Bookkeeping & Accounting All-in-One For Dummies (2015)

Book V

Accountants: Managing the Business

Chapter 2

Choosing Accounting Methods

In This Chapter

![]() Having a choice of accounting methods

Having a choice of accounting methods

![]() Understanding the alternatives for calculating cost of goods sold expense and stock cost

Understanding the alternatives for calculating cost of goods sold expense and stock cost

![]() Dealing with depreciation

Dealing with depreciation

![]() Writing down stock and debtors

Writing down stock and debtors

![]() Keeping two sets of books

Keeping two sets of books

Some people put a great deal of faith in numbers: 2 + 2 = 4, and that’s the end of the story. They see a number reported to the last digit on an accounting report, and they get the impression of exactitude. But accounting isn’t just a matter of adding up numbers. It’s not an exact science.

Accountants do have plenty of rules that they must follow. The official rule book of generally accepted accounting principles laid down by the Accounting Standards Board (and its predecessors) is more than 1,200 pages long and growing fast. In addition there are the rules and regulations issued by the various government regulatory agencies that govern financial reporting and accounting methods, and those issued by publicly owned companies such as the London Stock Exchange. The Institute of Chartered Accountants and the other professional accountancy institutes play a role in setting accounting standards. And accounting standards have now gone international: with the advent of the European Union and the ever‐increasing amount of international trade and investing, business and political leaders in many nations recognise the need to iron out differences in accounting methods and disclosure standards from country to country. The International Accounting Standards Board (IASB) is an independent, private sector body that develops and approves International Financial Reporting Standards under the oversight of the IFRS Foundation (www.IFRS.org).

Perhaps the most surprising thing - considering that formal rule‐making activity has been going on since the 1930s - is that a business still has options for choosing among alternative accounting methods. Different methods lead to inconsistent profit measures from company to company. The often‐repeated goal for standardising accounting methods is to make like things look alike and different things look different - but the accounting profession hasn’t reached this stage of nirvana yet. In addition, accounting methods change over the years, as the business world changes. Accounting rules too are, to one degree or another, in a state of flux.

Perhaps the most surprising thing - considering that formal rule‐making activity has been going on since the 1930s - is that a business still has options for choosing among alternative accounting methods. Different methods lead to inconsistent profit measures from company to company. The often‐repeated goal for standardising accounting methods is to make like things look alike and different things look different - but the accounting profession hasn’t reached this stage of nirvana yet. In addition, accounting methods change over the years, as the business world changes. Accounting rules too are, to one degree or another, in a state of flux.

Because the choice of accounting methods directly affects the profit figure for the year and the values reported in the ending Balance Sheet, business managers (and investors) need to know the difference between accounting methods. You don’t need to probe into these accounting methods in excruciating, technical detail, but you should at least know whether one method versus another yields higher or lower profit measures and higher or lower asset values in financial statements. This chapter explains accounting choices for measuring cost of goods sold, depreciation and other expenses. Get involved in making these important accounting decisions - it’s your business, after all.

Decision‐Making Behind the Scenes in Profit and Loss Statements

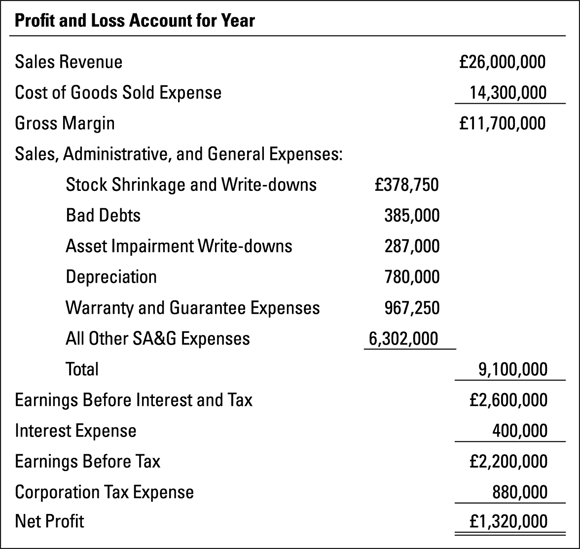

Book IV, Chapter 1 introduces the simplified UK format for presenting Profit and Loss statements. (We also discuss this in Book V, Chapter 3, where we look at managing profit performance.) Figure 2‐1 presents another Profit and Loss statement for a business - with certain modifications that you won’t see in actual external Profit and Loss statements. For explaining the choices between alternative accounting methods, certain specific expenses are broken down under the company’s sales, administrative and general expenses (SA&G) category in Figure 2‐1. Of these particular expenses, only depreciation is disclosed in external Profit and Loss statements. Don’t expect to find in external Profit and Loss statements the other expenses shown under the SA&G category in Figure 2‐1. Businesses are very reluctant to divulge such information to the outside world.

Figure 2-1: A Profit and Loss statement including certain expenses that aren’t reported outside the business.

Here’s a quick overview of the accounting matters and choices relating to each line in the Profit and Loss statement shown in Figure 2‐1, from the top line to the bottom line:

· Sales revenue: Timing the recording of sales is something to be aware of. Generally speaking, sales revenue timing isn’t a serious accounting problem, but businesses should be consistent from one year to the next. However, for some businesses- such as software and other high‐tech companies, and companies in their early start‐up phases - the timing of recording sales revenue is a major problem. A footnote to the company’s financial statements should explain its revenue recognition method if there’s anything unusual about it.

Note: If products are returnable and the deal between the seller and buyer doesn’t satisfy normal conditions for a completed sale, then recognition of sales revenue should be postponed until the return privilege no longer exists. For example, some products are sold on approval, which means the customer takes the product and tries it out for a few days or longer to see whether she really wants it. This area is increasingly significant with the continuing rapid growth of the Internet as a medium for selling. In response, the UK introduced the Distance Selling Regulations in October 2001. These regulations give consumers additional rights to obtain full refunds on goods bought over the Internet and through mail order without having to give a reason for doing so.

· Cost of goods sold expense: Whether to use the first‐in, first‐out (FIFO) method, or the last‐in, first‐out (LIFO) method, or the average cost method (each of which is explained in the section ‘Calculating Cost of Goods Sold and Cost of Stock’, later in this chapter), cost of goods sold is a big expense for companies that sell products and naturally the choice of method can have a real impact.

