Bookkeeping & Accounting All-in-One For Dummies (2015)

Book III

Undertaking Monthly and Quarterly Tasks

Chapter 3

Adjusting Your Books

In This Chapter

![]() Making adjustments for non-cash transactions

Making adjustments for non-cash transactions

![]() Checking your Trial Balance

Checking your Trial Balance

![]() Adding to and deleting from the Chart of Accounts

Adding to and deleting from the Chart of Accounts

During an accounting period, your bookkeeping duties focus on your business’s day-to-day transactions. When the time comes to report those transactions in financial statements, you must make adjustments to your books. Your financial reports are supposed to show your business’s financial health, so your books must reflect any significant change in the value of your assets, even if that change doesn’t involve the exchange of cash.

If you use cash-based accounting, these adjustments aren’t necessary because you only record transactions when cash changes hands. We talk about accrual and cash-based accounting in Book I, Chapter 2.

If you’re following the checklist we suggest in Book II, Chapter 1, we assume, in this chapter, that you’ve already entered/completed the following:

· Sale invoices

· Purchase invoices

· Bank receipts

· Bank payments

· Reconciled the bank accounts

All the above entries are routine transactions for the month. However, you also need to make some other types of adjustments. This chapter reviews the types of adjustments you need to make to the books before preparing the financial statements, including calculating depreciation, posting accruals and prepayments, updating stock figures and dealing with bad debts.

When you’ve posted all the necessary adjustments, print out a Trial Balance to check all the accounts and review for accuracy. We show you in the later section ‘Checking your Trial Balance’ how you can do this review using Sage 50 as an example.

When you’ve posted all the necessary adjustments, print out a Trial Balance to check all the accounts and review for accuracy. We show you in the later section ‘Checking your Trial Balance’ how you can do this review using Sage 50 as an example.

Adjusting All the Right Areas

We look at each of the adjustments that you need to make to your books in turn. These include the following areas:

· Asset depreciation: To recognise the use of assets during the accounting period.

· Accruals: Where goods or services have been received but not invoiced, and an accrual has to be made in the accounts, so that they can be matched with revenue for the month.

· Prepaid expenses: To match a portion of expenses that were paid at one point during the year, but for which the benefits are used throughout the year, such as an annual insurance premium. The benefit needs to be apportioned out against expenses for each month.

· Stock: To update stock to reflect what you have on hand.

· Bad debts: To acknowledge that some customers never pay and to write off those accounts.

Depreciating assets

The largest non-cash expense for most businesses is depreciation. Depreciation is an important accounting exercise for every business to undertake because it reflects the use and ageing of assets. Older assets need more maintenance and repair, and eventually need to be replaced. As the depreciation of an asset increases and the value of the asset dwindles, the need for more maintenance or replacement becomes apparent. The actual time to make this adjustment to the books is when you close the books for an accounting period. (Some businesses record depreciation expenses every month to match monthly expenses with monthly revenues more accurately, but other business owners only worry about depreciation adjustments on a yearly basis, when they prepare their annual financial statements.)

Depreciation doesn’t involve the use of cash. By accumulating depreciation expenses on an asset, you’re reducing the value of the asset as shown on the Balance Sheet (see Book IV, Chapter 2 for the low-down on Balance Sheets).

Depreciation doesn’t involve the use of cash. By accumulating depreciation expenses on an asset, you’re reducing the value of the asset as shown on the Balance Sheet (see Book IV, Chapter 2 for the low-down on Balance Sheets).

Readers of your financial statements can get a good idea of the health of your assets by reviewing your accumulated depreciation. If financial report readers see that assets are close to being fully depreciated, they know that you probably need to spend significant funds on replacing or repairing those assets soon. As they evaluate the financial health of the business, they take that future obligation into consideration before making a decision to lend money to the business or possibly invest in it.

Usually, you calculate depreciation for accounting purposes using the Straight-Line depreciation method. This method is used to calculate an equal amount to be depreciated each year, based on the anticipated useful life of the asset. For example, suppose that your business purchases a car for business purposes that costs £25,000. You anticipate that the car is going to have a useful lifespan of five years and be worth £5,000 after five years. Using the Straight-Line depreciation method, you subtract £5,000 from the total car cost of £25,000 to find the value of the car during its five-year useful lifespan (£20,000). Then, you divide £20,000 by five to find your depreciation charge for the car (£4,000 per year). When adjusting the assets at the end of each year in the car’s five-year lifespan, your entry to the books looks like this:

|

Debit |

Credit |

|

|

Depreciation Charge |

£4,000 |

|

|

Accumulated Depreciation: Vehicles |

£4,000 |

|

|

To record depreciation for Vehicles |

This entry increases depreciation charges, which appear on the Profit and Loss statement (see Book IV, Chapter 1). The entry also increases Accumulated Depreciation, which is the use of the asset and appears on the Balance Sheet directly under the Vehicles asset line. The Vehicles asset line always shows the value of the asset at the time of purchase.

