Bookkeeping & Accounting All-in-One For Dummies (2015)

Book V

Accountants: Managing the Business

Chapter 3

Managing Profit Performance

In This Chapter

![]() Recasting the Profit and Loss statement to focus on profit factors

Recasting the Profit and Loss statement to focus on profit factors

![]() Following two trails to profit

Following two trails to profit

![]() Breaking even - not the goal, but a useful point of reference

Breaking even - not the goal, but a useful point of reference

![]() Doing what-if analysis

Doing what-if analysis

![]() Making trade-offs: Be very careful!

Making trade-offs: Be very careful!

As a manager you get paid to make profit happen. That’s what separates you from the non-manager employees at your business. Of course, you have to be a motivator, innovator, consensus builder, lobbyist and maybe sometimes a babysitter too. But the real purpose of your job is to control and improve the profit of your business. No matter how much your staff love you (or do they love those doughnuts you bring in every Monday?), if you don’t meet your profit goals, you’re facing the unemployment line.

You have to be relentless in your search for better ways to do things. Competition in most industries is fierce, and you can never take profit performance for granted. Changes take place all the time - changes initiated by the business and changes pressured by outside forces. Maybe a new superstore down the street is causing your profit to fall off, and you decide that you’ll have a huge sale, complete with splashy ads on TV, to draw customers into the shop.

Slow down; not so fast! First make sure that you can afford to cut prices and spend money on advertising and still turn a profit. Maybe price cuts and splashy ads will keep your cash register singing and the kiddies smiling, but you need to remember that making sales doesn’t guarantee that you make a profit. As all you experienced business managers know, profit is a two-headed beast - profit comes from making sales and controlling expenses.

So how do you determine what effect price cuts and advertising costs may have on your bottom line? By turning to your beloved accounting staff, of course, and asking for some what-if reports (like ‘What if we offer a 15 per cent discount?’).

This chapter shows you how to identify the key variables that determine what your profit would be if you changed certain factors (such as prices).

Redesigning the External Profit and Loss Statement

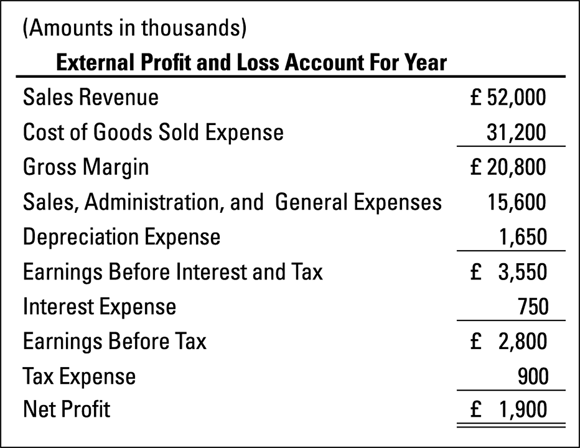

To begin, Figure 3-1 presents the Profit and Loss statement of a business (the same example is used in Book VI, Chapter 1). Figure 3-1 shows an external Profit and Loss statement - the Profit and Loss statement that’s reported to the outside investors and creditors of the business. The expenses in Figure 3-1 are presented as they’re usually disclosed in an external statement.

To begin, Figure 3-1 presents the Profit and Loss statement of a business (the same example is used in Book VI, Chapter 1). Figure 3-1 shows an external Profit and Loss statement - the Profit and Loss statement that’s reported to the outside investors and creditors of the business. The expenses in Figure 3-1 are presented as they’re usually disclosed in an external statement.

Figure 3-1: Example of a business’s external Profit and Loss statement.

The managers of the business should understand this Profit and Loss statement, of course. But the external Profit and Loss statement isn’t entirely adequate for management decision-making; this profit report falls short of providing all the information about expenses needed by managers.

Before moving on to the additional information managers need, take a quick look at the external Profit and Loss statement (Figure 3-1). Here are some key points:

· The business represented by this Profit and Loss statement sells products and therefore has a cost of goods sold expense. In contrast, companies that sell services (airlines, cinemas, consultants and so on) don’t have a cost of goods sold expense, because all their sales revenue goes toward meeting operating expenses and then providing profit.

·  The external Profit and Loss statement shown in Figure 3-1 is prepared according to authorised accounting methods and disclosure standards, but keep in mind that these financial reporting standards are designed for reporting information outside the business. After a Profit and Loss statement is released to people outside the business, a business has no control over the circulation of its statement. The accounting profession, in deciding on the information for disclosure in external Profit and Loss statements, has attempted to strike a balance. On the one side are the needs of those who have invested capital in the business and have loaned money to the business; clearly they have the right to receive enough information to evaluate their investments in the business and their loans to the business. On the other side is the need of the business to keep certain information confidential and out of the hands of its competitors. What it comes down to is that certain information that outside investors and creditors might find interesting and helpful doesn’t, in fact, legally have to be disclosed.

The external Profit and Loss statement shown in Figure 3-1 is prepared according to authorised accounting methods and disclosure standards, but keep in mind that these financial reporting standards are designed for reporting information outside the business. After a Profit and Loss statement is released to people outside the business, a business has no control over the circulation of its statement. The accounting profession, in deciding on the information for disclosure in external Profit and Loss statements, has attempted to strike a balance. On the one side are the needs of those who have invested capital in the business and have loaned money to the business; clearly they have the right to receive enough information to evaluate their investments in the business and their loans to the business. On the other side is the need of the business to keep certain information confidential and out of the hands of its competitors. What it comes down to is that certain information that outside investors and creditors might find interesting and helpful doesn’t, in fact, legally have to be disclosed.

