that information isn’t accurate, your financial reports are meaningless: remember, ‘garbage in, garbage out’.

Wading through Basic Bookkeeping Lingo

Before you can take on bookkeeping and start keeping the books, you first need to get a handle on the key accounting terms. This section describes the main terms that all bookkeepers use on a daily basis.

Accounts for the Balance Sheet

Here are a few terms that you need to know:

· Balance Sheet: The financial statement that presents a snapshot of the business’s financial position (assets, liabilities and capital) as of a particular date in time. The Balance Sheet is so-called because the things owned by the business (assets) must equal the claims against those assets (liabilities and capital).

On an ideal Balance Sheet, the total assets need to equal the total liabilities plus the total capital. If your numbers fit this formula, the business’s books are in balance. (We discuss the Balance Sheet in greater detail in Book IV, Chapter 2.)

· Assets: All the items a business owns in order to run successfully, such as cash, stock, debtors, buildings, land, tools, equipment, vehicles and furniture.

· Liabilities: All the debts the business owes, such as mortgages, loans and unpaid bills.

· Capital: All the money the business owners invest in the business. When one person (sole trader) or a group of people (partnership) own a small business, the owners’ capital is shown in a Capital account. In an incorporated business (limited company), the owners’ capital is shown as shares.

Another key Capital account is Retained Earnings, which shows all business profits that have been reinvested in the business rather than paid out to the owners by way of dividends. Unincorporated businesses show money paid out to the owners in a Drawings account (or individual Drawings accounts in the case of a partnership), whereas incorporated businesses distribute money to the owners by paying dividends (a portion of the business’s profits paid out to the ordinary shareholders, typically for the year).

Accounts for the Profit and Loss statement

Following are a few terms related to the Profit and Loss statement that you need to know:

· Profit and Loss statement: The financial statement that presents a summary of the business’s financial activity over a certain period of time, such as a month, quarter or year. The statement starts with Sales made, subtracts out the Costs of Goods Sold and the Expenses, and ends with the bottom line - Net Profit or Loss. (We show you how to develop a Profit and Loss statement in Book IV, Chapter 1.)

· Income: All sales made in the process of selling the business’s goods and services. Some businesses also generate income through other means, such as selling assets that the business no longer needs or earning interest from investments. (We discuss how to track income in Book II, Chapter 2.)

· Cost of Goods Sold: All costs incurred in purchasing or making the products or services a business plans to sell to its customers. (We talk about purchasing goods for sale to customers in Book II, Chapter 3. We also talk about how the accountant would use different accounting methods to determine the cost of goods sold in Book V, Chapter 2.)

· Expenses: All costs incurred to operate the business that aren’t directly related to the sale of individual goods or services. (We review common types of expenses in Book I, Chapter 3.)

Other common terms

Some other common terms include the following:

· Accounting period: The time for which financial information is being prepared. Most businesses monitor their financial results on a monthly basis, so each accounting period equals one month. Some businesses choose to do financial reports on a quarterly basis, so the accounting period is three months. Other businesses only look at their results on a yearly basis, so their accounting period is 12 months. Businesses that track their financial activities monthly usually also create quarterly and annual reports (a year-end summary of the business’s activities and financial results) based on the information they gather.

· Accounting year-end: In most cases a business accounting year is 12 months long and ends 12 months on from when the business started or at some traditional point in the trading cycle for that business. Many businesses have year-ends of 31 March (to tie in with the tax year) and 31 December (to tie in with the calendar year). You’re allowed to change your business year-end to suit your business.

For example, if you started your business on July 1, your year-end is 30 June (12 months later). If, however, your industry traditionally has 31 December as the year-end, you’re quite in order to change to this date. For example, most retailers have 31 December as their year-end. You do, of course, have to let HM Revenue & Customs know and get its formal acceptance.

· Trade Debtors (also known as Accounts Receivable): The account used to track all customer sales made on credit. Credit refers not to credit-card sales, but to sales in which the business gives a customer credit directly, and which the business needs to collect from the customer at a later date. (We discuss how to monitor Trade Debtors in Book II, Chapter 2.)