You can accelerate depreciation if you believe that the business isn’t going to use the asset evenly over its lifespan - namely, that the business is going to use the asset more heavily in the early years of ownership. If you use a computerised accounting system as opposed to keeping your books manually, you may or may not need to make this adjustment at the end of an accounting period. If your system is set up with an asset register feature, depreciation is automatically calculated, and you don’t have to worry about it. Check with your accountant (the person who sets up the asset register feature) before calculating and recording depreciation expenses. We talk more about the different methods of depreciation in Book V, Chapter 2.

Accruing the costs

Goods and services may have been received by the business but may not have been invoiced. These costs need to be accrued, which means recorded in the books, so that they can be matched to the revenue for the month. These accruals are necessary only if you use the accrual accounting method. If you use the cash-based accounting method, you need to record the bills only when cash is actually paid. For more on the accrual and cash-based methods, refer to Book I, Chapter 2.

You accrue bills yet to be received. For example, suppose that your business prints and mails flyers to advertise a sale during the last week of the month. A bill for the flyers totalling £500 hasn’t been received yet. Here’s how you enter the bill in the books:

|

Debit |

Credit |

|

|

Advertising |

£500 |

|

|

Accruals |

£500 |

|

|

To accrue the bill from Jack’s Printing for June sales flyers |

This entry increases advertising expenses for the month and increases the amount due in the Accruals account. When you receive and pay the bill later, the Accruals account is debited rather than the Advertising account (to reduce the liability), and the Cash account is credited (to reduce the amount in the Cash account). You make the actual entry in the Cash Payments book when the cash is paid out.

When checking out the cash, also review any accounts in which expenses are accrued for later payment, such as Value-Added Tax Collected, to ensure that all Accrual accounts are up to date. This Tax account is actually a Liability account for taxes that you need to pay in the future. If you use the accrual accounting method, you must match the expenses related to these taxes to the revenues collected for the month in which they’re incurred.

Allocating prepaid expenses

Most businesses have to pay certain expenses at the beginning of the year even though they benefit from that expense throughout the year. Insurance is a prime example of this type of expense. Most insurance businesses require you to pay the premium annually at the start of the year even though the value of that insurance protects the business throughout the year.

For example, suppose that your business’s annual car insurance premium is £1,200. You pay that premium in January in order to maintain insurance cover throughout the year. Showing the full cash expense of your insurance when you prepare your January financial reports greatly reduces any profit that month and makes your financial results look worse than they actually are, which is no good. Instead, you record a large expense such as insurance or prepaid rent as an asset called Prepaid Expenses, and then you adjust the value to reflect that the asset is being used up.

When you record the initial invoice, you record the expense to prepayments. The double entry is as follows:

|

Debit |

Credit |

|

|

Prepayments |

£1,200 |

|

|

Bank |

£1,200 |

This double entry shows that you paid the original invoice by cheque and that you’ve coded the whole value of the invoice to prepayments.

Your £1,200 annual insurance premium is actually valuable to the business for 12 months, so you calculate the actual expense for insurance by dividing £1,200 by 12, giving you £100 per month.

Each month the Prepayment account is reduced by £100 and the cost is transferred to the Insurance Expenses account, as shown in this double entry:

|

Debit |

Credit |

|

|

Insurance Expenses |

£100 |

|

|

Prepaid Expenses |

£100 |

|

|

To record insurance expenses for March |

This entry increases Insurance Expenses on the Profit and Loss statement and decreases the asset Prepaid Expenses on the Balance Sheet. No cash changes hands in this entry because you laid cash out when the insurance bill was paid, and the Asset account Prepaid Expenses was increased in value at the time the cash was paid.