· The Profit and Loss statement doesn’t report the financial effects of the company’s profit-making activities - that is, the increases and decreases in its assets and liabilities caused by revenue and expenses. Managers need to control these financial effects, for which purpose they need the complete financial picture provided by the two other primary financial statements (the Balance Sheet and the cash flow statement) in addition to the Profit and Loss statement. See Book IV, Chapters 2 and 3 for more about these two other primary financial statements.

Basic Model for Management Profit and Loss Account

Figure 3-2 presents a model for a management Profit and Loss statement using the same business as the example whose external Profit and Loss statement is shown in Figure 3-1. Many lines of information are exactly the same - sales revenue and cost of goods sold expense for instance - and thus gross margins are the same. The last five lines in the two statements are the same, starting with operating profit (earnings before interest and corporation tax) down to the bottom line. In other respects, however, there are critical differences between the two profit reports.

Figure 3-2: Management Profit and Loss statement model.

First, note that total unit sales volume and per unit amounts are included in the management Profit and Loss statement (Figure 3-2). The business appears to sell only one product; the 520,000 units total sales volume is from sales of this product. In fact, most businesses sell a mix of many different products. The company’s various managers need detailed sales revenue and cost information for each product, or product line, or segment of the business they’re responsible for. To keep the illustration easy to follow we’ve collapsed the business’s entire sales into one ‘average’ product. Instead of grappling with 100 or 1,000 different products, we condensed them all into one proxy product. The main purpose of Figure 3-2 is to show a basic template, or model, that can be used for the more detailed reports to different managers in the business organisation.

Variable versus fixed operating expenses

Another fundamental difference between the external profit report (Figure 3-1) and the internal profit report (Figure 3-2) is that the company’s operating expenses (sales, administration and general expenses plus depreciation expense) are separated into two different categories in the management report:

· Variable expenses: The revenue-driven expenses that depend directly on the total sales revenue amount for the period. These expenses move in step with changes in total sales revenue. Commissions paid to salespersons based on a percentage of the amount of sales are a common example of variable operating expenses.

· Fixed expenses: The operating expenses that are relatively fixed in amount for the period, regardless of whether the company’s total unit sales (sales volume) had been substantially more, or substantially less, than the 520,000 units that it actually sold during the year. An example of a fixed operating expense is the annual business rates on the company’s property. Also, depreciation is a fixed expense; a certain amount of depreciation expense is recorded to the year regardless of actual sales volume.

The management Profit and Loss statement does not, we repeat not, present different profit numbers for the year compared with the profit numbers reported in the company’s external Profit and Loss statement. Note that operating profit for the year (or earnings before interest and tax expenses) is the same as reported outside the business - in Figures 3-1 and 3-2 this number is the same. And in reading down the rest of the two Profit and Loss statements, note that earnings before tax and bottom-line net profit are the same in both the external and internal reports. The external Profit and Loss statement of the business reports a broad, all-inclusive group of ‘Sales, Administration and General Expenses’, and a separate expense for depreciation. In contrast, the management Profit and Loss statement reveals information about how the operating expenses behave relative to the sales of the business. The actual reporting of expenses in external Profit and Loss statements varies from business to business - but you never see Profit and Loss statements in which operating expenses are sorted between variable and fixed.

The management Profit and Loss statement does not, we repeat not, present different profit numbers for the year compared with the profit numbers reported in the company’s external Profit and Loss statement. Note that operating profit for the year (or earnings before interest and tax expenses) is the same as reported outside the business - in Figures 3-1 and 3-2 this number is the same. And in reading down the rest of the two Profit and Loss statements, note that earnings before tax and bottom-line net profit are the same in both the external and internal reports. The external Profit and Loss statement of the business reports a broad, all-inclusive group of ‘Sales, Administration and General Expenses’, and a separate expense for depreciation. In contrast, the management Profit and Loss statement reveals information about how the operating expenses behave relative to the sales of the business. The actual reporting of expenses in external Profit and Loss statements varies from business to business - but you never see Profit and Loss statements in which operating expenses are sorted between variable and fixed.

Virtually every business has variable operating expenses, which move up and down in tight proportion to changes in unit sales volume or sales revenue. Here are some examples of common variable operating expenses:

Virtually every business has variable operating expenses, which move up and down in tight proportion to changes in unit sales volume or sales revenue. Here are some examples of common variable operating expenses:

· Cost of goods sold expense - the cost of the products sold to customers

· Commissions paid to salespeople based on their sales

· Transportation costs of delivering products to customers

· Fees that a business pays to a bank when a customer uses a credit card such as Visa, MasterCard or American Express

The management Profit and Loss statement (Figure 3-2) can be referred to as the internal profit report, because it’s for management eyes only and doesn’t circulate outside the business - although it may be the target of industrial intelligence gathering and perhaps even industrial espionage by competitors. Remember that in the external Profit and Loss statement only one lump sum for the category of sales, administrative and general (SA&G) expenses is reported - a category for which some of the expenses are fixed but some are variable. What you need to do is have your accountant carefully examine these expenses to determine which are fixed and which are variable. (Some expenses may have both fixed and variable components, but we don’t go into these technical details.)

Further complicating the matter somewhat is the fact that the accountant needs to divide variable expenses between those that vary with sales volume (total number of units sold) and those that vary with sales revenue (total pounds of sales revenue). The following examples outline this important distinction:

· An example of an expense driven by sales volume is the cost of shipping and packaging. This cost depends strictly on the number of units sold and generally is the same regardless of how much the item inside the box costs.

· An example of an expense driven by sales revenue is the sales commission paid to salespersons, which directly depends on the amount of sales made to customers. Other examples are franchise fees based on total sales revenue of retailers, business premises rental contracts that include a clause that bases monthly rent on sales revenue, and royalties that are paid for the right to use a well-known name or a trademarked logo in selling the company’s products and that are based on total sales revenue.

