Bookkeeping & Accounting All-in-One For Dummies (2015)

Book IV

Working to Prepare Financial Statements

Chapter 2

Developing a Balance Sheet

In This Chapter

![]() Tackling the Balance Sheet

Tackling the Balance Sheet

![]() Pulling together your Balance Sheet accounts

Pulling together your Balance Sheet accounts

![]() Choosing a format

Choosing a format

![]() Drawing conclusions from your Balance Sheet

Drawing conclusions from your Balance Sheet

![]() Polishing your electronically produced Balance Sheet

Polishing your electronically produced Balance Sheet

Periodically, you want to know how well your business is doing. Therefore, at the end of each accounting period you draw up a Balance Sheet - a snapshot of your business’s condition. This snapshot gives you a picture of where your business stands - its assets, its liabilities and how much the owners have invested in the business at a particular point in time.

This chapter explains the key ingredients of a Balance Sheet and tells you how to pull them all together. You also find out how to use analytical tools called ratios to see how well your business is doing.

Breaking Down the Balance Sheet

Basically, creating a Balance Sheet is like taking a picture of the financial aspects of your business.

The business name appears at the top of the Balance Sheet along with the ending date for the accounting period being reported. The rest of the report summarises:

· The business’s assets, which include everything the business owns in order to stay in operation.

· The business’s debts, which include any outstanding bills and loans that it must pay.

· The owner’s capital, which is basically how much the business’s owners have invested in the business.

Assets, liabilities and capital probably sound familiar - they’re the key elements that show whether or not your books are in balance. If your liabilities plus capital equal assets, your books are in balance. All your bookkeeping efforts are an attempt to keep the books in balance based on this formula, which we talk more about in Book I, Chapter 2.

Generating Balance Sheets electronically

If you use a computerised accounting system, you can take advantage of its report function to generate your Balance Sheets automatically. These Balance Sheets give you quick snapshots of the business’s financial position, but may require adjustments before you prepare your financial reports for external use.

One key adjustment you’re likely to make involves the value of your stock. Most computerised accounting systems use the averaging method to value stock. This method totals all the stock purchased and then calculates an average price for the stock (see Book II, Chapter 3 for more information on stock valuation). However, your accountant may recommend a different valuation method that works better for your business. Therefore, if you use a method other than the default averaging method to value your stock, you need to adjust the stock value that appears on the Balance Sheet generated from your computerised accounting system.

Gathering Balance Sheet Ingredients

Most people now operate a computerised accounting system and the Balance Sheet is achieved simply by pressing a few buttons. However, you’ll find it useful to know how the Balance Sheet is constructed, and this chapter shows you how, with the aid of a fictitious set of accounts.

To keep this example simple, we’ve selected key accounts from the company’s Trial Balance as shown in Table 2-1:

Table 2-1 Balance Sheet Accounts

|

Account Name |

Balance in Account |

|

|

Debit |

Credit |

|

|

Cash |

£2,500 |

|

|

Petty Cash |

£500 |

|

|

Trade Debtors (Accounts Receivable) |

£1,000 |

|

|

Stock |

£1,200 |

|

|

Equipment |

£5,050 |

|

|

Vehicles |

£25,000 |

|

|

Furniture |

£5,600 |

|

|

Drawings |

£10,000 |

|

|

Trade Creditors (Accounts Payable) |

£2,200 |

|

|

Loans Payable |

£29,150 |

|

|

Capital |

£5,000 |

|

|

Net Profit for the Year |

£14,500 |

|

|

Total |

£50,850 |

£50,850 |

Dividing and listing your assets

The first part of the Balance Sheet is the assets section. The first step in developing this section is dividing your assets into two categories: current assets and fixed assets.

Current assets

Current assets are things your business owns that you can easily convert to cash and expect to use in the next 12 months to pay your bills and your employees. Current assets include cash, Trade Debtors (money due from customers) and stock. (We cover Trade Debtors in Book II, Chapter 2 and stock in Book II, Chapter 3.)