Counting stock

Stock is a Balance Sheet asset that you need to adjust at the end of an accounting period. During the accounting period, your business buys stock and records those purchases in a Purchases account without indicating any change to stock. When the business sells the products, you record the sales in the Sales account but don’t make any adjustment to the value of the stock. Instead, you adjust the stock value at the end of the accounting period because adjusting with each purchase and sale is much too time-consuming.

The steps for making proper adjustments to stock in your books are as follows:

1. Determine the stock remaining.

In addition to calculating closing stock using the purchases and sales numbers in the books, also do a physical count of stock to make sure that what’s on the shelves matches what’s in the books.

2. Set a value for that stock.

The value of closing stock varies depending on the method your business chooses for valuing stock. We talk more about stock value and how to calculate the value of closing stock in Book II, Chapter 3.

3. Adjust the number of items remaining in stock in the Stock account and adjust the value of that account based on the information collected in Steps 1 and 2.

If you record stock using your computerised accounting system, the system makes adjustments to stock as you record sales. At the end of the accounting period, the computer has already adjusted the value of your business’s closing stock in the books. Although the work’s done for you, still do a physical count of the stock to make sure that your computer records match the physical stock at the end of the accounting period.

Allowing for bad debts

No business likes to accept that money owed by some of its customers is never going to be received, but this situation is a reality for most businesses that sell items on credit. When your business determines that a customer who bought products on credit is never going to pay for them, you record the value of that purchase as a bad debt. (For an explanation of credit, check out Book II, Chapter 2.)

At the end of an accounting period, list all outstanding customer accounts in an Aged Debtor report, which is covered in Book II, Chapter 2. This report shows which customers owe how much and for how long. After a certain amount of time, you have to admit that some customers simply aren’t going to pay. Each business sets its own policy of how long to wait before tagging an account as a bad debt. For example, your business may decide that when a customer is six months late with a payment, you’re unlikely to ever see the money.

After you decide that an account is a bad debt, don’t include its value as part of your assets in Trade Debtors (Accounts Receivable). Including bad debt value doesn’t paint a realistic picture of your situation for the readers of your financial reports. Because the bad debt is no longer an asset, you adjust the value of your Trade Debtors to reflect the loss of that asset.

You can record bad debts in a couple of ways:

· By customer: Some businesses identify the specific customers whose accounts are bad debts and calculate the bad-debt expense for each accounting period based on specified customer accounts.

· By percentage: Other businesses look at their bad-debts histories and develop percentages that reflect those experiences. Instead of taking the time to identify each specific account that may be a bad debt, these businesses record bad-debt expenses as a percentage of their Trade Debtors.

· By using a bit of both: You can identify specific customers and write them off and apply a percentage to cover the rest.

However you decide to record bad debts, you need to prepare an adjusting entry at the end of each accounting period to record bad-debt expenses. Here’s an adjusting entry to record bad-debt expenses of £1,000:

|

Debit |

Credit |

|

|

Bad Debt Expense |

£1,000 |

|

|

Trade Debtors |

£1,000 |

|

|

To write off customer accounts |

You can’t have bad-debt expenses if you don’t sell to your customers on credit. You only need to worry about bad debt if you offer your customers the convenience of buying your products on credit.

If you use a computerised accounting system, check the system’s instructions for how to write off bad debts. To write off a bad debt using Sage 50 Accounts, follow these steps:

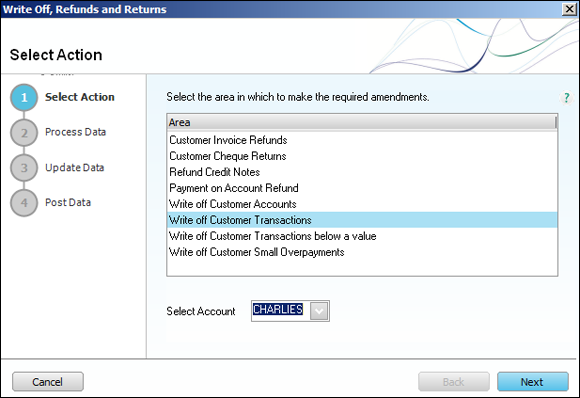

1. Open the Customers screen and select Customer Write Off/Refund from the Tasks on the left-hand side of the screen. This screen brings up the Write Offs, Refunds and Returns Wizard (see Figure 3-1). Select the task you want to perform, such as Write Off, and then select the customer account using the drop-down arrow. Click Next to continue.