The business represented in Figure 3-2 has just one variable operating expense - an 8 per cent sales commission, resulting in an expense total of £4.16 million (£52 million sales revenue × 8 per cent). Of course, a real business probably would have many different variable operating expenses, some driven by unit sales volume and some driven by total sales revenue pounds. But the basic idea is the same for all of them and one variable operating expense serves the purpose here. Also, cost of goods sold expense is itself a sales volume driven expense (see Book V, Chapter 2 regarding different accounting methods for measuring this expense). The example shown in Figure 3-2 is a bit oversimplified - the business sells only one product and has only one variable operating expense - but the main purpose is to present a general template that can be tailored to fit the particular circumstances of a business.

Fixed operating expenses are the many different costs that a business is obliged to pay and can’t decrease over the short run without major surgery on the human resources and physical facilities of the business. You must distinguish fixed expenses from your variable operating expenses.

As an example of fixed expenses, consider a typical self-service car wash business - you know, the kind where you drive in, put some coins in a box and use the water spray to clean your car. Almost all the operating costs of this business are fixed: rent on the land, depreciation of the structure and the equipment, and the annual insurance premium cost don’t depend on the number of cars passing through the car wash. The only variable expenses are probably the water and the soap.

If you want to decrease fixed expenses significantly, you need to downsize the business (lay off workers, sell off property and so on). When looking at the various ways you have for improving your profit, significantly cutting down on fixed expenses is generally the last-resort option. Refer to ‘Improving profit’, later in this chapter, for the better options.

Better than anyone else, managers know that sales for the year could have been lower or higher. A natural question is, ‘What difference in the profit would there have been at the lower or higher level of sales?’ If you’d sold 10 per cent fewer total units during the year, what would your net profit (bottom-line profit) have been? You might guess that profit would have slipped 10 per cent but that would not have been the case. In fact, profit would have slipped by much more than 10 per cent. Are you surprised? Read on for the reasons.

Why wouldn’t profit fall the same percentage as sales? The answer is because of the nature of fixed expenses - just because your sales are lower doesn’t mean that your expenses are lower. Fixed expenses are the costs of doing business that, for all practical purposes, are stuck at a certain amount over the short term. Fixed expenses don’t react to changes in the sales level. Here are some examples of fixed expenses:

· Interest on money that the business has borrowed

· Employees’ salaries and benefits

· Business rates

· Fire insurance

A business can downsize its assets and therefore reduce its fixed expenses to fit a lower sales level, but that can be a drastic reaction to what may be a temporary downturn. After deducting cost of goods sold, variable operating expenses and fixed operating expenses, the next line in the management Profit and Loss statement is operating profit, which is also called earnings before interest and tax (or EBIT). This profit line in the report is a critical juncture that managers need to fully appreciate.

From operating profit (EBIT) to the bottom line

After deducting all operating expenses from sales revenue, you get to earnings before interest and tax (EBIT), which is £3.55 million in the example. Operating is an umbrella term that includes cost of goods sold expense and all other expenses of making sales and operating your business - but not interest and tax. Sometimes EBIT is called operating profit, or operating earnings, to emphasise that profit comes from making sales and controlling operating expenses. This business earned £3.55 million operating profit from its £52 million sales revenue - which seems satisfactory. But is its £3.55 million EBIT really good enough? What’s the reference for answering this question?

The main benchmark for judging EBIT is whether this amount of profit is adequate to cover the cost of capital of the business. A business must secure money to invest in its various assets - and this capital has a cost. A business has to pay interest on its debt capital, and it should earn enough after-tax net profit (bottom-line profit) to satisfy its owners who have put their capital in the business. See the sidebar ‘How much net profit is needed to make owners happy?’ in this chapter.

Nobody - not even the most die-hard humanitarian - is in business to make a zero EBIT. You simply can’t do this, because profit is an absolutely necessary part of doing business, and recouping the cost of capital is why profit is needed.

Don’t treat the word profit as something that’s whispered in the hallways. Profit builds owners’ value and provides the basic stability for a business. Earning a satisfactory EBIT is the cornerstone of business. Without earning an adequate operating profit, a business couldn’t attract capital, and you can’t have a business without capital.

How much net profit is needed to make owners happy?

People who invest in a business usually aren’t philanthropists who don’t want to make any money on the deal. No, these investors want a business to protect their capital investment, earn a good bottom-line profit for them and enhance the value of their investment over time. They understand that a business may not earn a profit but suffer a loss - that’s the risk they take as owners.

How much of a business’s net profit (bottom-line profit) is distributed to the owners depends on the business and the arrangement that it made with the owners. But regardless of how much money the owners actually receive, they still have certain expectations of how well the business will do - that is, what the business’s earnings before interest and tax will be. After all, they’ve staked their money on the business’s success.

One test of whether the owners will be satisfied with the net profit (after interest and tax) is to compute the return on equity (ROE), which is the ratio of net profit to total owners’ equity (net profit ÷ owners’ equity). In this chapter’s business example, the bottom-line profit is £1.9 million. Suppose that the total owners’ equity in the business is £15.9 million; thus the ROE is 12 per cent (£1.9 million ÷ £15.9 million). Is 12 per cent a good ROE? Well, that depends on how much the owners could earn from an alternative investment. We’d say that a 12 per cent ROE isn’t bad. By the way, ROE is also known as ROSI: return on shareholders’ investment.

Note: ROE doesn’t imply that all the net profit was distributed in cash to the owners. Usually, a business needs to retain a good part of its bottom-line net profit to provide capital for growing the business. Suppose, in this example, that none of the net profit is distributed in cash to its owners. The ROE is still 12 per cent; ROE doesn’t depend on how much, if any, of the net profit is distributed to the owners. (Of course, the owners may prefer that a good part of the net profit be distributed to them.)