· Trade Creditors (also known as Accounts Payable): The account used to track all outstanding bills from suppliers, contractors, consultants and any other businesses or individuals from whom the business buys goods or services. (We talk about managing Trade Creditors in Book II, Chapter 3.)

· Depreciation: An accounting method used to account for the ageing and use of assets. For example, if you own a car, you know that the value of the car decreases each year (unless you own one of those classic cars that goes up in value). Every major asset a business owns ages and eventually needs replacement, including buildings, factories, equipment and other key assets. (We discuss the basics of depreciation in Book III, Chapter 3, and then discuss how your accountant decides on which depreciation method to use in Book V, Chapter 2).

· Nominal (or General) Ledger: A ledger that summarises all the business’s accounts. The Nominal Ledger is the master summary of the bookkeeping system. (We discuss posting to the Nominal Ledger in Book I, Chapter 4.)

· Stock (or Inventory): The account that tracks all products sold to customers. (We review stock valuation and control in Book II, Chapter 3.)

· Journals: Where bookkeepers keep records (in chronological order) of daily business transactions. Each of the most active accounts, including Cash, Trade Creditors and Trade Debtors, has its own journal. (We discuss entering information into journals in Book I, Chapter 4.)

· Payroll: The way a business pays its employees. Managing payroll is a key function of the bookkeeper and involves reporting many aspects of payroll to HM Revenue & Customs, including Pay As You Earn (PAYE) taxes to be paid on behalf of the employee and employer, and National Insurance Contributions (NICs). In addition, a range of other payments such as Statutory Sick Pay (SSP) and maternity/paternity pay may be part of the payroll function. (We discuss employee payroll in Book III, Chapter 2, including the recent Real Time Information scheme.)

· Trial Balance: How you test to ensure that the books are in balance before pulling together information for the financial reports and closing the books for the accounting period. (We discuss the Trial Balance in Book III, Chapter 3.)

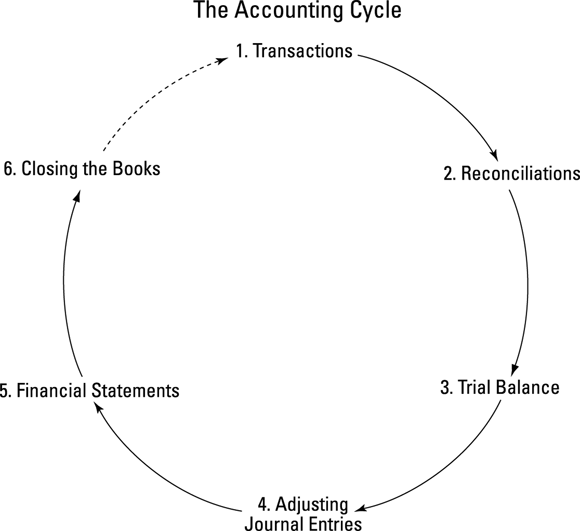

Pedalling through the Accounting Cycle

As a bookkeeper, you complete your work by completing the tasks of the accounting cycle, so-called because the workflow is circular: entering transactions, manipulating the transactions through the accounting cycle, closing the books at the end of the accounting period and then starting the entire cycle again for the next accounting period.

The accounting cycle has six basic steps, shown in Figure 2-1.

Figure 2-1: The accounting cycle.

1. Transactions: Financial transactions start the process. Transactions can include the sale or return of a product; the purchase of supplies for business activities or any other financial activity that involves the exchange of the business’s assets; the establishment or payoff of a debt; or the deposit from or payout of money to the business’s owners. All sales and expenses are transactions that must be recorded. We cover transactions in greater detail throughout the book as we discuss how to record the basics of business activities - recording sales, purchases, asset acquisition or disposal, taking on new debt or paying off debt.

You post the transactions to the relevant account. These accounts are part of the Nominal Ledger, where you can find a summary of all the business’s accounts. A computerised accounting system automatically journals the appropriate debits and credits to the correct accounts. For example, if a purchase invoice for British Telecom is entered as a transaction, the Creditors Ledger will be credited and the telephone Nominal account will be debited.