· Gross margin: Can be dramatically affected by the method used for calculating cost of goods sold expense (and the method of revenue recognition, if this is a problem).

· Stock write‐downs: Whether to count and inspect stock very carefully to determine loss due to theft, damage and deterioration, and whether to apply the net realisable value (NRV) method strictly or loosely are the two main questions that need to be answered. See ‘Identifying Stock Losses: Net Realisable Value (NRV)’, later in this chapter. Stock is a high‐risk asset that’s subject to theft, damage and obsolescence.

· Bad debts expense: When to conclude that the debts owed to you by customers who bought on credit (debtors) aren’t going to be paid - the question is really when to write down these debts (that is, remove the amounts from your asset column). You can wait until after you’ve made a substantial effort to collect the debts, or you can make your decision before that time. See ‘Collecting or Writing Off Bad Debts’, later in this chapter.

· Asset impairment write‐downs: Whether (and when) to write down or write off an asset - that is, remove it from the asset column. Stock shrinkage, bad debts and depreciation by their very nature are asset write‐downs. Other asset write‐downs are required when any asset becomes impaired, which means that it has lost some or all of its economic utility to the business and has little or no disposable value. An asset write‐down reduces the book (recorded) value of an asset (and at the same time records an expense or loss of the same amount). A write‐off reduces the asset’s book value to zero and removes it from the accounts, and the entire amount becomes an expense or loss.

For example, your delivery van driver had an accident. The repair of the van was covered by insurance, so no write‐down is necessary. But the products being delivered had to be thrown away and weren’t insured while in transit. You write off the cost of the stock lost in the accident.

For example, your delivery van driver had an accident. The repair of the van was covered by insurance, so no write‐down is necessary. But the products being delivered had to be thrown away and weren’t insured while in transit. You write off the cost of the stock lost in the accident.

· Depreciation expense: Whether to use a short‐life method and load most of the expense over the first few years, or a longer‐life method and spread the expense evenly over the years. Refer to ‘Appreciating Depreciation Methods’, later in this chapter. Depreciation is a big expense for some businesses, making the choice of method even more important.

· Warranty and guarantee (post‐sales) expenses: Whether to record an expense for products sold with warranties and guarantees in the same period that the goods are sold (along with the cost of goods sold expense, of course) or later, when customers actually return products for repair or replacement. Businesses can usually forecast the percentage of products sold that will be returned for repair or replacement under the guarantees and warranties offered to customers - although a new product with no track record can be a problem in this regard.

· All other SA&G expenses: This is the catch‐all ‘other expenses’ line that you use if you can’t categorise the item into any of the preceding items. Obviously, the expense has to relate to selling, admin or general expense types.

· Earnings before interest and tax (EBIT): This profit measure equals sales revenue less all the expenses above this line; therefore, EBIT depends on the particular choices made for recording sales revenue and expenses. Having a choice of accounting methods means that an amount of wriggle is inherent in recording sales revenue and many expenses. How much wriggle effect do all these accounting choices have on the EBIT profit figure? This is a very difficult question to answer. The business itself may not know. We would guess (and it’s no more than a conjecture on our part) that the EBIT for a period reported by most businesses could easily be 10-20 per cent lower or higher if different accounting choices had been made.

· Interest expense: Usually a cut‐and‐dried calculation, with no accounting problems. (Well, we can think of some really hairy interest accounting problems, but we won’t go into them here.)

·  Corporation tax expense: You can use different accounting methods for some of the expenses reported in your Profit and Loss statement than you use for calculating taxable income. Oh, crikey! The hypothetical amount of taxable income, if the accounting methods used in the Profit and Loss statement were used in the tax return, is calculated; then the corporation tax based on this hypothetical taxable income is figured. This is the corporation tax expense reported in the Profit and Loss statement. This amount is reconciled with the actual amount of corporation tax owed based on the accounting methods used for tax purposes. A reconciliation of the two different tax amounts is provided in a rather technical footnote to the financial statements. See ‘Reconciling Corporation Tax’, later in this chapter.

Corporation tax expense: You can use different accounting methods for some of the expenses reported in your Profit and Loss statement than you use for calculating taxable income. Oh, crikey! The hypothetical amount of taxable income, if the accounting methods used in the Profit and Loss statement were used in the tax return, is calculated; then the corporation tax based on this hypothetical taxable income is figured. This is the corporation tax expense reported in the Profit and Loss statement. This amount is reconciled with the actual amount of corporation tax owed based on the accounting methods used for tax purposes. A reconciliation of the two different tax amounts is provided in a rather technical footnote to the financial statements. See ‘Reconciling Corporation Tax’, later in this chapter.

· Net profit: Like EBIT, this can vary considerably depending on which accounting methods you use for measuring expenses. (See also Book VI, Chapter 1 on profit smoothing, which crosses the line from choosing acceptable accounting methods into the grey area of ‘earnings management’ through means of accounting manipulation.)

Whereas bad debts, post‐sales expenses and asset write‐downs vary in importance from business to business, cost of goods sold and depreciation methods are so important that a business must disclose which methods it uses for these two expenses in the footnotes to its financial statements. (Book VI, Chapter 1 explains footnotes to financial statements.) HM Revenue & Customs requires that a company actually records in its cost of goods sold expense and stock asset accounts the amounts determined by the accounting method it uses to determine taxable income - a rare requirement in company tax law.

Considering how important the bottom‐line profit number is, and that different accounting methods can cause a major difference in this all‐important number, you’d think that accountants would have developed clear‐cut and definite rules so that only one accounting method would be correct for a given set of facts. No such luck. The final choice boils down to an arbitrary decision, made by top‐level accountants in consultation with, and with the consent of, managers. If you own a business or are a manager in a business, we strongly encourage you to get involved in choosing which accounting methods to use for measuring your profit and for presenting your Balance Sheet. Accounting methods vary from business to business more than you’d probably suspect, even though all of them stay within the boundaries of acceptable practice. The rest of this chapter expands on the methods available for measuring certain expenses. Sales revenue accounting can be a challenge as well, but profit accounting problems lie mostly on the expense side of the ledger.