Travelling Two Trails to Profit

How is the additional information in the management Profit and Loss statement useful? Well, with this information you can figure out how the business earned its profit for the year. We’re not referring to how the company decided which products to sell, and the best ways to market and advertise its products, and how to set sales prices, and how to design an efficient and smooth-running organisation, and how to motivate its employees, and all the other things every business has to do to achieve its financial goals. We’re talking about an accounting explanation of profit that focuses on methods for calculating profit - going from the basic input factors of sales price, sales volume and costs to arrive at the amount of profit that results from the interaction of the factors. Business managers should be familiar with these accounting calculations. They’re responsible for each factor and for profit, of course. With this in mind, therefore: how did the business earn its profit for the year?

First path to profit: Contribution margin minus fixed expenses

We can’t read your mind. But if we had to hazard a guess regarding how you’d go about answering the profit question, we’d bet that, after you had the chance to study Figure 3-2, you’d do something like the following, which is correct as a matter of fact:

|

Computing Profit Before Tax |

|

|

Contribution margin per unit |

£32 |

|

× Unit sales volume |

520,000 |

|

Equals: Total contribution margin |

£16,640,000 |

|

Less: Total fixed operating expenses |

£13,090,000 |

|

Equals: Operating profit (EBIT) |

£3,550,000 |

|

Less: Interest Expense |

£750,000 |

|

Equals: Earnings before tax |

£2,800,000 |

Note that we stop at the earnings before tax line in this calculation. You’re aware, of course, that business profit is subject to tax. This chapter focuses on profit above the taxation expense line.

Contribution margin is what’s left over after you subtract cost of goods sold expense and other variable expenses from sales revenue. On a per unit basis the business sells its product for £100, its variable product cost (cost of goods sold) is £60 and its variable operating cost per unit is £8 - which yields £32 contribution margin per unit. Total contribution margin for a period equals contribution margin per unit times the units sold during the period - in the business example, £32 × 520,000 units, which is £16.64 million total contribution margin. Total contribution margin is a measure of profit before fixed expenses are deducted. To pay for its fixed operating expenses and its interest expense, a business needs to earn a sufficient amount of total contribution margin. In the example, the business earned more total contribution margin than its fixed expenses, so it earned a profit for the year.

How variable expenses mow down your sales price

Consider a retail hardware store that sells, say, a lawnmower to a customer. The purchase cost per unit that the retailer paid to the lawnmower manufacturer when the retailer bought its shipment is the product cost in the contribution margin equation. The retailer also provides one free servicing of the lawnmower after the customer has used it for a few months (cleaning it and sharpening the blade) and also pays its salesperson a commission on the sale. These two additional expenses, for the service and the commission, are examples of variable expenses in the margin equation.

Here are some other concepts associated with the term margin that you’re likely to encounter:

· Gross margin, also called gross profit: Gross margin = sales revenue - cost of goods sold expense. Gross margin is profit from sales revenue before deducting the other variable expenses of making the sales. So gross margin is one step short of the final contribution margin earned on making sales. Businesses that sell products must report gross margin on their external Profit and Loss statements. However, generally accounting standards do not require that you report other variable expenses of making sales on external Profit and Loss statements. In their external financial reports, very few businesses divulge other variable expenses of making sales. In other words, managers don’t want the outside world and competitors to know their contribution margins. Most businesses carefully guard information about contribution margins because the information is very sensitive.

· Gross margin ratio: Gross margin ratio = gross margin ÷ sales revenue. In the business we use as an example in this chapter, the gross margin on sales is 40 per cent. Gross margins of companies vary from industry to industry, from over 50 per cent to under 25 per cent - but very few businesses can make a bottom-line profit with less than a 20 per cent gross margin.

· Markup: Generally refers to the amount added to the product cost to determine the sales price. For example, suppose a product that cost £60 is marked up (based on cost) by 662/3 per cent to determine its sales price of £100 - for a gross margin of £40 on the product. Note: The markup based on cost is 662/3 per cent (£40 markup ÷ £60 product cost). But the gross margin ratio is only 40 per cent, which is based on sales price (£40 ÷ £100).

Second path to profit: Excess over break-even volume × contribution margin per unit

The second method of computing a company’s profit starts with a particular sales volume as the point of reference. So, the first step is to compute this specific sales volume of the business (which isn’t its actual sales volume for the year) by dividing its total annual fixed expenses by its contribution margin per unit. Interest expense is treated as a fixed expense (because for all practical purposes it’s more or less fixed in amount over the short run). For the business in the example, the interest expense is £750,000 (see Figure 3-2), which, added to the £13.09 million fixed operating expenses, gives total fixed expenses of £13.84 million. The company’s break-even point, also called its break-even sales volume, is computed as follows:

· £13,840,000 total annual fixed expenses for year ÷ £32 contribution margin per unit = 432,500 units break-even point (or, break-even sales volume) for the year

In other words, if you multiply £32 contribution margin per unit by 432,500 units you get a total contribution margin of £13.84 million, which exactly equals the company’s total fixed expenses for the year. The business actually sold more than this number of units during the year, but if it had sold only 432,500 units, the company’s profit would have been exactly zero. Below this sales level the business suffers a loss, and above this sales level the business makes profit. The break-even sales volume is the crossover point from the loss column to the profit column. Of course, a business’s goal is to do better than just reaching its break-even sales volume.

Calculating its break-even point calls attention to the amount of fixed expenses hanging over a business. As explained earlier, a business is committed to its fixed expenses over the short run and can’t do much to avoid these costs - short of breaking some of its contracts and taking actions to downsize the business that could have disastrous long-run effects. Sometimes the total fixed expenses for the year are referred to as the ‘nut’ of the business - which may be a hard nut to crack (by exceeding its break-even sales volume).