2. Reconciliations: Once you’ve entered all your transactions, you need to reconcile your bank account(s) to ensure that all your banking entries have been recorded correctly.

3. Trial Balance: At the end of the accounting period (which may be a month, quarter or year depending on your business’s practices), you prepare a trial balance. You must then review each account on the Trial Balance to ensure accuracy.

4. Adjusting journal entries: Having reviewed the Trial Balance, you may need to make adjustments to some of the accounts in order to make corrections. You also need to account for the depreciation of assets and to adjust for one-time payments (such as insurance). These need to be allocated on a monthly basis, in order to match monthly expenses with monthly revenues more accurately. After you make the adjustments, run another Trial Balance to ensure that you’re happy with the accounts.

5. Financial statements: You run the Balance Sheet and Profit and Loss statement using the corrected account balances.

6. Closing the books: You close the books for the Revenue and Expense accounts and begin the entire cycle again.

At the end of the accounting year (year-end) you close off all the accounting ledgers. This situation means that Revenue and Expense accounts must start with a zero balance at the beginning of each new accounting year. In contrast, you carry over Asset, Liability and Capital account balances from year to year, because the business doesn’t start each cycle by getting rid of old assets and buying new assets, paying off and then taking on new debt, or paying out all claims to owners and then collecting the money again.

At the end of the accounting year (year-end) you close off all the accounting ledgers. This situation means that Revenue and Expense accounts must start with a zero balance at the beginning of each new accounting year. In contrast, you carry over Asset, Liability and Capital account balances from year to year, because the business doesn’t start each cycle by getting rid of old assets and buying new assets, paying off and then taking on new debt, or paying out all claims to owners and then collecting the money again.

Understanding Accounting Methods

Many not-for-profit organisations, such as sports clubs, have really simple accounting needs. These organisations aren’t responsible to shareholders to account for their financial performance, though they’re responsible to their members for the safe custody of their subscriptions and other funds. Consequently, the accounting focus isn’t on measuring profit but more on accounting for receipts and payments. In these cases, a simple cash-based accounting system may well suffice, which allows for only cash transactions -giving or receiving credit is not possible.

However, complications may arise when members don’t pay their subscriptions during the current accounting year, and the organisation needs to reflect this situation in its accounts. In this case, the accrual accounting method is best (see the later section ‘Recording right away with accrual accounting’).

A few businesses operate on a cash basis, and their owners can put forward a good case for using this method. However, most accountants and HM Customs & Revenue don’t accept this method because it doesn’t give an accurate measure of profit (or loss) for accounting periods.

In the next sections, we briefly explain how cash-based accounting works before dismissing it in favour of the more accepted and acceptable accrual method.

Realising the limitations of cash-based accounting

With cash-based accounting, you record all transactions in the books when cash actually changes hands, which means when the business receives cash payment from customers or pays out cash for purchases or other services. Cash receipt or payment can be in the form of cash, cheque, credit card, electronic transfer or other means used to pay for an item.

With cash-based accounting, you record all transactions in the books when cash actually changes hands, which means when the business receives cash payment from customers or pays out cash for purchases or other services. Cash receipt or payment can be in the form of cash, cheque, credit card, electronic transfer or other means used to pay for an item.

Cash-based accounting can’t be used when a business sells products on credit and collects the money from the customer at a later date. No provision exists in the cash-based accounting method to record and track money due from customers at some point in the future.

This situation also applies for purchases. With the cash-based accounting method, the business only records the purchase of supplies or goods that are to be sold later when it actually pays cash. When the business buys goods on credit to be paid later, it doesn’t record the transaction until the cash is actually paid out.

Depending on the size of your business, you may want to start out with cash-based accounting. Many small businesses run by a sole proprietor or a small group of partners use the easier cash-based accounting system. When your business model is simple - you carry no stock, start and finish each job within a single accounting period, and pay and get paid within this period - the cash-based accounting method can work for you. But as your business grows, you may find it necessary to switch to accrual accounting in order to track revenues and expenses more accurately and to satisfy the requirements of the external accountant and HM Revenue & Customs. The same basic argument also applies to not-for-profit organisations.