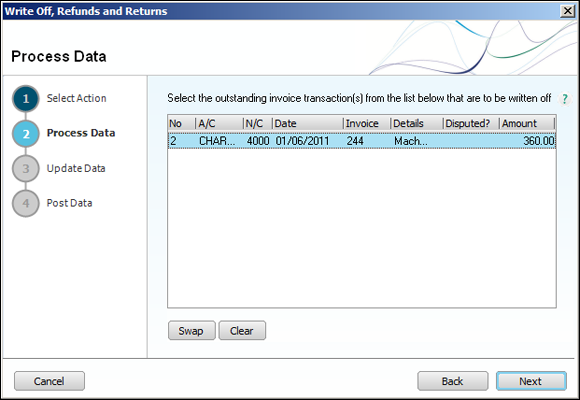

2. Highlight the invoices you’re writing off and click Next (see Figure 3-2).

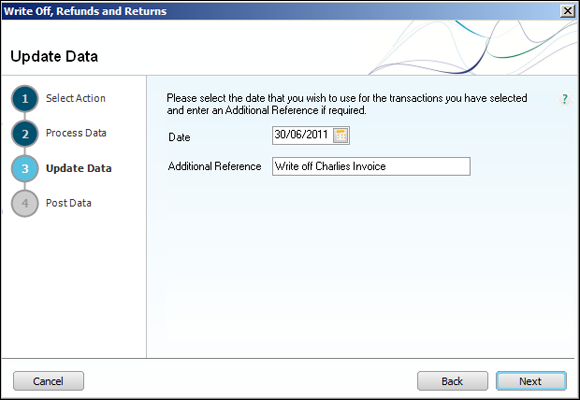

3. Enter the date of the write-off and any reference you may wish to use (see Figure 3-3). Click Next to continue.

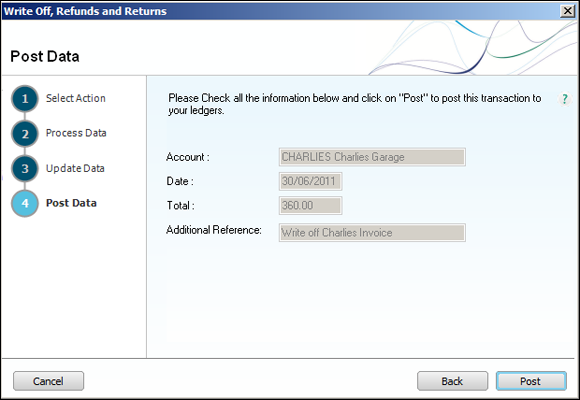

4. Check the data that’s about to be written off ( Figure 3-4). If you’re happy that the details are correct, click Post. Otherwise, click Back and redo.

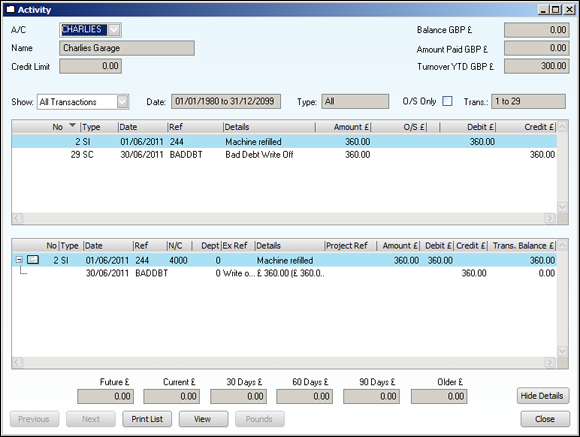

5. Double-click on the customer account and click the Activity tab to check that the write-off has been done (see Figure 3-5).

Figure 3-1: In Sage 50 Accounts, use the Write Offs, Refunds and Returns Wizard to write off bad debts.

Figure 3-2: Selecting the customer account in which you’re writing off debt in Sage 50 Accounts.

Figure 3-3: Selecting and highlighting the invoices you’re writing off in Sage 50 Accounts.

Figure 3-4: Confirming the details of the write-off in Sage 50 Accounts.

Figure 3-5: Check that the write-off has been posted properly by viewing the Customer Activity screen.

Checking Your Trial Balance

When you’ve entered all your transactions and then posted your adjusting entries, such as depreciation, accruals, prepayments and so on, you need to review all your account balances to ensure the accuracy of the data.