In the example (see Figure 3-2) the business actually sold 520,000 units during the year, which is 87,500 units more than its break-even sales volume (520,000 units sold minus its 432,500 break-even sales volume). Therefore, you can determine the company’s earnings before tax as follows:

|

Second Way of Computing Profit |

|

|

Contribution margin per unit |

£32 |

|

× Units sold in excess of break-even point |

87,500 |

|

Equals: Earnings before tax |

£2,800,000 |

This second way of analysing profit calls attention to the need of the business to achieve and exceed its break-even point to make profit. The business makes no profit until it clears its break-even hurdle, but when over this level of sales it makes profit hand over fist because the units sold from here on aren’t burdened with any fixed costs, which have been covered by the first 432,500 units sold during the year. Be careful in thinking that only the last 87,500 units sold during the year generate all the profit for the year. The first 432,500 units sold are necessary to get the business into position in order for the next 87,500 units to make profit.

The key point is that when the business has reached its break-even sales volume (thereby covering its annual fixed expenses), each additional unit sold brings in pre-tax profit equal to the contribution margin per unit. Each additional unit sold brings in ‘pure profit’ of £32 per unit, which is the company’s contribution margin per unit. A business has to get into this upper region of sales volume to make a profit for the year.

The key point is that when the business has reached its break-even sales volume (thereby covering its annual fixed expenses), each additional unit sold brings in pre-tax profit equal to the contribution margin per unit. Each additional unit sold brings in ‘pure profit’ of £32 per unit, which is the company’s contribution margin per unit. A business has to get into this upper region of sales volume to make a profit for the year.

Calculating the margin of safety

The margin of safety is the excess of its actual sales volume over a company’s break-even sales volume. This business sold 520,000 units, which is 87,500 units above its break-even sales volume - a rather large cushion against any downturn in sales. Only a major sales collapse would cause the business to fall all the way down to its break-even point, assuming that it can maintain its £32 contribution margin per unit and that its fixed costs don’t change. You may wonder what a ‘normal’ margin of safety is for most businesses. Sorry, we can’t give you a definitive answer on this. Due to the nature of the business, or industry-wide problems, or due to conditions beyond its control, a business may have to operate with a smaller margin of safety than it would like.

Doing What-If Analysis

Managing profit is like driving a car - you need to be glancing in the rear-view mirror constantly as well as looking ahead through the windscreen. You have to know your profit history to see your profit future. Understanding the past is the best preparation for the future.

The model of a management Profit and Loss statement shown in Figure 3-2 allows you to compare your actual profit with what it would’ve looked like if you’d done something differently - for example, raised prices and sold fewer units. With the profit model, you can test-drive adjustments before putting them into effect. It lets you plan and map out your profit strategy for the coming period. Also, you can analyse why profit went up or down from the last period, using the model to do hindsight analysis.

The management Profit and Loss statement profit model focuses on the key factors and variables that drive profit. Here’s what you should know about these factors:

· Even a small decrease in the contribution margin per unit can have a drastic impact on profit because fixed expenses don’t go down over the short run (and may be hard to reduce even over the long run).

· Even a small increase in the contribution margin per unit can have a dramatic impact on profit because fixed expenses won’t go up over the short run - although they may have to be increased in the long run.

· Compared with changes in contribution margin per unit, sales volume changes have secondary profit impact; sales volume changes aren’t trivial, but even relatively small margin changes can have a bigger effect on profit.

· You can, perhaps, reduce fixed expenses to improve profit, but you have to be very careful to cut fat and not muscle; reducing fixed expenses may very well diminish the capacity of your business to make sales and deliver a high-quality service to customers.

The following sections expand on these key points.

Lower profit from lower sales - but that much lower?

The management Profit and Loss statement shown in Figure 3-2 is designed for managers to use in profit analysis - to expose the critical factors that drive profit. Remember what information has been added that isn’t included in the external Profit and Loss statement:

· Unit sales volume for the year

· Per-unit values

· Fixed versus variable operating expenses

· Contribution margin - total and per unit

Handle this information with care. The contribution margin per unit is confidential, for your eyes only. This information is limited to you and other managers in the business. Clearly, you don’t want your competitors to find out your margins. Even within a business, the information may not circulate to all managers - just those who need to know.

Handle this information with care. The contribution margin per unit is confidential, for your eyes only. This information is limited to you and other managers in the business. Clearly, you don’t want your competitors to find out your margins. Even within a business, the information may not circulate to all managers - just those who need to know.

The contribution margin per unit is one of the three most important determinants of profit performance, along with sales volume and fixed expenses - as shown in the upcoming sections.

With the information provided in the management Profit and Loss statement, you’re ready to paint a what-if scenario. We’re making you the chief executive officer of the business in this example. What if you’d sold 5 per cent fewer units during this period? In this example, that would mean you’d sold only 494,000 units rather than 520,000 units, or 26,000 units less. The following computation shows you how much profit damage this seemingly modest drop in sales volume would have caused.

|

Impact of 5 Per Cent Lower Sales Volume on Profit |

|

|

Contribution margin per unit |

£32 |

|

× 26,000 fewer units sold |

26,000 |

|

Equals: Decrease in earnings before tax |

£832,000 |

By selling 26,000 fewer units you missed out on the £832,000 profit that these units would have produced - this is fairly straightforward. What’s not so obvious, however, is that this £832,000 decrease in profit would have been a 30 per cent drop in profit: £832,000 decrease ÷ £2.8 million profit = 30 per cent decrease. Lose just 5 per cent of your sales and lose 30 per cent of your profit? How can such a thing happen? The next section expands on how a seemingly small decrease in sales volume can cause a stunning decrease in profit. Read on.