Cash-based accounting does a good job of tracking cash flow, but the system does a poor job of matching revenues earned with money laid out for expenses. This deficiency is a problem particularly when, as often happens, a business buys products in one month and sells those products in the next month.

Say you buy products in June paying £1,000 cash, with the intent to sell them that same month. You don’t sell the products until July, which is when you receive cash for the sales. When you close the books at the end of June, you have to show the £1,000 expense with no revenue to offset it, meaning that you have a loss that month. When you sell the products for £1,500 in July, you have a £1,500 profit. So, your monthly report for June shows a £1,000 loss, and your monthly report for July shows a £1,500 profit, when in reality you had revenues of £500 over the two months. Using cash-based accounting, you can never be sure that you have an accurate measure of profit or loss - but because cash-based accounting is for not-for-profit organisations, this isn’t surprising.

Say you buy products in June paying £1,000 cash, with the intent to sell them that same month. You don’t sell the products until July, which is when you receive cash for the sales. When you close the books at the end of June, you have to show the £1,000 expense with no revenue to offset it, meaning that you have a loss that month. When you sell the products for £1,500 in July, you have a £1,500 profit. So, your monthly report for June shows a £1,000 loss, and your monthly report for July shows a £1,500 profit, when in reality you had revenues of £500 over the two months. Using cash-based accounting, you can never be sure that you have an accurate measure of profit or loss - but because cash-based accounting is for not-for-profit organisations, this isn’t surprising.

Because accrual accounting is the only accounting method acceptable to accountants and HM Revenue & Customs, we concentrate on this method throughout the book. If you choose to use cash-based accounting because you have a cash-only business and a simple trading model, don’t panic: most of the bookkeeping information here is still useful, but you don’t need to maintain some of the accounts, such as Trade Debtors and Trade Creditors, because you aren’t recording transactions until cash actually changes hands. When you’re using a cash-based accounting system and you start to sell things on credit, though, you’d better have a way to track what people owe you!

Our advice is to use the accrual accounting method right from the beginning. When your business grows and your business model changes, you need the more sophisticated and legally required accrual accounting.

Recording right away with accrual accounting

With accrual accounting, you record all transactions in the books when they occur, even when no cash changes hands. For example, when you sell on credit, you record the transaction immediately and enter it into a Trade Debtors account until you receive payment. When you buy goods on credit, you immediately enter the transaction into a Trade Creditors account until you pay out cash.

Like cash-based accounting, accrual accounting has drawbacks: it does a good job of matching revenues and expenses, but a poor job of tracking cash. Because you record income when the transaction occurs and not when you collect the cash, your Profit and Loss statement can look great even when you don’t have cash in the bank. For example, suppose you’re running a contracting business and completing jobs on a daily basis. You can record the revenue upon completion of the job even when you haven’t yet collected the cash. When your customers are slow to pay, you may end up with lots of income but little cash. Remember - never confuse profit and cash. In the short term, cash flow is often more important than profit, but in the long term profit becomes more important. But don’t worry just yet; in Book II, Chapter 2 we tell you how to manage your Trade Debtors so that you don’t run out of cash because of slow-paying customers.

Many businesses that use the accrual accounting method monitor cash flow on a weekly basis to be sure that they’ve enough cash on hand to operate the business. If your business is seasonal, such as a landscaping business with little to do during the winter months, you can establish short-term lines of credit through your bank to maintain cash flow through the lean times.

Seeing Double with Double-Entry Bookkeeping

All businesses use double-entry bookkeeping to keep their books, whether they use the cash-based accounting method or the accrual accounting method. Double-entry bookkeeping - so-called because you enter all transactions twice - helps to minimise errors and increase the chance that your books balance.

When it comes to double-entry bookkeeping, the key formula for the Balance Sheet (Assets = Liabilities + Capital) plays a major role.