Calculating Cost of Goods Sold and Cost of Stock

One main accounting problem of companies that sell products is how to measure their cost of goods sold expense, which is the sum of the costs of the products sold to customers during the period. You deduct cost of goods sold from sales revenue to determine gross margin - the first profit line on the Profit and Loss statement (see Book IV, Chapter 1 for more about Profit and Loss statements, and Figure 1-1 there for a typical Profit and Loss statement). Cost of goods sold is therefore a very important figure, because if gross margin is wrong, bottom‐line profit (net profit) is wrong.

First a business acquires products, either by buying them (retailers) or by producing them (manufacturers). Book V, Chapter 4 explains how manufacturers determine product cost; for retailers product cost is simply the purchase cost. (Well, it’s not entirely this simple, but you get the point.) Product cost is entered in the stock asset account and is held there until the products are sold. Then, but not before, product cost is taken out of stock and recorded in the cost of goods sold expense account.

First a business acquires products, either by buying them (retailers) or by producing them (manufacturers). Book V, Chapter 4 explains how manufacturers determine product cost; for retailers product cost is simply the purchase cost. (Well, it’s not entirely this simple, but you get the point.) Product cost is entered in the stock asset account and is held there until the products are sold. Then, but not before, product cost is taken out of stock and recorded in the cost of goods sold expense account.

You must be absolutely clear on this point. Suppose that you clear £700 from your salary for the week and deposit this amount in your bank account. The money stays in there and is an asset until you spend it. You don’t have an expense until you write a cheque. Likewise, not until the business sells products does it have a cost of goods sold expense. When you write a cheque, you know how much it’s for - you have no doubt about the amount of the expense. But when a business withdraws products from its stock and records cost of goods sold expense, the expense amount is in some doubt. The amount of expense depends on which accounting method the business selects.

The essence of this accounting issue is that you have to divide the total cost of your stock between the units sold (cost of goods sold expense, in the Profit and Loss statement) and the unsold units that remain on hand waiting to be sold next period (stock asset, in the Balance Sheet).

The essence of this accounting issue is that you have to divide the total cost of your stock between the units sold (cost of goods sold expense, in the Profit and Loss statement) and the unsold units that remain on hand waiting to be sold next period (stock asset, in the Balance Sheet).

For example, say you own a shop that sells antiques. Every time an item sells, you need to transfer the amount you paid for the item from the stock asset account into the cost of goods sold expense account. At the start of a fiscal period, your cost of goods sold expense is zero, and if you own a medium‐sized shop selling medium‐quality antiques, your stock asset account may be £20,000. Over the course of the fiscal period, your cost of goods sold expense should increase (hopefully rapidly, as you make many sales).

You probably want your stock asset account to remain fairly static, however. If you paid £200 for a wardrobe that sells during the period, the £200 leaves the stock asset account and finds a new home in the cost of goods sold expense account. However, you probably want to turn around and replace the item you sold, ultimately keeping your stock asset account at around the same level - although more complicated businesses have more complicated strategies for dealing with stock and more perplexing accounting problems.

You have three methods to choose from when you measure cost of goods sold and stock costs: You can follow a first‐in, first‐out (FIFO) cost sequence, follow a last‐in, first‐out cost sequence (LIFO), or compromise between the two methods and take the average costs for the period. Other methods are acceptable, but these three are the primary options.

Product costs are entered in the stock asset account in the order acquired, but they’re not necessarily taken out of the stock asset account in this order. The different methods refer to the order in which product costs are taken out of the stock asset account. You may think that only one method is appropriate - that the sequence in should be the sequence out. However, generally accepted accounting principles permit other methods.

In reality, the choice boils down to FIFO versus LIFO; the average cost method runs a distant third in popularity. If you want our opinion, FIFO is better than LIFO for reasons that we explain in the next two sections. You may not agree, and that’s your right. For your business, you make the call.

In reality, the choice boils down to FIFO versus LIFO; the average cost method runs a distant third in popularity. If you want our opinion, FIFO is better than LIFO for reasons that we explain in the next two sections. You may not agree, and that’s your right. For your business, you make the call.

The FIFO method

With the FIFO method, you charge out product costs to cost of goods sold expense in the chronological order in which you acquired the goods. The procedure is that simple. It’s like the first people in line to see a film get in the cinema first. The usher collects the tickets in the order in which they were bought.

We think that FIFO is the best method for both the expense and the asset amounts. We hope that you like this method, but also look at the LIFO method before making up your mind. You should make up your mind, you know. Don’t just sit on the sidelines. Take a stand.

Suppose that you acquire four units of a product during a period, one unit at a time, with unit costs as follows (in the order in which you acquire the items): £100, £102, £104 and £106. By the end of the period, you’ve sold three of those units. Using FIFO, you calculate the cost of goods sold expense as follows:

· £100 + £102 + £104 = £306

In short, you use the first three units to calculate the cost of goods sold expense. (You can see the benefit of having such a standard method if you sell hundreds or thousands of different products.)

The ending stock asset, then, is £106, which is the cost of the most recent acquisition. The £412 total cost of the four units is divided between the £306 cost of goods sold expense for the three units sold and the £106 cost of the one unit in ending stock. The total cost has been taken care of; nothing fell between the cracks.

FIFO works well for two reasons:

· In most businesses, products actually move into and out of stock in a FIFO sequence: the earlier acquired products are delivered to customers before the later acquired products are delivered, so the most recently purchased products are the ones still in ending stock to be delivered in the future. Using FIFO, the stock asset reported on the Balance Sheet at the end of the period reflects the most recent purchase cost and therefore is close to the current replacement cost of the product.

· When product costs are steadily increasing, many (but not all) businesses follow a FIFO sales price strategy and hold off on raising sales prices as long as possible. They delay raising sales prices until they’ve sold all lower‐cost products. Only when they start selling from the next batch of products, acquired at a higher cost, do they raise sales prices. We strongly favour using the FIFO cost of goods sold expense method when the business follows this basic sales pricing policy because both the expense and the sales revenue are better matched for determining gross margin.