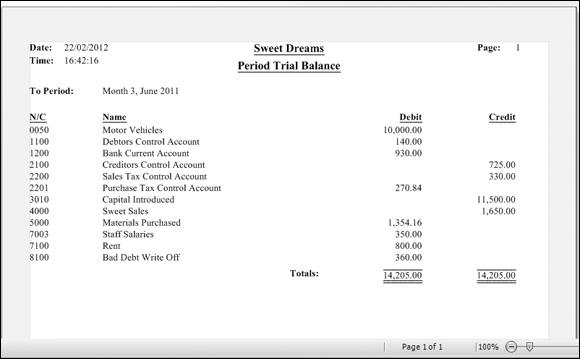

To do this, you need to run a Trial Balance, which shows you a list of all accounts with a current balance. The report is listed in account number order as shown in Figure 3-6.

Figure 3-6: An example of a Trial Balance in Sage 50.

You can see from looking at the Trial Balance that it’s simply a list of all the nominal accounts that contain a balance. The debit balances are shown in one column and the credit balances are shown in another. The totals of each of the columns must always be equal. If they aren’t, this difference means that there’s a major problem with your accounts. Computerised trial balances are always going to balance, unless there’s serious corruption of data. If you’re maintaining a manual Trial Balance, you must check all your figures again.

You may want to make further adjustments after you’ve reviewed your Trial Balance. Perhaps you posted items to the wrong nominal code. You need to write out correcting entries to sort this mistake out. This is where your double-entry rules come back into play.

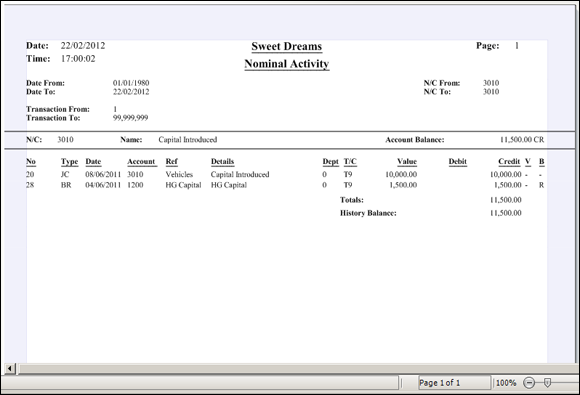

You may want to investigate an account because the balance seems high. For example, Kate the bookkeeper wants to see what’s been coded to Capital Introduced, because at £11,500 the amount seems quite high. In order to investigate this account, Kate would have to run a Nominal Activity report in Sage. This report would show her all the items that have been posted to the nominal code she’s investigating. See Figure 3-7 for the Nominal Activity report that Kate has run for Capital Introduced.

You may want to investigate an account because the balance seems high. For example, Kate the bookkeeper wants to see what’s been coded to Capital Introduced, because at £11,500 the amount seems quite high. In order to investigate this account, Kate would have to run a Nominal Activity report in Sage. This report would show her all the items that have been posted to the nominal code she’s investigating. See Figure 3-7 for the Nominal Activity report that Kate has run for Capital Introduced.

Figure 3-7: Showing a Nominal Activity report for Capital Introduced.

Kate can see from the report that two items have been posted to Capital Introduced; one was for £10,000 and relates to the company vehicle that was bought using owner funds, and the other was cash lent to the business by the owner. Kate is happy with her findings and doesn’t need to make any adjustments.

Changing Your Chart of Accounts

After you finalise your Nominal Ledger for the year, you may want to make changes to your Chart of Accounts, which lists all the accounts in your accounting system. (For the full story on the Chart of Accounts, see Book I, Chapter 3.) You may need to add accounts if you think that you need additional ones or delete accounts if you think that they’re no longer needed.

Delete accounts from your Chart of Accounts only at the end of the year. If you delete an account in the middle of the year, your annual financial statements don’t reflect the activities in that account prior to its deletion. So even if you decide halfway through the year not to use an account, leave it on the books until the end of the year and then delete it.

You can add accounts to your Chart of Accounts throughout the year, but if you decide to add an account in the middle of the year in order to more closely track certain assets, liabilities, revenues or expenses, you may need to adjust some related entries.

Suppose that you start the year recording paper expenses in the Office Supplies Expenses account, but paper usage and its expense keeps increasing and you decide to track the expense in a separate account beginning in July.