Double-entry bookkeeping goes way back

No one’s really sure who invented double-entry bookkeeping. The first person to put the practice on paper was Benedetto Cotrugli in 1458, but mathematician and Franciscan monk Luca Pacioli is most often credited with developing double-entry bookkeeping. Although Pacioli is called the Father of Accounting, accounting actually occupies only one of five sections of his book, Everything About Arithmetic, Geometry and Proportions, which was published in 1494.

Pacioli didn’t actually invent double-entry bookkeeping; he just described the method used by merchants in Venice during the Italian Renaissance period. He’s most famous for his warning to bookkeepers: ‘A person should not go to sleep at night until the debits equal the credits!’

Golden rules of bookkeeping

You have some simple rules to remember when getting to grips with double-entry bookkeeping.

First of all, remember that a debit is on the left side of a transaction and a credit is on the right side of a transaction. Then apply the following rules:

· If you want to increase an asset, you must debit the Assets account.

· To decrease an asset, you must credit the Assets account.

· To increase a liability, you credit the Liabilities account.

· To decrease a liability, you debit the Liabilities account.

· If you want to record an expense, you debit the Expense account.

· If you need to reduce an expense, you credit the Expense account.

· If you want to record income, you credit the Income account.

· If you want to reduce income, you debit the Income account.

Copy Table 2-1 and have it on your desk when you start keeping your own books (a bit like the chief accountant in the ‘Sharing a secret’ sidebar). We guarantee that the table can help to keep your debits and credits straight.

Table 2-1 How Credits and Debits Impact Your Accounts

|

Account Type |

Debits |

Credits |

|

Assets |

Increase |

Decrease |

|

Liabilities |

Decrease |

Increase |

|

Income |

Decrease |

Increase |

|

Expenses |

Increase |

Decrease |

Believe it or not, identifying the difference becomes second nature as you start making regular entries in your bookkeeping system. But, to make things easier for you, Table 2-1 is a chart that bookkeepers and accountants commonly use. Everyone needs help sometimes!

Here’s an example of the practice in action. Suppose that you purchase a new desk for your office that costs £1,500. This transaction actually has two parts: you spend an asset (cash) to buy another asset (furniture). So, you must adjust two accounts in your business’s books: the Cash account and the Furniture account. The transaction in a bookkeeping entry is as follows (we talk more about how to do initial bookkeeping entries in Book I, Chapter 4):

|

Account |

Debit |

Credit |

|

Furniture |

£1,500 |

|

|

Cash |

£1,500 |

To purchase a new desk for the office

In this transaction, you record the accounts impacted by the transaction. The debit increases the value of the Furniture account, and the credit decreases the value of the Cash account. For this transaction, both accounts impacted are Asset accounts. So looking at how the Balance Sheet is affected, you can see that the only changes are to the asset side of the Balance Sheet equation:

· Assets = Liabilities + Capital

· Furniture increase = No change to this side of the equation

· Cash decrease

In this case, the books stay in balance because the exact pounds sterling amount that increases the value of your Furniture account decreases the value of your Cash account. At the bottom of any journal entry, include a brief explanation that explains the purpose of the entry. In the first example, we indicate that this entry was ‘To purchase a new desk for the office’.

Practising with an example

To show you how you record a transaction that impacts both sides of the Balance Sheet equation, here’s an example that records the purchase of stock. Suppose that you purchase £5,000 worth of widgets on credit. (Have you always wondered what widgets are? Can’t help you. They’re just commonly used in accounting examples to represent something purchased where what’s purchased is of no real significance.) These new widgets add value to your Stock Asset account and also add value to your Trade Creditors account. (Remember, the Trade Creditors account is a Liability account where you track bills that need to be paid at some point in the future.) The bookkeeping transaction for your widget purchase looks as follows:

|

Account |

Debit |

Credit |

|

Stock |

£5,000 |

|

|

Trade Creditors |

£5,000 |

To purchase widgets for sale to customers

This transaction affects the Balance Sheet equation as follows:

· Assets = Liabilities + Capital

· Stock increases = Creditor increases + No change

In this case, the books stay in balance because both sides of the equation increase by £5,000.