The LIFO method

Remember the cinema usher we mentioned earlier? Think about that usher going to the back of the line of people waiting to get into the next showing and letting them in from the rear of the line first. In other words, the later you bought your ticket, the sooner you get into the cinema. This is the LIFO method, which stands for last‐in, first‐out. The people in the front of the queue wouldn’t stand for it, of course, but the LIFO method is quite acceptable for determining the cost of goods sold expense for products sold during the period. The main feature of the LIFO method is that it selects the last item you purchased first and then works backward until you have the total cost for the total number of units sold during the period. What about the ending stock, the products you haven’t sold by the end of the year? Using the LIFO method, you never get back to the cost of the first products acquired (unless you sold out your entire stock); the earliest cost remains in the stock asset account.

Using the same example from the preceding section, assume that the business uses the LIFO method instead of FIFO. The four units, in order of acquisition, had costs of £100, £102, £104 and £106. If you sell three units during the period, LIFO gives you the following cost of goods sold expense:

· £106 + £104 + £102 = £312

The ending stock cost of the one unit not sold is £100, which is the oldest cost. The £412 total cost of the four units acquired less the £312 cost of goods sold expense leaves £100 in the stock asset account. Determining which units you actually delivered to customers is irrelevant; when you use the LIFO method, you always count backward from the last unit you acquired.

If you really want to argue in favour of using LIFO - and we have to tell you that we won’t back you up on this one - here’s what you can say:

· Assigning the most recent costs of products purchased to the cost of goods sold expense makes sense because you have to replace your products to stay in business and the most recent costs are closest to the amount you’ll have to pay to replace your products. Ideally, you should base your sales prices not on original cost but on the cost of replacing the units sold.

· During times of rising costs, the most recent purchase cost maximises the cost of goods sold expense deduction for determining taxable income, and thus minimises the taxable income. In fact, LIFO was invented for income tax purposes. True, the cost of stock on the ending Balance Sheet is lower than recent acquisition costs, but the Profit and Loss statement effect is more important than the Balance Sheet effect.

The more product cost you take out of the stock asset to charge to cost of goods sold expense, the less product cost you have in the ending stock. In maximising cost of goods sold expense, you minimise the stock cost value.

But here are the reasons why LIFO, in our view, is usually the wrong choice (the following sections of this chapter go into more details about these issues):

· Unless you base your sales prices on the most recent purchase costs or you raise sales prices as soon as replacement costs increase - and most businesses don’t follow either of these pricing policies - using LIFO depresses your gross margin and, therefore, your bottom‐line net profit.

· The LIFO method can result in an ending stock cost value that’s seriously out‐of‐date, especially if the business sells products that have very long lives.

· Unscrupulous managers can use the LIFO method to manipulate their profit figures if business isn’t going well. Refer to ‘Manipulating LIFO stock levels to give profit a boost’, later in the chapter.

Note: In periods of rising product costs, it’s true that FIFO results in higher taxable income than LIFO does - something you probably want to avoid, we’re sure. Nevertheless, even though LIFO may be preferable in some circumstances, we still say that FIFO is the better choice in the majority of situations, for the reasons discussed earlier, and you may come over to our way of thinking after reading the following sections. By the way, if the products are intermingled such that they can’t be identified with particular purchases, then the business has to use FIFO for its income tax returns.

The greying of LIFO stock cost

If you sell products that have long lives and for which your product costs rise steadily over the years, using the LIFO method has a serious impact on the ending stock cost value reported on the Balance Sheet and can cause the Balance Sheet to look misleading. Over time, the cost of replacing products becomes further and further removed from the LIFO‐based stock costs. Your 2014 Balance Sheet may very well report stock based on 1985, 1975 or 1965 product costs. As a matter of fact, the product costs used to value stock can go back even further.

Suppose that a major manufacturing business has been using LIFO for more than 45 years. The products that this business manufactures and sells have very long lives - in fact, the business has been making and selling many of the same products for many years. Believe it or not, the difference between its LIFO and FIFO cost values for its ending stock is about £2 billion because some of the products are based on costs going back to the 1950s, when the company first started using the LIFO method. The FIFO cost value of its ending stock is disclosed in a footnote to its financial statements; this disclosure is how you can tell the difference between a business’s LIFO and FIFO cost values. The gross margin (before income tax) over the business’s 45 years would have been £2 billion higher if the business had used the FIFO method - and its total taxable income over the 45 years would have been this much higher as well.

Of course, the business’s income taxes over the years would have been correspondingly higher as well. That’s the trade‐off.

Note: A business must disclose the difference between its stock cost value according to LIFO and its stock cost value according to FIFO in a footnote on its financial statements - but, of course, not too many people outside of stock analysts and professional investment managers read footnotes. Business managers get involved in reviewing footnotes in the final steps of getting annual financial reports ready for release (refer to Book VI, Chapter 1). If your business uses FIFO, your ending stock is stated at recent acquisition costs, and you don’t have to determine what the LIFO value may have been. Annual financial reports don’t disclose the estimated LIFO cost value for a FIFO‐based stock.

Many products and raw materials have very short lives; they’re regularly replaced by new models (you know, with those ‘New and Improved!’ labels) because of the latest technology or marketing wisdom. These products aren’t around long enough to develop a wide gap between LIFO and FIFO, so the accounting choice between the two methods doesn’t make as much difference as with long‐lived products.

Manipulating LIFO stock levels to give profit a boost

The LIFO method opens the door to manipulation of profit - not that you would think of doing this, of course. Certainly, most of the businesses that choose LIFO do so to minimise current taxable income and delay paying taxes on it as long as possible - a legitimate (though perhaps misguided in some cases) goal. However, some unscrupulous managers know that they can use the LIFO method to ‘create’ some profit when business isn’t going well.

So if a business that uses LIFO sells more products than it purchased (or manufactured) during the period, it has to reach back into its stock account and pull out older costs to transfer to the cost of goods sold expense. These costs are much lower than current costs, leading to an artificially low cost of goods sold expense, which in turn leads to an artificially high gross margin figure. This dipping into old cost layers of LIFO‐based stock is called a LIFO liquidation gain.

So if a business that uses LIFO sells more products than it purchased (or manufactured) during the period, it has to reach back into its stock account and pull out older costs to transfer to the cost of goods sold expense. These costs are much lower than current costs, leading to an artificially low cost of goods sold expense, which in turn leads to an artificially high gross margin figure. This dipping into old cost layers of LIFO‐based stock is called a LIFO liquidation gain.

This unethical manipulation of profit is possible for businesses that have been using LIFO for many years and have stock cost values far lower than the current purchase or manufacturing costs of products. By not replacing all the quantities sold, they let stock fall below normal levels.