When you see Cash as the first line item on a Balance Sheet, that account includes what you have on hand in the tills and what you have in the bank, including current accounts, savings accounts and petty cash. In most cases, you simply list all these accounts as one item, Cash, on the Balance Sheet.

The current assets for the fictional business are:

|

Cash |

£2,500 |

|

Petty Cash |

£500 |

|

Trade Debtors |

£1,000 |

|

Stock |

£1,200 |

You total the Cash and Petty Cash accounts, giving you £3,000, and list that amount on the Balance Sheet as a line item called Cash.

Fixed assets

Fixed assets are things your business owns that you expect to have for more than 12 months. Fixed assets include land, buildings, equipment, furniture, vehicles and anything else that you expect to have for longer than a year.

The fixed assets for the fictional business are:

|

Equipment |

£5,050 |

|

Vehicles |

£25,000 |

|

Furniture |

£5,600 |

Most businesses have more items in the fixed assets section of a Balance Sheet than the few fixed assets we show here for the fictional business. For example:

Most businesses have more items in the fixed assets section of a Balance Sheet than the few fixed assets we show here for the fictional business. For example:

· A manufacturing business that has a lot of tools, dies or moulds created specifically for its manufacturing processes needs to have a line item called Tools, Dies and Moulds.

· A business that owns one or more buildings needs to have a line item labelled Land and Buildings.

· A business may lease its business space and then spend lots of money doing it up. For example, a restaurant may rent a large space and then furnish it according to a desired theme. Money the restaurant spends on doing up the space becomes a fixed asset called Leasehold Improvements and is listed on the Balance Sheet in the fixed assets section.

Everything mentioned so far in this section - land, buildings, leasehold improvements and so on - is a tangible asset. These items are ones that you can actually touch or hold. Another type of fixed asset is the intangible asset. Intangible assets aren’t physical objects; common examples are patents, copyrights and trademarks.

· A patent gives a business the right to dominate the markets for the patented product. When a patent expires (usually after 20 years), competitors can enter the marketplace for the product that was patented, and the competition helps to lower the price to consumers. For example, pharmaceutical businesses patent all their new drugs and therefore are protected as the sole providers of those drugs. When your doctor prescribes a brand-name drug, you’re getting a patented product. Generic drugs are products whose patents have run out, meaning that any pharmaceutical business can produce and sell its own version of the same product.

· A copyright protects original works, including books, magazines, articles, newspapers, television shows, movies, music, poetry and plays, from being copied by anyone other than the creator(s). For example, this book is copyrighted, so no one can make a copy of any of its contents without the permission of the publisher, John Wiley & Sons, Ltd.

· A trademark gives a business ownership of distinguishing words, phrases, symbols or designs. For example, check out this book’s cover to see the registered trademark, For Dummies, for this brand. Trademarks can last forever, as long as a business continues to use the trademark and files the proper paperwork periodically.

In order to show in financial statements that their values are being used up, all fixed assets are depreciated or amortised. Tangible assets are depreciated; see Book III, Chapter 3 for a brief overview on how to depreciate fixed assets. Intangible assets such as patents and copyrights are amortised (amortisation is similar to depreciation). Each intangible asset has a lifespan based on the number of years for which the rights are granted. After setting an initial value for the intangible asset, a business then divides that value by the number of years it has protection, and the resulting amount is then written off each year as an Amortisation Expense, which is shown on the Profit and Loss statement. You can find the total amortisation or depreciation expenses that have been written off during the life of the asset on the Balance Sheet in a line item called Accumulated Depreciation or Accumulated Amortisation, whichever is appropriate for the type of asset.

In order to show in financial statements that their values are being used up, all fixed assets are depreciated or amortised. Tangible assets are depreciated; see Book III, Chapter 3 for a brief overview on how to depreciate fixed assets. Intangible assets such as patents and copyrights are amortised (amortisation is similar to depreciation). Each intangible asset has a lifespan based on the number of years for which the rights are granted. After setting an initial value for the intangible asset, a business then divides that value by the number of years it has protection, and the resulting amount is then written off each year as an Amortisation Expense, which is shown on the Profit and Loss statement. You can find the total amortisation or depreciation expenses that have been written off during the life of the asset on the Balance Sheet in a line item called Accumulated Depreciation or Accumulated Amortisation, whichever is appropriate for the type of asset.