Violent profit swings due to operating leverage

First, the bare facts for the business in the example: the company’s contribution margin per unit is £32 and, before making any changes, the company sold 520,000 units during the year, which is 87,500 units in excess of its break-even sales volume. The company earned a total contribution margin of £16.64 million (see Figure 3-2), which is its contribution per unit times its total units sold during the year. If the company had sold 5 per cent less during the year (26,000 fewer units), you’d expect its total contribution margin to decrease 5 per cent, and you’d be absolutely correct - £832,000 decrease ÷ £16.64 million = 5 per cent decrease. Compared with its £2.8 million profit before tax, however, the £832,000 drop in total contribution margin equals a 30 per cent fall-off in profit.

The main focus of business managers and investors is on profit, which in this example is profit before tax. Therefore, the 30 per cent drop in profit would get more attention than the 5 per cent drop in total contribution margin. The much larger percentage change in profit caused by a relatively small change in sales volume is the effect of operating leverage. Leverage means that there’s a multiplier effect - that a relatively small percentage change in one factor can cause a much larger change in another factor. A small push can cause a large movement - this is the idea of leverage.

In the preceding scenario for the 5 per cent, 26,000 units decrease in sales volume, note that the 5 per cent is based on the total 520,000 units sales volume of the business. But if the 26,000 units decrease in sales volume is divided by the 87,500 units in excess of the company’s break-even point - which are the units that generate profit for the business - the sales volume decrease equals 30 per cent. In other words, the business lost 30 per cent of its profit layer of sales volume and, thus, the company’s profit would have dropped 30 per cent. This dramatic drop is caused by the operating leverage effect.

In the preceding scenario for the 5 per cent, 26,000 units decrease in sales volume, note that the 5 per cent is based on the total 520,000 units sales volume of the business. But if the 26,000 units decrease in sales volume is divided by the 87,500 units in excess of the company’s break-even point - which are the units that generate profit for the business - the sales volume decrease equals 30 per cent. In other words, the business lost 30 per cent of its profit layer of sales volume and, thus, the company’s profit would have dropped 30 per cent. This dramatic drop is caused by the operating leverage effect.

Note: If the company had sold 5 per cent more units, with no increase in its fixed expenses, its pre-tax profit would have increased by 30 per cent, reflecting the operating leverage effect. The 26,000 additional units sold at a £32 contribution margin per unit would increase its total contribution margin by £832,000, and this increase would increase profit by 30 per cent. You can see why businesses are always trying to increase sales volume.

Cutting sales price, even a little, can gut profit

So what effect would a 5 per cent decrease in the sales price have caused? Around a 30 per cent drop similar to the effect of a 5 per cent decrease in sales volume? Not quite. Check out the following computation for this 5 per cent sales price decrease scenario:

|

Impact of 5 Per Cent Lower Sales Price on Profit |

|

|

Contribution margin per unit decrease |

£4.60 |

|

× Units sold during year |

520,000 |

|

Equals: Decrease in earnings before tax |

£2,392,000 |

Hold on! Earnings before tax would drop from £2.8 million at the £100 sales price (refer to Figure 3-2) to only £408,000 at the £95 sales price - a plunge of 85 per cent. What could cause such a drastic dive in profit?

The sales price drops £5 per unit - a 5 per cent decrease of the £100 sales price. But contribution margin per unit doesn’t drop by the entire £5 because the variable operating expense per unit (sales commissions in this example) would also drop 5 per cent, or £40 per unit - for a net decrease of £4.60 per unit in the contribution margin per unit. (This is one reason for identifying the expenses that depend on sales revenue - as shown in the management Profit and Loss statement in Figure 3-2.) For this what-if scenario that examines the case of the company selling all units at a 5 per cent lower sales price than it did, the company’s contribution margin would have been only £27.40 per unit. Such a serious reduction in its contribution margin per unit would have been intolerable.

At the lower sales price, the company’s contribution margin would be £27.40 per unit (£32.00 in the original example minus the £4.60 decrease = £27.40). As a result, the break-even sales volume would be much higher, and the company’s 520,000 sales volume for the year would have been only 14,891 units over its break-even point. So the lower £27.40 contribution margin per unit would yield only £408,000 profit before tax.

The moral of the story is to protect contribution margin per unit above all else. Every pound of contribution margin per unit that’s lost - due to decreased sales prices, increased product cost or increases in other variable costs - has a tremendously negative impact on profit. Conversely, if you can increase the contribution margin per unit without hurting sales volume, you reap very large profit benefits, as described next.

Improving profit

The preceding sections explore the downside of things - that is, what would’ve happened to profit if sales volume or sales prices had been lower. The upside - higher profit - is so much more pleasant to discuss and analyse, don’t you think?

Profit improvement boils down to the three critical profit-making factors, listed in order from the most effective to the least effective:

· Increasing the contribution margin per unit

· Increasing sales volume

· Reducing fixed expenses

Say you want to improve your bottom-line profit from the £1.9 million net profit you earned the year just ended to £2.1 million next year. How can you pump up your net profit by £210,000? (By the way, this is the only place in the chapter we bring the tax factor into the analysis.)

First of all, realise that to increase your net profit after taxes by £210,000, you need to increase your before-tax profit by much more - to provide for the amount that goes to tax. Your accountant calculates that you would need a £312,000 increase in earnings before tax next year because your tax increase would be about £102,000 on the £312,000 increase in pre-tax earnings. So you have to find a way to increase earnings, before tax, by £312,000.

You should also take into account the possibility that fixed costs and interest expense may rise next year, but for this example we’re assuming that they won’t. We’re also assuming that the business can’t cut any of its fixed operating expenses without hurting its ability to maintain and support its present sales level (and a modest increase in the sales level). Of course, in real life every business should carefully scrutinise its fixed expenses to see whether some of them can be cut.

· Increase your contribution margin per unit by £0.60, which would raise the total contribution margin by £312,000, based on a 520,000 units sales volume (£0.60 × 520,000 = £312,000).