Suppose that a retailer sold 100,000 units during the year and normally would have replaced all units sold. Instead, it purchased only 90,000 replacement units. Therefore, the other 10,000 units were taken out of stock, and the accountant had to reach back into the old cost layers of stock to record some of the cost of goods sold expense. To see the impact of LIFO liquidation gain on the gross margin, check out what the gross margin would look like if this business had replaced all 100,000 units versus the gross margin for replacing only 90,000. In this example, the old units in stock carry a LIFO‐based cost of only £30, whereas the current purchase cost is £65. Assume that the units have a £100 price tag for the customer.

|

Gross margin if the business replaced all 100,000 of the units sold |

||

|

Sales revenue (100,000 units at £100 per unit) |

£10,000,000 |

|

|

Cost of goods sold expense (100,000 units at £65 per unit) |

6,500,000 |

|

|

Gross margin |

£3,500,000 |

|

|

Gross margin if the business replaced only 90,000 of the units sold |

||

|

Sales revenue (100,000 units at £100 per unit) |

£10,000,000 |

|

|

Cost of goods sold expense: |

||

|

Units replaced (90,000 units at £65 per unit) |

£5,850,000 |

|

|

Units from stock (10,000 units at £30 per unit) |

300,000 |

6,150,000 |

|

Gross margin |

£3,850,000 |

The LIFO liquidation gain (the difference between the two gross margins) in this example is £350,000 - the £35 difference between the old and the current unit costs multiplied by 10,000 units. Just by ordering fewer replacement products, this business padded its gross margin - but in a very questionable way.

Of course, this business may have a good, legitimate reason for trimming stock by 10,000 units - to reduce the capital invested in that asset, for example, or to anticipate lower sales demand in the year ahead. LIFO liquidation gains may also occur when a business stops selling a product and that stock drops to zero. Still, we have to warn investors that when you see a financial statement reporting a dramatic decrease in stock and the business uses the LIFO method, you should be aware of the possible profit manipulation reasons behind the decrease.

Note: A business must disclose in the footnotes to its financial statements any substantial LIFO liquidation gains that occurred during the year. The outside auditor should make sure that the company includes this disclosure. (Book VI, Chapter 3 discusses audits of financial statements by auditors.)

The average cost method

Although not nearly as popular as the FIFO and LIFO methods, the average cost method seems to offer the best of both worlds. The costs of many things in the business world fluctuate; business managers focus on the average product cost over a time period. Also, the averaging of product costs over a period of time has a desirable smoothing effect that prevents cost of goods sold from being overly dependent on wild swings of one or two purchases.

To many businesses, the compromise aspect of the method is its worst feature. Businesses may want to go one way or the other and avoid the middle ground. If they want to minimise taxable income, LIFO gives the best effect during times of rising prices. Why go only halfway with the average cost method? Or if the business wants its ending stock to be as near to current replacement costs as possible, FIFO is better than the average cost method. Even using computers to keep track of averages, which change every time product costs change, is a nuisance. No wonder the average cost method isn’t popular! But it is an acceptable method.

Identifying Stock Losses: Net Realisable Value (NRV)

Regardless of which method you use to determine stock cost, you should make sure that your accountants apply the net realisable value (NRV) test to stock. (Just to confuse you, this test is sometimes called the lower of cost or market (LCM) test.) A business should go through the NRV routine at least once a year, usually near or at year‐end. The process consists of comparing the cost of every product in stock - meaning the cost that’s recorded for each product in the stock asset account according to the FIFO or LIFO method (or whichever method the company uses) - with two benchmark values:

· The product’s current replacement cost (how much the business would pay to obtain the same product right now)

· The product’s net realisable value (how much the business can sell the product for)

If a product’s cost on the books is higher than either of these two benchmark values, your accountant should decrease product cost to the lower of the two. In other words, stock losses are recognised now rather than later, when the products are sold. The drop in the replacement cost or sales value of the product should be recorded now, on the theory that it’s better to take your medicine now than to put it off. Also, the stock cost value on the Balance Sheet is more conservative because stock is reported at a lower cost value.

Buying and holding stock involves certain unavoidable risks. Asset write‐downs, explained in the ‘Decision‐Making behind the Scenes in Profit and Loss Statements’ section of this chapter, are recorded to recognise the consequences of two of those risks - stock shrinkage and losses to natural disasters not fully covered by insurance. NRV records the losses from two other risks of holding stock:

· Replacement cost risk: After you purchase or manufacture a product, its replacement cost may drop permanently below the amount you paid (which usually also affects the amount you can charge customers for the products, because competitors will drop their prices).

· Sales demand risk: Demand for a product may drop off permanently, forcing you to sell the products below cost just to get rid of them.

Determining current replacement cost values for every product in your stock isn’t easy! Applying the NRV test leaves much room for interpretation.

Keeping accurate track of your stock costs is important to your bottom line both now and in the future, so don’t fall into the trap of doing a quick NRV scan and making a snap judgement that you don’t need a stock write‐down.

Some shady characters abuse NRV to cheat on their company tax returns. They write down their ending stock cost value - decrease ending stock cost more than can be justified by the NRV test - to increase the deductible expenses on their tax returns and thus decrease taxable income. A product may have a proper cost value of £100, for example, but a shady character may invent some reason to lower it to £75 and thus record a £25 stock write‐down expense in this period for each unit - which isn’t justified by the facts. But even though the person can deduct more this year, she’ll have a lower stock cost to deduct in the future. Also, if the person is selected for an HM Revenue & Customs audit and the tax inspectors discover an unjustified stock write‐down, the person may end up being charged with tax evasion.

Most accounting software packages either support or have plug‐in modules that allow you to run all these costing methods and compare their effect on your apparent financial performance. For example, Sage 50 Accounts 2015 supports the FIFO model. This means the cost price of the oldest stock is used to calculate the cost of stock.

Managing Your Stock Position

Businesses have to carry a certain minimum amount of stock to ensure the production pipeline works efficiently and likely demand is met. So the costs associated with ordering large quantities infrequently (and so reducing the order cost but increasing the cost of holding stock) have to be balanced with placing frequent orders (which pushes the cost of orders up but reduces stock holding costs). Economic Order Quantity (EOQ) is basically an accounting formula that calculates the most cost‐effective quantity to order; the point at which the combination of order costs and inventory carrying costs are at the minimum.