Acknowledging your debts

The liabilities section of the Balance Sheet comes after the assets section and shows all the money that your business owes to others, including banks, suppliers, contractors, financial institutions and individuals. Like assets, you divide your liabilities into two categories on the Balance Sheet:

· Current liabilities section: All bills and debts that you plan to pay within the next 12 months. Accounts appearing in this section include Trade Creditors (bills due to suppliers, contractors and others), Credit Cards Payable and the current portion of a long-term debt (for example, if you’ve a mortgage on your premises, the payments due in the next 12 months appear in the current liabilities section).

· Long-term liabilities section: All debts you owe to lenders that are to be paid over a period longer than 12 months. Mortgages Payable and Loans Payable are common accounts in the long-term liabilities section of the Balance Sheet.

Most businesses try to minimise their current liabilities because the interest rates on short-term loans, such as credit cards, are usually much higher than those on loans with longer terms. As you manage your business’s liabilities, always look for ways to minimise your interest payments by seeking longer-term loans with lower interest rates than you can get on a credit card or short-term loan.

Most businesses try to minimise their current liabilities because the interest rates on short-term loans, such as credit cards, are usually much higher than those on loans with longer terms. As you manage your business’s liabilities, always look for ways to minimise your interest payments by seeking longer-term loans with lower interest rates than you can get on a credit card or short-term loan.

The fictional business used for the example Balance Sheets in this chapter has only one account in each liabilities section:

|

Current liabilities: |

|

|

Trade Creditors |

£2,200 |

|

Long-term liabilities: |

|

|

Loans Payable |

£29,150 |

Naming your investments

Every business has investors. Even a small family business requires money up front to get the business on its feet. Investments are reflected on the Balance Sheet as capital. The line items that appear in a Balance Sheet’s capital section vary depending upon whether or not the business is incorporated. (Businesses incorporate primarily to minimise their personal legal liabilities; we talk more about incorporation in Book V, Chapter 1.)

If you’re preparing the books for a business that isn’t incorporated, the capital section of your Balance Sheet contains these accounts:

· Capital: All money invested by the owners to start up the business as well as any additional contributions made after the start-up phase. If the business has more than one owner, the Balance Sheet usually has a Capital account for each owner so that individual stakes in the business can be recorded.

· Drawings: All money taken out of the business by the business’s owners. Balance Sheets usually have a Drawing account for each owner in order to record individual withdrawal amounts.

· Retained Earnings: All profits left in the business.

For an incorporated business, the capital section of the Balance Sheet contains the following accounts:

· Shares: Portions of ownership in the business, purchased as investments by business owners.

· Retained Earnings: All profits that have been reinvested in the business.

Because the fictional business isn’t incorporated, the accounts appearing in the capital section of its Balance Sheet are:

|

Capital |

£5,000 |

|

Retained Earnings |

£4,500 |

Sorting out share investments

You’re probably most familiar with the sale of shares on the open market through the various stock market exchanges, such as the London Stock Exchange (LSE) and the Alternative Investment Market (AIM). However, not all companies sell their shares through public exchanges; in fact, most companies aren’t public companies but rather remain private operations.

Whether public or private, people become owners in a business by buying shares. If the business isn’t publicly traded, the owners buy and sell shares privately. In most small businesses, family members, close friends and occasionally outside investors buy shares, having been approached individually as a means to raise additional money to build the business.

The value of each share is set at the time the share is sold. Many businesses set the initial share value at £1 to £10.

Pulling Together the Final Balance Sheet

After you group together all your accounts (see the preceding section ‘Gathering Balance Sheet Ingredients’), you’re ready to produce a Balance Sheet. Businesses in the UK usually choose between two common formats for their Balance Sheets: the horizontal format or the vertical format, with the vertical format preferred. The actual line items appearing in both formats are the same; the only difference is the way in which you lay out the information on the page.