· Sell 9,750 additional units at the current contribution margin per unit of £32, which would raise the total contribution margin by £312,000 (9,750 × £32 = £312,000).

· Use a combination of these two approaches: increase both the margin per unit and the sales volume.

The second approach is obvious - you just need to set a sales goal of increasing the number of products sold by 9,750 units. (How you motivate your already overworked sales staff to accomplish that sales volume goal is up to you.) But how do you go about the first approach, increasing the contribution margin per unit by £0.60?

The simplest way to increase contribution margin per unit by £0.60 would be to decrease your product cost per unit by £0.60. Or you could attempt to reduce sales commissions from £8 per £100 of sales to £7.40 per £100 - which may adversely affect the motivation of your sales force, of course. Or you could raise the sales price by about £0.65 (remember that 8 per cent comes off the top for the sales commission, so only £0.60 would remain from that £0.65 to improve the unit contribution margin). Or you could combine two or more such changes so that your unit contribution next year would increase by £0.60. However you do it, the improvement would increase your earnings before tax by the desired amount:

|

Impact of £0.60 Higher Unit Contribution Margin on Profit |

|

|

Contribution margin per unit increase |

£0.60 |

|

× Units sold during year |

520,000 |

|

Equals: Increase in earnings before tax |

£312,000 |

Cutting prices to increase sales volume: A very tricky game to play!

A word of warning: be sure to run the numbers (accountant speak for using a profit model) before deciding to drop sales prices in an effort to gain more sales volume. Suppose, for example, you’re convinced that if you decrease sales prices by 5 per cent, your sales volume will increase by 10 per cent. Seems like an attractive trade-off, one that would increase both profit performance and market share. But are you sure that those positive changes are the results you’ll get?

The impact on profit may surprise you. Get a piece of notepaper and do the computation for this lower sales price and higher sales volume scenario:

|

Lower Sales Price and Higher Sales Volume Impact on Profit |

|

|

New sales price (lower) |

£95.00 |

|

Less: Product cost per unit (same) |

£60.00 |

|

Less: Variable operating expenses (lower) |

£7.60 |

|

Equals: New unit contribution margin (lower) |

£27.40 |

|

× Sales volume (higher) |

572,000 |

|

Equals: Total contribution margin |

£15,672,800 |

|

Less: Previous total contribution margin |

£16,640,000 |

|

Equals: Decrease in total contribution margin |

£967,200 |

Your total contribution margin wouldn’t go up; instead, it would go down by £967,200! In dropping the sales price by £5, you’d give up too much of your contribution margin per unit. The increase in sales volume wouldn’t make up for the big dent in unit contribution margin. You may gain more market share, but would pay for it with a £967,200 drop in earnings before tax.

To keep profit the same, you’d have to increase sales volume more than 10 per cent. By how much? Divide the total contribution margin for the 520,000 units situation by the contribution margin per unit for the new scenario:

· £16,640,000 ÷ £27.40 = 607,300 units

In other words, just to keep your total contribution margin the same at the lower sales price, you’d have to increase sales volume to 607,300 units - an increase of 87,300 units, or a whopping 17 per cent. That would be quite a challenge, to say the least.

Cash flow from improving profit margin versus improving sales volume

This chapter discusses increasing profit margin versus increasing sales volume to improve bottom-line profit. Improving your profit margin is the better way to go, compared with increasing sales volume. Both actions increase profit, but the profit margin tactic is much better in terms of cash flow. When sales volume increases, so does stock. On the other hand, when you improve profit margin (by raising the sales price or by lowering product cost), you don’t have to increase stock - in fact, reducing product cost may actually cause stock to decrease a little. In short, increasing your profit margin yields a higher cash flow from profit than does increasing your sales volume.

A Final Word or Two

Recently, some friends pooled their capital and opened an up-market off-licence in a rapidly growing area. The business has a lot of promise. We can tell you one thing they should have done before going ahead with this new venture - in addition to location analysis and competition analysis, of course. They should have used the basic profit model (in other words, the management Profit and Loss statement) discussed in this chapter to figure out their break-even sales volume - because we’re sure they have rather large fixed expenses. And they should have determined how much more sales revenue over their break-even point that they’ll need to earn a satisfactory return on their investment in the business.

During their open house for the new shop we noticed the very large number of different beers, wines and spirits available for sale - to say nothing of the different sizes and types of containers many products come in. Quite literally, the business sells thousands of distinct products. The shop also sells many products like soft drinks, ice, corkscrews and so on. Therefore, the company doesn’t have a single sales volume factor (meaning the number of units sold) to work with in the basic profit model. So you have to adapt the profit model to get along without the sales volume factor.

The trick is to determine your average contribution margin as a percentage of sales revenue. We’d estimate that an off-licence’s average gross margin (sales revenue less cost of goods sold) is about 25 per cent. The other variable operating expenses of the shop probably run about 5 per cent of sales. So the average contribution margin would be 20 per cent of sales (25 per cent gross margin less 5 per cent variable operating expenses). Suppose the total fixed operating expenses of the shop are about £100,000 per month (for rent, salaries, electricity and so on), which is £1.2 million per year. So the shop needs £6 million in sales per year just to break even:

· £1.2 million fixed expenses ÷ 20% average contribution margin = £6 million annual sales to break even

Selling £6 million of product a year means moving a lot of booze. The business needs to sell another £1 million to provide £200,000 of operating earnings (at the 20 per cent average contribution margin) - to pay interest expense and tax and to leave enough net profit for the owners who invested capital in the business and who expect a good return on their investment.