The formula for EOQ is

![]()

where R = annual demand in units; O = cost of placing an order; and C = cost of carrying a unit of inventory for the year.

Appreciating Depreciation Methods

We discussed depreciation earlier in Book III Chapter 3, but here we expand on the methods in a little more detail.

In theory, depreciation expense accounting is straightforward enough: you divide the cost of a fixed asset among the number of years that the business expects to use the asset. In other words, instead of having a huge lump‐sum expense in the year that you make the purchase, you charge a fraction of the cost to expense for each year of the asset’s lifetime. Using this method is much easier on your bottom line in the year of purchase, of course.

When calculating depreciation of your assets each year, you’ve a choice of two main methods: Straight Line and Reducing Balance. In this section, we explain these methods as well as the pros and cons of using each one.

Although other methods of calculating depreciation are available, for accounting purposes the two main methods are Straight Line and Reducing Balance. Both methods are acceptable, and it doesn’t matter to HM Revenue & Customs which you use. In practice, a business chooses one method and sticks with it. Straight‐Line suits those businesses that want to write off their assets more quickly.

To show you how the methods handle assets differently, we calculate the first year’s depreciation expense using the purchase of a piece of equipment on 1 January 2014, with a cost basis of £25,000. We assume the equipment has a useful life of five years, so the annual depreciation rate is 20 per cent.

Straight‐Line depreciation

When depreciating assets using the Straight‐Line method, you spread the cost of the asset evenly over the number of years that your business is going to use the asset. Straight‐Line is the most commonly used method for depreciation of assets, and the easiest one to use. The formula for calculating Straight‐Line depreciation is

· Cost of fixed asset × Annual depreciation rate = Annual depreciation expense

For the piece of equipment in this example, the cost basis is £25,000 and the annual depreciation rate is 20 per cent. With these figures, the calculation for finding the annual depreciation expense of this equipment based on the Straight‐Line depreciation method is

· £25,000 × 20% = £5,000 per annum

Each year, the business’s Profit and Loss statement includes £5,000 as a depreciation expense for this piece of equipment. You add this £5,000 depreciation expense to the Accumulated Depreciation account for this asset. You show this Accumulated Depreciation account below the asset’s original value on the Balance Sheet. You subtract the accumulated depreciation from the value of the asset to show a net asset value, which is the value remaining on the asset.

Reducing‐Balance depreciation

The Reducing‐Balance method of depreciation works well because it comes closest to matching the calculation of Capital Allowances, HM Revenue & Customs’ version of depreciation.

The peculiarity of this method is that, unlike Straight‐Line, the annual depreciation expense varies, and in theory the asset is never fully depreciated. Each year, you deduct the calculated depreciation figure from the previous year’s value to calculate the new brought‐forward figure. As time goes on, the annual depreciation figure gets smaller and the new brought‐forward figure for the asset gets gradually smaller and smaller - but the item never fully depreciates.

Using the same asset as in the preceding section at a cost of £25,000 and depreciating at an annual rate of 20 per cent, you calculate depreciation using the Reducing‐Balance method as follows:

·

|

Cost |

25,000 |

|

First year: depreciation (20%) |

5,000 |

|

Balance |

20,000 |

|

Second year: depreciation (20% of £20,000) |

4,000 |

|

Balance |

16,000 |

|

Third year: deprecation (20% of £16,000) |

3,200 |

|

Balance |

12,800 |

|

Fourth year: depreciation (20% of £12,800) |

2,560 |

|

Balance |

10,240 |

… and so on, forever.

By the way, the salvage value of fixed assets (the estimated disposal values when the assets are taken to the junkyard or sold off at the end of their useful lives) is ignored in the calculation of depreciation for income tax. Put another way, if a fixed asset is held to the end of its entire depreciation life then its original cost will be fully depreciated, and the fixed asset from that time forward will have a zero book value. (Recall that book value is equal to the cost minus the balance in the accumulated depreciation account.) Fully depreciated fixed assets are grouped with all other fixed assets in external Balance Sheets. All these long‐term resources of a business are reported in one asset account called property, plant and equipment (instead of fixed assets). If all its fixed assets were fully depreciated, the Balance Sheet of a company would look rather peculiar - the cost of its fixed assets would be completely offset by its accumulated depreciation. We’ve never seen this, but it would be possible for a business that hasn’t replaced any of its fixed assets for a long time.

Comparing the methods

The Straight‐Line method has strong advantages: it’s easy to understand and it stabilises the depreciation expense from year to year. But many business managers and accountants favour the Reducing‐Balance method. Keep in mind, however, that the depreciation expense in the annual Profit and Loss statement is higher in the early years when you use the Reducing‐Balance method, and so bottom‐line profit is lower until later years. Nevertheless, many accountants and businesses like the Reducing‐Balance method because it paints a more conservative (a lower, or a more moderate) picture of profit performance in the early years. Who knows? Fixed assets may lose their economic usefulness to a business sooner than expected. If this happens, using the Reducing‐Balance depreciation method would look good in hindsight.

Minimising taxable income and corporation tax in the early years to hang on to as much cash as possible is very important to many businesses, and they pay the price of reporting lower net profit in order to defer paying corporation tax for as long as possible. Or they may use the Straight‐Line method in their financial statements even though they use the Reducing‐Balance method in their annual tax returns, which complicates matters. (Refer to the section ‘Reconciling Corporation Tax’ for more information.)

Except for brand‐new enterprises, a business typically has a mix of fixed assets - some in their early years of depreciation, some in their middle years and some in their later years. So, the overall depreciation expense for the year may not be that different than if the business had been using Straight‐Line depreciation for all its fixed assets. A business does not have to disclose in its external financial report what its depreciation expense would have been if it had been using an alternative method. Readers of the financial statements can’t tell how much difference the choice of depreciation method made in that year.

Collecting or Writing Off Bad Debts

A business that allows its customers to pay on credit granted by the business is always subject to bad debts - debts that some customers never pay off. You are allowed, provided that you demonstrate serious efforts to recover the money owed, to write the loss in value off against your tax bill. You may also recover any value‐added tax (VAT) paid in respect of the invoice concerned. Don’t forget that in your role as an unpaid tax collector you’ll have charged your defaulting customer VAT, paid that over to HM Revenue & Customs as required, but failed to recover the loot from the said customer, along with the rest of the boodle owed.