First, you add the new account, Paper Expenses, to your Chart of Accounts. Then you prepare an adjusting entry to move all the paper expenses that were recorded in the Office Supplies Expenses account to the Paper Expenses account. In the interest of space and to avoid boring you, the adjusting entry below is an abbreviated one. In your actual entry, you’d probably detail the specific dates on which paper was bought as an office supplies expense rather than just tally one summary total.

|

Debit |

Credit |

|

|

Paper Expenses |

£1,000 |

|

|

Office Supplies Expenses |

£1,000 |

|

|

To move expenses for paper from the Office Supplies Expenses account to the Paper Expenses account |

Moving beyond the catch-all Miscellaneous Expenses account

When new accounts are added to the Chart of Accounts, the account most commonly adjusted is the Miscellaneous Expenses account. In many cases, you may expect to incur an expense only one or two times during the year, therefore making it unnecessary to create a new account specifically for that expense. But after a while, you find that your ‘rare’ expense is adding up, and you’d be better off with a designated account, meaning that you need to create adjusting entries to move expenses out of the Miscellaneous Expenses account.

For example, suppose you think that you’re going to need to rent a car for the business just once before you buy a new vehicle, and so you enter the rental cost in the books as a Miscellaneous Expense. However, after renting cars three times, you decide to start a Rental Expense account mid-year. When you add the Rental Expense account to your Chart of Accounts, you need to use an adjusting entry to transfer any expenses incurred and recorded in the Miscellaneous Expense account prior to the creation of the new account.

Have a Go

This section allows you to practise bookkeeping questions.

1. Using the information below, and using Figure 3-6 (a Sage 50 Trial Balance) as an example of how it should look, reconstruct a Trial Balance for the end of June.

Your totals for each of the accounts at the end of June are:

|

Account |

Debit |

Credit |

|

Cash Debit |

£2,500 |

|

|

Debtors Debit |

£1,500 |

|

|

Stock Debit |

£1,000 |

|

|

Equipment Debit |

£5,050 |

|

|

Vehicle Debit |

£25,000 |

|

|

Furniture Debit |

£5,600 |

|

|

Creditors Credit |

£2,000 |

|

|

Loans Payable Credit |

£28,150 |

|

|

Owner’s Capital Credit |

£5,000 |

|

|

Sales Credit |

£27,000 |

|

|

Purchases Debit |

£12,500 |

|

|

Advertising Debit |

£2,625 |

|

|

Interest Expenses Debit |

£345 |

|

|

Office Expenses Debit |

£550 |

|

|

Payroll Taxes Debit |

£425 |

|

|

Rent Expense Debit |

£800 |

|

|

Salaries and Wages Debit |

£3,500 |

|

|

Telephone Expenses Debit |

£500 |

|

|

Utilities Expenses Debit |

£255 |

2. Your company owns a copier that cost £30,000. Assume a useful life of five years. How much should you record for depreciation expenses for the year? What is your bookkeeping entry?

3. Your offices have furniture that cost £200,000. Assume a useful life of five years. How much should you record for depreciation expenses for the year? What is your adjusting entry?

4. Suppose that your company pays £6,000 for an advertising campaign that covers the period 1 January to 31 December. You have already received an invoice dated 15 January, which you’ve paid at the end of January. You’re closing the books for the month of May. How much should you have charged to the Profit and Loss account for the period to 31 May and what balance should remain in Prepayments?

5. Your accountant has prepared your year-end accounts, but hasn’t sent you a bill yet! From past experience, you know that you should accrue about £2,400. What journal entry do you need to make to enter this situation into the books?

6. At the end of the month, you find that you’ve £9,000 in Closing Stock. You started the month with £8,000 in Opening Stock. What adjusting entry would you make to the books?

7. At the end of the month you calculate your Closing Stock and find that the value is £250 more than your Opening Stock value, which means that you purchased stock during the month that was not used. What adjusting entry should you make to the books?

8. You identify six customers that are more than six months late paying their bills, and the total amount due from these customers is £2,000. You decide to write off the debt. What adjusting entry would you make to the books?

9. Your company has determined that, historically, 5 per cent of its debtors never pay. What adjusting entry should you make to the books if your Debtors account at the end of the month is £10,000?

10. You decide that you want to track the amount that you spend on postage separately. Prior to this, you were entering these transactions in the Office Expense account. You make this decision in May, five months into your accounting year. You’ve already entered £1,000 for postage expenses. What would you need to do to start the account in the middle of the accounting year?

11. You decide that you want to track telephone expenses separately from other utilities. Prior to this, you were entering these transactions in the Utilities Expense account. You make this decision in July, but have already recorded transactions totalling £1,400 in your books. What do you need to do to start this new account in the middle of the accounting year?