By the way, some disreputable off-licence owners are known (especially to HM Revenue & Customs) to engage in sales skimming. This term refers to not recording all sales revenue; instead, some cash collected from customers is put in the pockets of the owners. They don’t report the profit in their tax returns or in the Profit and Loss statements of the business. Our friends who started the off-licence are honest businesspeople, and we’re sure they won’t engage in sales skimming - but they do have to make sure that none of their store’s employees skim off some sales revenue.

When sales skimming is being committed, not all the actual sales revenue for the year is recorded, even though the total cost of all products sold during the year is recorded. Obviously, this distorts the Profit and Loss statement and throws off normal ratios of gross profit and operating profit to sales revenue. If you have the opportunity to buy a business, please be alert to the possibility that some sales skimming may have been done by the present owner. Indeed, we’ve been involved in situations in which the person selling the business bragged about how much he was skimming off the top.

Have a Go

1. Using the information shown in Table 3-1, calculate the contribution Margin for Company A.

2. Using the information shown in Table 3-1, calculate the break-even point for Company B.

3. Using the information in Table 3-1, calculate the margin of safety for Company A.

4. Using the information in Table 3-1, calculate the gross margin ration of Company B.

Table 3-1 Internal Profit and Loss Statement Highlighting Profit Drivers

|

Company A |

Company B |

|||

|

Totals |

Per Unit |

Totals |

Per Unit |

|

|

Sales volume (units) |

50,000 |

1,500,000 |

||

|

Sales revenue |

£15,000,000 |

£300.00 |

£36,000,000 |

£24.00 |

|

Cost of goods sold expense |

£7,500,000 |

£150.00 |

£27,000,000 |

£18.00 |

|

Gross margin |

£7,500,000 |

£150.00 |

£9,000,000 |

£6.00 |

|

Variable operating expenses |

£3,750,000 |

£75.00 |

£4,200,000 |

£2.80 |

|

Contribution margin |

£3,750,000 |

£75.00 |

£4,800,000 |

£3.20 |

|

Fixed operating expenses |

£1,950,000 |

£39.00 |

£3,000,000 |

£2.00 |

|

Operating profit |

£1,800,000 |

£36.00 |

£1,800,000 |

£1.20 |

5. Using the information shown in Table 3-2, calculate the effect of Company C allowing a 10 per cent decrease in its selling price, in exchange for a 10 per cent increase in sales volume. What is the effect on the operating profit?

Table 3-2 Operating Profit Result from 10 per cent Sales Price Decrease in Exchange for 10 per cent Sales Volume Increase

|

Company C |

||||

|

Before |

After |

Calculate Change |

||

|

Sales price |

£300.00 |

£270.00 |

?? |

|

|

Product cost |

£150.00 |

£150.00 |

||

|

Variable operating expenses: |

£15.00 |

£15.00 |

?? |

|

|

Volume driven expenses |

£60.00 |

£54.00 |

||

|

Revenue driven expenses at 20 per cent |

||||

|

Contribution margin per unit |

£75.00 |

£51.00 |

? |

|

|

Times sales volume in units |

50,000 |

55,000 |

? |

|

|

Equals total contribution margin |

£3,750,000 |

£2,805,000 |

? |

|

|

Less fixed operating expenses |

£1,950,000 |

£1,950,000 |

||

|

Operating profit |

£1,800,000 |

£855,000 |

? |

|

Answering the Have a Go Questions

1. You calculate the contribution margin by multiplying the contribution per unit by the volume of units sold. So in the case of Company A, you do this:

· Contribution per unit = £75

· Volume sold = 50,000 units

· Contribution margin = £75 × 50,000 = £3,750,000

2. You calculate the break-even point by taking the total annual fixed expenses and dividing them by the contribution margin per unit. For Company B, the calculation is as follows:

· Total fixed expenses = £3,000,000

· Contribution per unit = £3.20

· Break-even point = 3,000,000 ÷ £3.20 = 937,500 units

3. The margin of safety is described as the volume of sales units minus the break even number of units. In the case of Company A the calculation is as follows:

· Sales volume = 50,000 units

· Break-even volume = 26,000 (1,950,000 ÷ £75)

· Margin of safety = 50,000 - 26,000 = 24,000 units

4. You calculate the gross margin ratio by dividing the gross margin by the sales revenue and multiplying by 100. So in the case of Company B, the calculation is as follows:

· Gross margin = 9,000,000

· Sales revenue = £36,000,000

· Gross margin ratio = 9,000,000 ÷ 36,000,000 × 100 = 25%

5. Table 3-3 shows the completed Table 3-2.

You can see that the operating profit decreases by £945,000, which is a decrease of more than 50 per cent prior to decreasing the selling price! The reason for this huge drop isn’t immediately obvious, but here goes… . The 10 per cent decrease in the sales prices causes the contribution margin per unit to drop from £75 to £51, which is a plunge of 32 per cent (£24 decrease divided by £75 original contribution margin). The small 10 per cent increase in sales volume can’t make up for the 32 per cent decrease in contribution margin.

Table 3-3 Operating Profit Result - Completed

|

Company C |

|||

|

Before |

After |

Change |

|

|

Sales price |

£300.00 |

£270.00 |

(£30.00) |

|

Product cost |

£150.00 |

£150.00 |

|

|

Variable operating expenses: |

£15.00 |

£15.00 |

(£6.00) |

|

Volume driven expenses |

£60.00 |

£54.00 |

|

|

Revenue driven expenses at 20 per cent |

|||

|

Contribution margin per unit |

£75.00 |

£51.00 |

(£24.00) |

|

Times sales volume in units |

50,000 |

55,000 |

5,000 |

|

Equals total contribution margin |

£3,750,000 |

£2,805,000 |

(£945,000) |

|

Less fixed operating expenses |

£1,950,000 |

£1,950,000 |

|

|

Operating profit |

£1,800,000 |

£855,000 |

(£945,000) |