Horizontal format

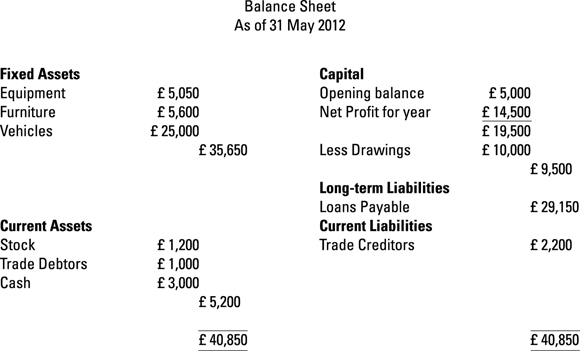

The horizontal format is a two-column layout with assets on one side and liabilities and capital on the other side.

Figure 2-1 shows the elements of a sample Balance Sheet in the horizontal format.

Figure 2-1: A sample Balance Sheet using the horizontal format.

Vertical format

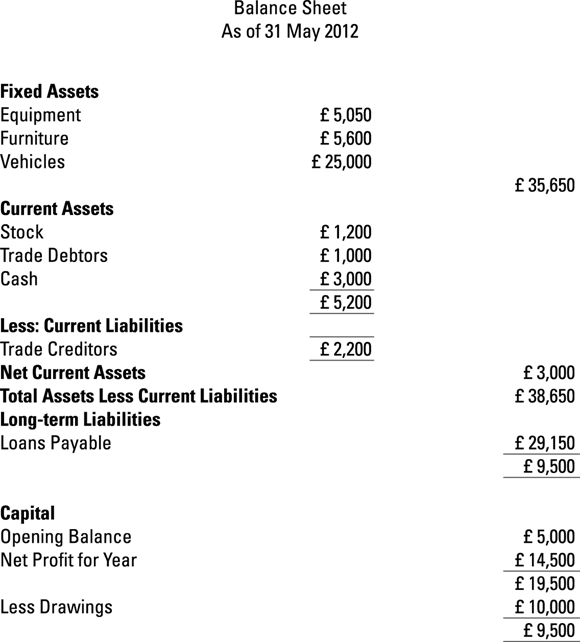

The vertical format is a one-column layout showing assets first, followed by liabilities and then capital.

Using the vertical format, Figure 2-2 shows the Balance Sheet for a fictional business.

Figure 2-2: A sample Balance Sheet using the vertical format.

Whether you prepare your Balance Sheet as per Figure 2-1 or Figure 2-2, remember that Assets = Liabilities + Capital, so both sides of the Balance Sheet must balance to reflect this.

The vertical format includes:

· Net current assets: Calculated by subtracting current assets from current liabilities - a quick test to see whether or not a business has the money on hand to pay bills. Net current assets is sometimes referred to as working capital.

· Total assets less current liabilities: What’s left over for a business’s owners after all liabilities have been subtracted from total assets. Total assets less current liabilities is sometimes referred to as net assets.

Putting Your Balance Sheet to Work

With a complete Balance Sheet in your hands, you can analyse the numbers through a series of ratio tests to check your cash status and monitor your debt. These tests are the type of tests that financial institutions and potential investors use to determine whether or not to lend money to or invest in your business. Therefore, a good idea is to run these tests yourself before seeking loans or investors. Ultimately, the ratio tests in this section can help you determine whether or not your business is in a strong cash position.

Testing your cash

When you approach a bank or other financial institution for a loan, you can expect the lender to use one of two ratios to test your cash flow: the current ratio and the acid test ratio (also known as the quick ratio).

Current ratio

This ratio compares your current assets to your current liabilities and provides a quick glimpse of your business’s ability to pay its bills in the short term.