Reconciling Corporation Tax

Corporation tax is a heavy influence on a business’s choice of accounting methods. Many a business decides to minimise its current taxable income by recording the maximum amount of deductible expenses. Thus, taxable income is lower, corporation tax paid to the Treasury is lower and the business’s cash balance is higher. Using these expense maximisation methods to prepare the Profit and Loss statement of the business has the obvious effect of minimising the profit that’s reported to the owners of the business. So, you may ask whether you can use one accounting method for corporation tax but an alternative method for preparing your financial statements. Can a business eat its cake (minimise corporation tax) and have it too (report more profit in its Profit and Loss statement)?

The answer is yes, you can. You may decide, however, that using two different accounting methods isn’t worth the time and effort. In other areas of accounting for profit, businesses use one method for income tax and an alternative method in the financial statements (but we don’t want to go into the details here).

When recording an expense, either an asset is decreased or a liability is increased. In this example, a special type of liability is increased to record the full amount of corporation tax expense: deferred tax payable. This unique liability account recognises the special contingency hanging over the head of the business to anticipate the time in the future when the business exhausts the higher depreciation amounts deducted in the early years by using, for example, the Reducing‐Balance method of depreciation, and moves into the later years when annual depreciation amounts are less than amounts by the Straight‐Line depreciation method. This liability account doesn’t bear interest. Be warned that the accounting for this liability can get very complicated. The business provides information about this liability in a footnote to its financial statements, as well as reconciling the amount of corporation tax expense reported in its Profit and Loss statement with the tax owed to the government based on its tax return for the year. These footnotes are a joy to read - just kidding.

Dealing with Foreign Exchange

Foreign exchange poses a tricky problem when it comes to accounting reports. Currencies just aren’t stable and they certainly don’t respect year‐end. A business can have all sorts of currency swishing around: pounds, dollars, euros, yen… . You need to include a note in your accounts to explain the extent of your use of foreign exchange and the way in which you’ve handled the conversion of currencies. In this section we explain three areas to pay particular attention to.

Transaction exposure

Transaction exposure occurs when a business incurs costs or generates revenues in any currency other than the one shown in its filed accounts. Two types of event can lead to this:

· A mismatch between cost of sales (manufacturing and so on) incurred in one currency and the actual sales income generated in another

· A time lag between setting the selling price in one currency and the date the customer actually pays up

As exchange rates frequently change, you need to explain how you handled the conversions.

Translation exposure

Translation exposure refers to the effects of movements in the exchange rate on the Balance Sheet and Profit and Loss statement that occur between reporting dates on assets and liabilities denominated in foreign currencies. In practice, any company that has assets or liabilities denominated in a currency other than the currency shown on its reported accounts has to ‘translate’ those back into the company’s reporting currency when the consolidated accounts have to be produced. This can be up to four times a year for major trading businesses. Any changes in the foreign exchange rate between the countries involved cause movements in the accounts.

Comparing performance

Exchange rate movements can make it difficult to compare one year with another; an essential accounting task if management is to keep track of how a business is performing. Accountants usually handle this movement by stating that current year revenue is compared to the prior financial year, translated on consistent exchange rates to eliminate distortions due to fluctuations in exchange rates. In any event, you need to include a note in the accounts showing how you’ve handled currency movements.

Two Final Issues to Consider

We think that you’ve been assuming all along that all expenses should be recorded by a business. Of course, you’re correct on this score. Many accountants argue that two expenses, in fact, aren’t recorded by businesses, but should be. A good deal of controversy surrounds both items. Many think one or both expenses should be recognised in measuring profit and in presenting the financial statements of a business:

· Share options: As part of their compensation packages, many public companies award their high‐level executives share options, which give them the right to buy a certain number of shares at fixed prices after certain conditions are satisfied (years of service and the like). If the market price of the company’s shares in the future rises above the exercise (purchase) prices of the share options - assuming the other conditions of these contracts are satisfied - the executives use their share options to buy shares below the going market price of the shares.

Should the difference between the going market price of the shares and the exercise prices paid for the shares by the executives be recognised as an expense? Generally accepted accounting principles don’t require that such an expense be recorded (unless the exercise price was below the market price at the time of granting the share option). However, the business must present a footnote disclosing the number of shares and exercise prices of its stock options, the theoretical cost of the share options to the business, and the dilution effect on earnings per share that exercising the share options will have. But this is a far cry from recording an expense in the Profit and Loss statement. Many persons, including Warren Buffett, who’s chair of Berkshire Hathaway, Inc, are strongly opposed to share options, thinking that the better alternative is to pay the executives in cash and avoid diluting earnings per share, which depresses the market value of the shares.

In brief, the cost to shareholders of share options is off the books. The dilution in the market value of the shares of the corporation caused by its share options is suffered by the shareholders, but doesn’t flow through the Profit and Loss statement of the business.

· Purchasing power of pound loss caused by inflation: Due to inflation, the purchasing power of one pound today is less than it was one year ago, two years ago and so on back in time. Yet accountants treat all pounds the same, regardless of when the pound amounts were recorded on the books. The cost balance in a fixed asset account (a building, for instance) may have been recorded 10 or 20 years ago; in contrast, the cost balance in a current asset account (stock, for instance) may have been recorded only one or two months ago (assuming the business uses the FIFO method). So, depreciation expense is based on very old pounds that had more purchasing power back then, and cost of goods sold expense is based on current pounds that have less purchasing power than in earlier years.

Stay tuned for what might develop in the future regarding these two expenses. If we had to hazard a prediction, we’d say that the pressure for recording the expense of share options will continue and might conceivably succeed - although we’d add that powerful interests oppose recording share options expense. On the other hand, the loss of purchasing power of the pound caused by inflation has become less important in an era signified by low inflation rates around the world. However, an enormous increase in the rate of inflation would resurrect this argument, and with rates of 5 per cent and more prevailing in some parts of ‘new’ Europe, 7 per cent in India, 10 per cent in Russia and 11 per cent in Turkey, the beast isn’t quite as dead as economists would like us to believe.

