HBR’s 10 Must Reads (2015)

Contextual Intelligence

by Tarun Khanna

WHETHER AS MANAGERS or as academics, we study business to extract learning, formalize it, and apply it to puzzles we wish to solve. That’s why we go to business school, why we write case studies and develop analytic frameworks, why we read HBR.

I believe deeply in the importance of that work: I’ve spent my career studying business as it is practiced in varied global settings.

But I’ve come to a conclusion that may surprise you: Trying to apply management practices uniformly across geographies is a fool’s errand, much as we’d like to think otherwise. To be sure, plenty of aspirations enjoy wide if not universal acceptance. Most entrepreneurs and managers agree, for example, that creating value and motivating talent are at the heart of what they do. But once you drill below the homilies, differences quickly emerge over what constitutes value and how to motivate people. That’s because conditions differ enormously from place to place, in ways that aren’t easy to codify—conditions not just of economic development but of institutional character, physical geography, educational norms, language, and culture. Students of management once thought that best manufacturing practices (to take one example) were sufficiently established that processes merely needed tweaking to fit local conditions. More often, it turns out, they need radical reworking—not because the technology is wrong but because everything surrounding the technology changes how it will work.

It’s not that we’re ignoring the problem—not at all. Business schools increasingly offer opportunities for students and managers to study practices abroad. At Harvard Business School, where I teach, international research is essential to our mission, and we now send first-year MBA students out into the world to briefly experience the challenges local businesses face. Nonetheless, I continually find that people overestimate what they know about how to succeed in other countries.

Context matters. This is not news to social scientists, or indeed to my colleagues who study leadership, but we have paid it insufficient attention in the field of management. There is nothing wrong with the analytic tools we have at our disposal, but their application requires careful thought. It requires contextual intelligence: the ability to understand the limits of our knowledge and to adapt that knowledge to an environment different from the one in which it was developed. (The term is not new; my HBS colleagues Anthony Mayo and Nitin Nohria have recently used it in the pages of HBR, and academic references date from the mid-1980s.) Until we acquire and apply this kind of intelligence, the failure rate for cross-border businesses will remain high, our ability to learn from experiments unfolding across the globe will remain limited, and the promise of healthy growth worldwide will remain unfulfilled.

Why Knowledge Often Doesn’t Cross Borders

I started thinking about contextual intelligence some years ago, when my colleague Jan Rivkin and I studied how profitable different industries were in various countries. To say that what we found surprised us would be an understatement.

First some background. Into the 1990s, empirical economists studying the economies of the OECD member countries, whose data were readily available, concluded that similar industries tended to have similar structures and deliver similar economic returns. This led to a widespread assumption that a given industry would be just as profitable or unprofitable in any country—and that industry analysis, one of the most rigorous tools we have, would support that assumption. But when data from multiple non-OECD countries became available, we could not replicate those results. Knowing something about the performance of a particular industry in one country was no guarantee that we could predict its structure or returns elsewhere. (See the sidebar “How Well Correlated Is Industry Profitability Across Countries?”)

Idea in Brief

The Finding

Most universal truths about management play out differently in different contexts: Best practices don’t necessarily travel.

The Implications

Global companies won’t succeed in unfamiliar markets unless they adapt—or even rebuild—their operating models.

The Solution

The first steps in that adaptation are the toughest: jettisoning assumptions about what will work and then experimenting to find out what actually does work.

To see why performance might vary so much, consider the cement industry. The technology for manufacturing cement is similar everywhere, but individual cement plants are located within specific contexts that vary widely. Corrupt materials suppliers may adulterate the mixtures that go into cement. Unions may support or impede plant operations. Finished cement may be sold to construction firms in bulk or to individuals in bags. Such variables often outweigh the unifying effect of a common technology. A cement plant manager moving to an unfamiliar setting would indeed have a leg up on someone who had never managed such a plant before, but not by nearly as much as she might think.

Rather than assume that technical knowledge will trump local conditions, we should expect institutional context to significantly affect industry structure. Each of Michael Porter’s five forces (which together describe industry structure) is influenced by local institutions, such as those that enforce contracts and provide capital. In a country where only established players have access to these, incumbent cement producers can prevent the emergence of new rivals. That consolidation of power means they can keep prices high. To use the language of business strategists, the logic of how value is created and divided among industry participants is unchanged, but its application is constrained by contextual variables. The institutional context affects the cement maker’s profitability far more than how good she is at producing cement.

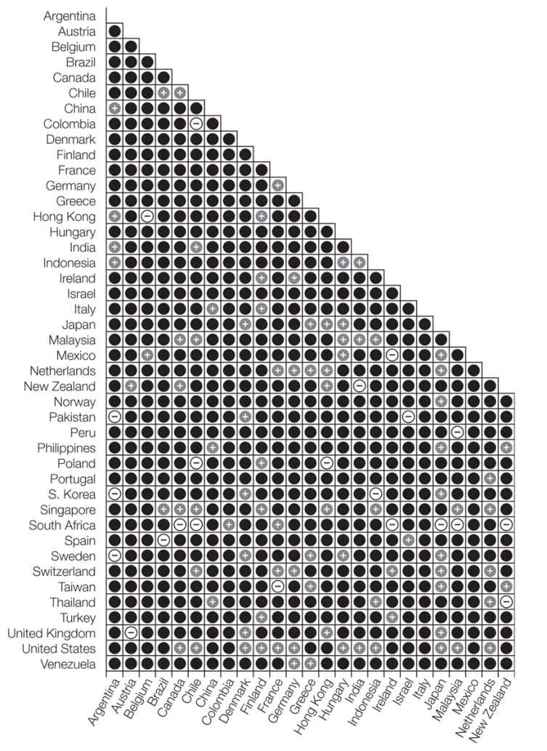

How Well Correlated Is Industry Profitability Across Countries?