You can see from the two example transactions how double-entry bookkeeping helps to keep your books in balance - as long as you make sure that each entry into the books is balanced. Balancing your entries may look simple here, but sometimes bookkeeping entries can get complex when the transaction impacts more than two accounts.

Sharing a secret

Don’t feel embarrassed if you forget which side the debits go on and which side the credits go on. One often-told story is of a young clerk in an accounts office plucking up the courage to ask the chief accountant, who was retiring that day, why for 30 years he had at the start of each day opened up his drawer and read the contents of a piece of paper before starting work. The chief accountant at first was reluctant to spill the beans, but ultimately decided he had to pass on his secret - and who better than an up-and-coming clerk? Swearing the young clerk to secrecy, he took out the piece of paper and showed it to him. The paper read: ‘Debit on the left and credit on the right.’

Have a Go

In this section you can practise double-entry bookkeeping by having a go at the next few exercises. You can find the answers at the end of the chapter. Good luck! By the way, if you get stuck, remember to look back at the section ‘Golden rules of bookkeeping’, earlier in this chapter.

1. Have a look at the following list and decide whether the items described belong in the Profit and Loss statement or the Balance Sheet.

|

Item |

Profit and Loss or Balance Sheet? |

|

Telephone bill |

|

|

Purchase of motor vehicles |

|

|

Bank loan |

|

|

Petty cash |

|

|

Sales |

|

|

Materials purchased for resale |

2. Write the journal entry for the following, as shown in the furniture example in the previous section:

On 15 February, you buy new products (to be sold in your shop) on credit for £3,000. How would you enter this transaction in your books?

|

Date |

Account |

Debit |

Credit |

3. Write down the journal entry for the following transaction:

On 31 March, you sell £5,000 worth of goods and receive £5,000 in cash.

|

Date |

Account |

Debit |

Credit |

4. Write down the journal entry for the following transaction:

On 30 June, you sell £3,000 worth of goods on credit. You don’t get cash. Customers will pay you after you bill them. How do you record the sales transaction?

|

Date |

Account |

Debit |

Credit |

5. Write down the journal entry for the following transaction:

On 30 September, you buy office supplies for £500 using a cheque. How do you record the transaction?

|

Date |

Account |

Debit |

Credit |

6. In which two accounts would you record the cash purchase of products (stock)?

7. In which two accounts would you record the purchase of furniture for your office using a credit card?

8. In which two accounts would you record the payment of rent to your landlord in cash?

9. If your accountant wants to know how many products are still on the shelves after you closed the books for an accounting period, which account would you show?

10. If a customer buys your product on credit, in which account would you record the transaction?

11. You receive an invoice for some goods received. Where do you record the invoice in the accounting system, so that you can pay it in the future?

12. Which report would you run to ensure that your accounts are in balance?

13. If you find a mistake, what type of entry would you make to get your books back in balance?

Answering the Have a Go Questions

1. Telephone bill: A telephone bill is usually considered to be an overhead of the business. As such, it would be included in the Profit and Loss account and classified as an expense.

Purchase of motor vehicle: A motor vehicle is likely to be kept in the business for a long period of time, usually 3-4 years or more. This is categorised as a fixed asset and would be included in the Balance Sheet.

Bank loan: The owner or directors of the business may have taken out a bank loan to provide funds for a large purchase. A bank loan is something that the business owes to a third party, and it’s considered to be a liability. As such, it’ll be shown in the Balance Sheet.

Petty cash: Although it may be a small amount of money held in a petty cash tin, it’s still considered to be an asset. It’ll therefore be shown as an asset in the Balance Sheet.

Sales: Once your business starts generating income through sales, this must be entered into a Profit and Loss account. Sales is the first category of a Profit and Loss statement; when you deduct costs from this, a profit or loss can be calculated.

Materials purchased for resale: You may buy goods and sell them on in their present state, or you may buy materials that can be used to manufacture a product. Either way, these costs are considered to be direct costs (they’re directly attributed to making the products you sell) and as such they need to be shown as Cost of Goods Sold in the Profit and Loss account.