The formula for calculating the current ratio is:

· Current assets ÷ Current liabilities = Current ratio

The following is an example of a current ratio calculation:

· £5,200 ÷ £2,200 = 2.36 (current ratio)

Lenders usually look for current ratios of 1.2 to 2, so any financial institution considers a current ratio of 2.36 a good sign. A current ratio under 1 is considered a danger sign because it indicates that the business doesn’t have enough cash to pay its current bills. This rule is only a rough guide and some business sectors may require a higher or lower current ratio figure. Get advice to see what the norm is for your business sector.

A current ratio over 2.0 may indicate that your business isn’t investing its assets well and may be able to make better use of its current assets. For example, if your business is holding a lot of cash, you may want to invest that money in some long-term assets, such as additional equipment, that you can use to help grow the business.

A current ratio over 2.0 may indicate that your business isn’t investing its assets well and may be able to make better use of its current assets. For example, if your business is holding a lot of cash, you may want to invest that money in some long-term assets, such as additional equipment, that you can use to help grow the business.

Acid test (quick) ratio

The acid test ratio uses only the Cash account and Trade Debtors in its calculation - otherwise known as liquid assets. Although similar to the current ratio in that it examines current assets and liabilities, the acid test ratio is a stricter test of a business’s ability to pay bills. The assets part of this calculation doesn’t take stock into account because it can’t always be converted to cash as quickly as other current assets and because in a slow market selling your stock may take a while.

Many lenders prefer the acid test ratio when determining whether or not to give a business a loan because of its strictness.

Calculating the acid test ratio is a two-step process:

1. Determine your quick assets.

Cash + Trade Debtors = Quick assets

2. Calculate your quick ratio.

Quick assets ÷ Current liabilities = Quick ratio

The following is an example of an acid test ratio calculation:

· £3,000 + £1,000 = £4,000 (quick assets)

· £4,000 ÷ £2,200 = 1.8 (acid test ratio)

Lenders consider that a business with an acid test ratio around 1 is in good condition. An acid test ratio of less than 1 indicates that the business can’t currently pay back its current liabilities.

Assessing your debt

Before you even consider whether or not to take on additional debt, always check out your debt condition. One common ratio that you can use to assess your business’s debt position is the gearing ratio. This ratio compares what your business owes - external borrowing - to what your business’s owners have invested in the business - internal funds.

Calculating your debt-to-capital ratio is a two-step process:

1. Calculate your total debt.

Current liabilities + Long-term liabilities = Total debt

2. Calculate your gearing ratio.

Total debt ÷ Capital = Gearing ratio

The following is an example of a debt-to-capital ratio calculation:

· £2,200 + £29,150 = £31,350 (total debt)

· £31,350 ÷ £9,500 = 3.3 (gearing ratio)

Lenders like to see a gearing ratio close to 1 because it indicates that the amount of debt is equal to the amount of capital. Most banks probably wouldn’t lend any more money to a business with a debt to capital ratio of 3.3 until its debt levels were lowered or the owners put more money into the business. The reason for this lack of confidence may be one of two:

· They don’t want to have more money invested in the business than the owners.

· They’re concerned about the business’s ability to service the debt.

We look at ratios in a lot more detail in Book VI, Chapter 2; skip ahead to see how investors may read the financial statements of a company.

Have a Go

The next section invites you to have a go at putting together a few Balance Sheets, so that you become more familiar with the component parts.

1. In which part of the Balance Sheet do you find the Furniture account?

2. In which part of the Balance Sheet do you find the Trade Creditors (Accounts Payable) account?

3. Describe the Owner’s Capital account.

4. Where do you find the Land and Buildings Account?

5. Whereabouts in the Balance Sheet do you find the Credit Cards Payable account?

6. Where do you find the Retained Earnings account?

7. To practise preparing a Balance Sheet in the horizontal format, use this list of accounts to prepare a Balance Sheet for the Abba Company as of the end of May 2014:

|

Cash |

£5,000 |

|

Debtors |

£2,000 |

|

Stock |

£10,500 |

|

Equipment |

£12,000 |

|

Furniture |

£7,800 |

|

Building |

£300,000 |

|

Creditors |

£5,200 |

|

Loans Payable |

£250,000 |

|

Owners Capital |

£52,000 |

|

Retained Earnings |

£30,100 |

8. To practise preparing a Balance Sheet in the vertical format, use this list of accounts to prepare a Balance Sheet for the Abba Company as of the end of May 2014:

|

Cash |

£5,000 |

|

Debtors |

£2,000 |

|

Stock |

£10,500 |

|

Equipment |

£12,000 |

|

Furniture |

£7,800 |

|

Building |

£300,000 |

|

Creditors |

£5,200 |

|

Loans Payable |

£250,000 |

|

Owners Capital |

£52,000 |

|

Retained Earnings |

£30,100 |

9. Your Balance Sheet shows that your current assets equal £22,000 and your current liabilities equal £52,000. What is your current ratio? Is that a good or bad sign to lenders?

10. Suppose that your Balance Sheet shows that your current assets equal £32,000 and your current liabilities equal £34,000. What would your current ratio be? Is that a good or bad sign to lenders?

11. Your Balance Sheet shows that your current assets equal £45,000 and your current liabilities are £37,000. What is your current ratio? Is that a good or bad sign to lenders?

12. Your Balance Sheet shows that your Cash account equals £10,000, your Debtors account equals £25,000 and your current liabilities equal £52,000. What would your acid test ratio be? Is that a good or bad sign to lenders?

13. Suppose that your Balance Sheet shows that your Cash account equals £15,000, your Debtors equals £17,000 and your current liabilities equals £34,000. What would your acid test ratio be? Is that a good or bad sign to lenders?

14. Suppose that your Balance Sheet shows that your Cash account equals £19,000, your Debtors equals £21,000 and your current liabilities equals £37,000. What would your acid test ratio be? Is that a good or bad sign to lenders?

15. A business’s current liabilities are £2,200 and its long-term liabilities are £35,000. The owners’ equity in the company totals £12,500. What is the debt-to-equity ratio? Is this a good or bad sign?

16. Suppose that a business’s current liabilities are £5,700 and its long-term liabilities are £35,000. The owners’ equity in the company totals £42,000. What is the debt-to-equity ratio? Is this ratio a good or bad sign?

17. Suppose that a business’s current liabilities are £6,500 and its long-term liabilities are £150,000. The owners’ equity in the company totals £175,000. What is debt-to-equity ratio? Is this ratio a good or bad sign?

Answering the Have a Go Questions

1. The Furniture account is regarded as a fixed asset because furniture is kept in the business for more than 12 months.

2. Trade Creditors (Accounts Payable) are suppliers that the business owes money to. This account is classified as a current liability.

3. Owners capital can be described as the money invested in the business by the owners. When owners put money into the business, this act can be described as capital introduced. When money is taken out, it can be taken as drawings (if the business is a sole trader or partnership) or dividends (if the business is a limited company).

4. The Land and Buildings account is part of fixed assets because land and buildings are kept in the business for a long period of time.

5. The Credit Cards payable account is money owed by the business to credit cards. This account is therefore a liability. Because the debt is due to be repaid within 12 months, the account is considered a Current Liability account.

6. The Retained Earnings account tracks the earnings that the owners reinvest in the business each year, and are part of the owners’ equity in the company.