Answering the Have a Go Questions

1. Here’s how the completed Trial Balance should look:

|

Account |

Debit |

Credit |

|

Cash |

£2,500 |

|

|

Debtors |

£1,500 |

|

|

Stock |

£1,000 |

|

|

Equipment |

£5,050 |

|

|

Vehicle |

£25,000 |

|

|

Furniture |

£5,600 |

|

|

Creditors |

£2,000 |

|

|

Loans Payable |

£28,150 |

|

|

Owner’s Capital |

£5,000 |

|

|

Sales |

£27,000 |

|

|

Purchases |

£12,500 |

|

|

Advertising |

£2,625 |

|

|

Interest Expenses |

£345 |

|

|

Office Expenses |

£550 |

|

|

Payroll Taxes |

£425 |

|

|

Rent Expense |

£800 |

|

|

Salaries and Wages |

£3,500 |

|

|

Telephone Expenses |

£500 |

|

|

Utilities Expenses |

£255 |

|

|

TOTALS |

£62,150 |

£62,150 |

2. Annual depreciation expense = £30,000 ÷ 5 = £6,000

|

Debit |

Credit |

|

|

Depreciation expense |

£6,000 |

|

|

Accumulated depreciation: Office Machines |

£6,000 |

3. Annual depreciation expense = (£200,000) ÷ 5 = £40,000

|

Debit |

Credit |

|

|

Depreciation expense |

£40,000 |

|

|

Accumulated depreciation: Furniture & Fittings |

£40,000 |

4. The original invoice should be coded to Prepaid Expenses. You need to calculate the monthly charge for advertising, which would be £6,000 ÷ 12 months = £500 per month. Each month, you must do the following journal:

|

Debit |

Credit |

|

|

Advertising Costs |

£500 |

|

|

Prepaid Expenses |

£500 |

5. This journal has the effect of charging the Profit and Loss account with £500 each month and reducing the prepayment in the Balance Sheet.

6. Therefore, in May the balances are:

|

✵ Advertising Expenses (in Profit & Loss) |

£2,500 (£500 × 5 months) |

|

✵ Prepayment in Balance Sheet |

£3,500 (£6,000 - £2,500) |

7. The journal entry should be as follows:

|

Debit |

Credit |

|

|

Accountancy Costs |

£2,400 |

|

|

Accruals |

£2,400 |

8. You could, if you wanted, prepare a monthly accrual and post a monthly charge through the accounts. To do this, simply split the £2,400 by 12 and post £200 per month. When the actual invoice comes in, it should be coded to Accruals rather than Accounting Fees.

9. You ended the month with £1,000 more stock than you started with. So you need to increase the Stock on hand by £1,000 and decrease the Purchases expense by £1,000, because some of the stock purchased won’t be used until the next month. The entry would be:

|

Debit |

Credit |

|

|

Stock |

£1,000 |

|

|

Purchases |

£1,000 |

10. Your entry would be:

|

Debit |

Credit |

|

|

Stock |

£250 |

|

|

Purchases |

£250 |

11. This entry decreases the amount of the Purchases expenses because you purchased some of the Stock that you then didn’t use.

12. Your entry would be:

|

Debit |

Credit |

|

|

Bad Debt Expenses |

£2,000 |

|

|

Debtors (Accounts Receivable) |

£2,000 |

13. First you need to calculate the amount of the Bad Debt Expenses:

Bad Debt Expenses = £10,000 × 0.05 = £500

Your entry would be:

|

Debit |

Credit |

|

|

Bad Debt Expenses |

£500 |

|

|

Debtors |

£500 |

14. First you need to establish a new account called Postage Expenses in your Chart of Accounts.

Then you need to transfer the amount of transactions involving the payment of postage from your Office Expenses account to your new Postage Expenses account. The transaction looks like this:

|

Debit |

Credit |

|

|

Postage Expenses |

£1,000 |

|

|

Office Expenses |

£1,000 |

15. First you need to establish a new account called Telephone Expenses in your Chart of Accounts. Then you need to transfer the amount of transactions involving the payment of telephone bills from your Utilities Expenses account to your Telephone Expenses account. The transaction looks like this:

|

Debit |

Credit |

|

|

Telephone Expenses |

£1,400 |

|

|

Utilities Expenses |

£1,400 |