2. In this transaction, you’d debit the Purchases account to show the additional purchases made during that period and credit the Creditors account.

Remember, if you’re increasing a liability (such as Creditors) you must credit that account. When recording an expense such as Purchases, you should debit that account. Because you’re buying the goods on credit, that means you have to pay the bill at some point in the future.

|

Date |

Account |

Debit |

Credit |

|

15 Feb |

Purchases |

£3,000 |

|

|

15 Feb |

Creditors |

£3,000 |

3. As you think about the journal entry, you may not know whether something is a credit or a debit.

As you know from our discussions earlier in the chapter, cash is an asset, and if you increase the value of an asset, you debit that account. In this question, because you received cash, you know that the Cash account needs to be a debit. So your only choice is to make the Sales account the account to be credited. This is correct because all Income accounts are increased by a credit. If you’re having trouble figuring these entries out, look again at Table 2-1.

|

Date |

Account |

Debit |

Credit |

|

31 March |

Cash |

£5,000 |

|

|

31 March |

Sales |

£5,000 |

4. In this question, rather than taking in cash, the customers are allowed to pay on credit, so you need to debit the Asset account Debtors.

(Remember: When increasing an asset, you debit that account.) You’ll credit the Sales account to track the additional revenue. (When recording income, you credit the Income account.)

|

Date |

Account |

Debit |

Credit |

|

30 June |

Debtors |

£3,000 |

|

|

30 June |

Sales |

£3,000 |

5. In this question, you’re paying with a cheque, so the transaction is recorded in your Cash account.

The Cash account tracks the amount in your bank account. Any cash, cheques, debit cards or other types of transactions that are taken directly from your bank account are always entered as a credit. This is because you’re decreasing an asset (say, cash); therefore, you must credit the Cash account. All money paid out for expenses is always a debit. When recording an expense, always post a debit to the Expense account.

|

Date |

Account |

Debit |

Credit |

|

30 Sept |

Office Supplies |

£500 |

|

|

30 Sept |

Cash |

£500 |

6. In which two accounts would you record the cash purchase of products (stock)?

Record the cash spent in the Cash account. The product cost should be recorded in the Stock account, until the products are sold. A business acquires products either by buying them (retailers) or by producing them (manufacturers). After the product is sold, the product cost should be taken out of Stock and added to the Cost of Goods Sold expense account. The unsold units are left in Stock, and this Stock is checked periodically, when a physical count of the stock is done. Most businesses have an automatic stock update facility, which makes it easy to manage. If in doubt, check with an accountant first and she will be able to advise on the best method to use.

7. Record the furniture in an Asset account called Furniture and record the credit card transaction in a Liability account called Credit Card.

You’d record the charge on the credit card in a Liability account called Credit Card. Cash wouldn’t be paid until the credit card bill is due to be paid. Furniture is always listed as an asset on your Balance Sheet. Anything you buy that you expect to use for more than one year is a fixed asset, rather than an expense.

8. Record the rent payment in an Expense account called Rent.

Record the cash used in a Current Asset account called Cash. Cash is always a Current Asset account (unless your bank account is overdrawn and then it would be considered a liability and would be shown in Current Liabilities). Rent is always an expense.

9. Stock account.

The Stock account is adjusted at the end of each accounting period to show the total number of products remaining to be sold at the end of the period.

10. Debtors Ledger.

This is the account that is used to track all customer purchases bought on credit. In addition to this account, which summarises all products bought on credit, you’d also need to enter the purchases into the individual accounts of each of your customers so you can bill them and track their payments.

11. Creditors Ledger.

You record all unpaid invoices in Trade Creditors.

12. You would run a Trial Balance.

The Trial Balance is a working tool that helps you test whether your books are in balance before you prepare your financial statements.

13. A journal.

At the end of an accounting period you correct any mistakes by entering journals. These entries also need to be in balance. You’ll always have at least one account that’s a debit and one that’s a credit.