7. The horizontal format would look like this:

|

Abba Company Balance Sheet; as of 31 May 2014 |

|||||

|

Fixed Asset |

Capital |

||||

|

Building |

£300,000 |

Opening balance |

£52,000 |

||

|

Equipment |

£12,000 |

Net Profit for the year |

£30,100 |

||

|

Furniture |

£7,800 |

£82,100 |

|||

|

£319,800 |

|||||

|

Current Assets |

Current Liabilities |

||||

|

Stock |

£10,500 |

Creditors |

£5,200 |

||

|

Debtors |

£2,000 |

||||

|

Cash |

£5,000 |

Long-Term Liabilities |

|||

|

Loans Payable |

£250,000 |

||||

|

Total Current Assets |

£17,500 |

||||

|

Total Assets |

£337,300 |

Total Liabilities and Equity |

£337,300 |

8. Here’s what the vertical format would look like:

|

Abba Company Balance Sheet; as of 31 May 2014 |

|||||

|

Fixed Assets |

|||||

|

Building |

£300,000 |

||||

|

Equipment |

£12,000 |

||||

|

Furniture |

£7,800 |

||||

|

£319,800 |

|||||

|

Current Assets |

|||||

|

Stock |

£10,500 |

||||

|

Debtors |

£2,000 |

||||

|

Cash |

£5,000 |

£17,500 |

|||

|

Less: Current Liabilities |

|||||

|

Creditors |

£5,200 |

||||

|

Net Current Assets |

£12,300 |

||||

|

Total Assets less Current Liabilities |

£332,100 |

||||

|

Long-Term Liabilities |

|||||

|

Loans Payable |

£250,000 |

||||

|

£82,100 |

|||||

|

Capital |

|||||

|

Opening Balance |

£52,000 |

||||

|

Retained Earnings |

£30,100 |

||||

|

Total Equity |

£82,100 |

9. Calculate the current ratio:

o £22,000 ÷ £52,000 = 0.42

This ratio is considerably below 1.2, so it would be considered a really bad sign. A ratio this low would indicate that a company may have trouble paying its bills because its current liabilities are considerably higher than the money the company has on hand in current assets.

10. Calculate the current ratio:

o £32,000 ÷ £34,000 = 0.94

The current ratio is slightly below the preferred minimum of 1.2, which would be considered a bad sign. A financial institution may loan money to this company, but consider it a higher risk. A company with this current ratio would pay higher interest rates than one in the 1.2 to 2 current ratio preferred range.

11. Calculate the current ratio:

o £45,000 ÷ £37,000 = 1.22

The current ratio is at 1.22, which would be considered a good sign and the company probably wouldn’t have difficulty borrowing money.

12. First you calculate your quick assets:

o £10,000 + £25,000 = £35,000

Then you calculate your acid test ratio:

o £35,000 ÷ £52,000 = 0.67

An acid test ratio of less than 1 would be considered a bad sign. A company with this ratio would have a difficult time getting a loan from a financial institution.

13. First you calculate your quick assets:

o £15,000 + £17,000 = £32,000

Then you calculate your acid test ratio:

o £32,000 ÷ £34,000 = 0.94

An acid test ratio of less than 1 would be considered a bad sign. Because this company’s acid test ratio is close to 1 it could probably get a loan, but would have to pay a higher interest rate because it would be considered a higher risk.

14. First you calculate your quick assets:

o £19,000 + £21,000 = £40,000

Then you calculate your acid test ratio:

o £40,000 ÷ £37,000 = 1.08

An acid test ratio of more than 1 would be considered a good sign. A company with this ratio would probably be able to get a loan from a financial institution without difficulty.

15. First, you calculate your total debt:

o £2,200 + £35,000 = £37,200

Then you calculate your debt-to-equity ratio:

o £37,200 ÷ £12,500 = 2.98

A debt-to-equity ratio of more than 1 would be considered a bad sign. A company with this ratio probably wouldn’t be able to get a loan from a financial institution until the owners put more money into the business from other sources, such as family and friends or a private investor.

16. First, you calculate your total debt:

o £5,700 + £35,000 = £40,700

Then you calculate your debt-to-equity ratio:

o £40,700 ÷ £42,000 = 0.97

A debt-to-equity ratio near 1 is considered a good sign. A company with this ratio is probably able to get a loan from a financial institution, but the institution may require additional funds from the owner or investors as well if the company is applying for a large, unsecured loan. A loan secured with assets, such as a mortgage, wouldn’t be a problem.

17. First, you calculate your total debt:

o £6,500 + £150,000 = £156,500

Then you calculate your debt-to-equity ratio:

o £156,500 ÷ £175,000 = 0.89

A debt-to-equity ratio of less than 1 would be considered a good sign. A company with this ratio would probably be able to get a loan from a financial institution.