Have a Go

1. Table 2.1 presents the stock acquisition history of a business for its first year. The business sells 158,100 units during the year. Using the FIFO method, determine its cost of goods sold expense for the year and its cost of ending stock.

Table 2-1 History of Stock Acquisitions During the First Year

|

Quantity (Units) |

Cost Per Unit |

Total Cost |

|

|

First purchase |

14,200 |

£25.75 |

£365,650 |

|

Second purchase |

42,500 |

£23.85 |

£1,013,625 |

|

Third purchase |

16,500 |

£24.85 |

£410,025 |

|

Fourth purchase |

36,500 |

£23.05 |

£841,325 |

|

Fifth purchase |

6,100 |

£26.15 |

£159,515 |

|

Sixth purchase |

52,000 |

£23.65 |

£1,229,800 |

|

Seventh purchase |

18,200 |

£26.00 |

£473,200 |

|

Totals |

186,000 |

£4,493,140 |

2. The business in Table 2‐1 sells 158,100 units during the year. Using the LIFO method, determine its cost of goods sold expense for the year and its cost of ending stock.

3. Calculate the annual depreciation expense for a copier with a cost basis of £5,000 and a depreciation rate of 20 per cent using the Straight‐Line depreciation method.

4. Calculate the annual depreciation expense for a computer with a cost basis of £1,500 and a useful life of three years using the Straight‐Line depreciation method.

5. John has just bought a photocopier costing £8,000. He intends to depreciate it at a rate of 20 per cent, using the Reducing‐Balance method. Calculate the depreciation charges for the next three years and then write down the net book value at the end of the three‐year period.

6. If you wanted to apply an even amount of depreciation each year against your asset, which depreciation method would you use?

7. If you have a machine with a useful life of four years, and you want to use the Straight‐Line method of depreciation, what depreciation rate do you use?

8. How do you calculate net book value?

Answering the Have a Go Questions

1. Using the information given in table 2‐1 above, you can determine the cost of goods sold expense with the FIFO method as shown in Table 2‐2.

Table 2-2 Cost of Goods Sold Expense Calculation Using the FIFO Method

|

Quantity (Units) |

Cost Per Unit |

Total Cost |

|

|

First purchase |

14,200 |

£25.75 |

£365,650 |

|

Second purchase |

42,500 |

£23.85 |

£1,013,625 |

|

Third purchase |

16,500 |

£24.85 |

£410,025 |

|

Fourth purchase |

36,500 |

£23.05 |

£841,325 |

|

Fifth purchase |

6,100 |

£26.15 |

£159,515 |

|

Sixth purchase |

42,300 |

£23.65 |

£1,000,395 |

|

Totals |

158,100 |

£3,790,535 |

The business purchased 186,000 units of goods and these were acquired in seven different batches, as I outline in Table 2‐1. The business actually sold 158,000 of those units. Using a first‐in, first‐out method, the business would calculate the cost of goods sold, as being all of the first five batches purchased, plus 42,300 of the 52,000 units of purchase no. 6. This would enable you to calculate the cost of 158,000 units sold by summing the individual costs of each batch of goods purchased, as I show in Table 2‐2.

The cost of ending stock includes some units from the sixth purchase and all units from the seventh purchase, which is summarised in Table 2‐3.

Table 2-3 The cost of the remaining stock unsold (FIFO method)

|

Quantity (Units) |

Cost Per Unit |

Total Cost |

|

|

Sixth purchase |

9,700 |

£23.65 |

£229,405 |

|

Seventh purchase |

18,200 |

£26.00 |

£473,200 |

|

Totals |

27,900 |

£702,605 |

2. You determine the cost of goods sold expense with the LIFO as shown in Table 2‐4.

Table 2-4 Cost of Goods Sold Expense Calculation Using the LIFO Method

|

Quantity (Units) |

Cost Per Unit |

Total Cost |

|

|

Seventh purchase |

18,200 |

£26.00 |

£473,200 |

|

Sixth purchase |

52,000 |

£23.65 |

£1,229,800 |

|

Fifth purchase |

6,100 |

£26.15 |

£159,515 |

|

Fourth purchase |

36,500 |

£23.05 |

£841,325 |

|

Third purchase |

16,500 |

£24.85 |

£410,025 |

|

Second purchase |

28,800 |

£23.85 |

£686,880 |

|

Totals |

158,100 |

£3,800,745 |

Reversing the dates of stock purchased, you can see in Table 2‐4 that for the last‐in, first‐out (LIFO) calculation, all of batches three to seven are sold and only 28,800 units out of 42,500 units from the second batch purchased are sold. None of the first batch of purchases are sold. Calculating the cost of each of these batches allows you to find the total cost of goods sold using this method (see Table 2‐4).

The cost of ending stock includes all the units from the first purchase and some from the second purchase, as summarised in Table 2‐5.

Table 2-5 Cost of stock remaining that is unsold (LIFO method)

|

Quantity (Units) |

Cost Per Unit |

Total Cost |

|

|

Sixth purchase |

13,700 |

£23.85 |

£326,745 |

|

Seventh purchase |

14,200 |

£25.75 |

£365,650 |

|

Totals |

27,900 |

£692,395 |

3. The annual depreciation cost for the copier is as follows:

|

Cost price of photocopier |

£5,000 |

|

Depreciation (0.20 × £5,000) |

£1,000 |

4. The annual depreciation expense for the computer is as follows:

Cost price of computer £1,500

Depreciation (£1,500 ÷ 3 years) £500

This equates to a depreciation rate of 33.33 per cent (100% ÷ 3 years).

5. Using the Reducing Balance method, here’s what to do:

|

Year 1 |

|

|

Cost of photocopier |

£8,000 |

|

Depreciation at 20 per cent |

£1,600 (0.20 × £8,000) |

|

Net book value |

£6,400 |

|

Year 2 |

|

|

Depreciation at 20 per cent |

£1,280 (20 per cent of £6,400) |

|

Net book value |

£5,120 (£6,400 - £1,280) |

|

Year 3 |

|

|

Depreciation at 20 per cent |

£1,024 (20 per cent of £5,120) |

|

Net book value |

£4,096 (£5,120 - £1,024) |

6. Straight Line.

7. You use 25 per cent (100 per cent ÷ four years).

8. Cost of fixed assets less accumulated depreciation.