by Tarun Khanna and Jan W. Rivkin

UNTIL RECENTLY, MANY STRATEGISTS believed that patterns of profitability in developed countries would show up in less developed economies as well. They couldn’t know for sure, because empirical research on business strategy had focused on a small handful of advanced economies. But it was often assumed that if an industry was highly profitable in, say, Germany, it would also be highly profitable in Thailand or Brazil.

In 2001, as good data on emerging markets started to become available, we checked that assumption by computing the average profitability of individual industries in each of 43 countries and checking correlation between the countries in every pairing.

If it were indeed true that profitability is predictable from country to country, most of this chart would be dark gray, reflecting significant positive correlation (meaning that industries profitable in one country are likely to be so in others, to a degree beyond the relationship prone to arise by chance). Such correlation, however, exists in only about 11% of cases, and it’s often between similar nations—the United States and Canada, for example.

Instead the chart is dominated by black: There’s no significant correlation of industry profitability between most of these country pairs. The fact that an industry is highly profitable in Sweden tells us nothing about whether it will be profitable in Singapore.

The implications are alarming. Companies enter new markets all the time relying on what they think they know about how their industry works and the technical competencies that have allowed them to succeed in their home markets. But given the results of our study, it’s not much of a stretch to say that what you learn in your home market about a particular industry may have very little to do with what you’ll need to succeed in a new market.

Much of my academic work has focused on institutional context. With my colleague Krishna Palepu, I’ve explored the idea that developing countries typically lack the “specialized intermediaries” that allow new enterprises to reach a broad market: courts that adjudicate disputes, venture capitalists that lend money, accreditation agencies that corroborate claims, and so on. Over time these voids are filled by entrepreneurs and better-run governments, and eventually the country “emerges” with a formal economy that functions reasonably well. Our framework has proved useful to businesses and scholars trying to understand a particular country’s institutional context and how to build a business within it. (Our book Winning in Emerging Markets: A Road Map for Strategy and Execution looks at institutional voids in more depth.)

Contextual intelligence requires moving far beyond an analysis of institutional context into areas as diverse as intellectual property rights, aesthetic preferences, attitudes toward power, beliefs about the free market, and even religious differences. The most difficult work is often the “soft” work of adjusting mental models, learning to differentiate between universal principles and their specific embodiments, and being open to new ideas.

Even Good Companies Have a Really Hard Time

Businesses that have achieved success in one market invariably have tightly woven operating models and highly disciplined cultures that fit that market’s context—so they sometimes find it more difficult to pull those things apart and rebuild than other companies do. Shifting into a new context may be straightforward if just one or two parts of the model need to change. But generally the adaptations required are far more complicated than that. In addition, executives rarely understand precisely why their operating model works, which makes reverse engineering all the more difficult, even for highly successful companies.

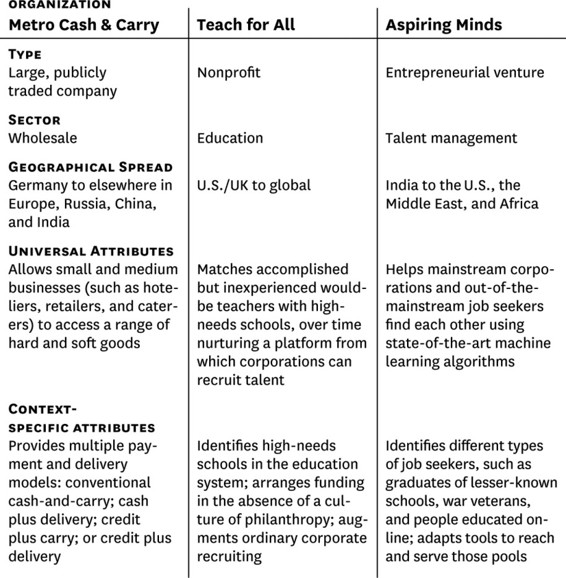

Metro Cash & Carry, a big-box wholesaler that provides urban businesses with fresh foods and dry goods, illustrates this point well. Metro successfully expanded from Germany to other parts of Western Europe and then to Eastern Europe and Russia, learning from each experience. So when the company entered the Chinese market, Metro executives knew they’d have to make adjustments but assumed that their basic recipe for success, tempered by what they’d learned, was transferable. They did indeed get a lot right, partly by developing effective partnerships and partly by helping provincial governments experiment with advanced food-safety techniques.

Nonetheless, the company ran into multiple challenges it had not fully anticipated. In any given location in China, learning how to work with the constellation of political and economic players took months. Lessons learned in one place often didn’t transfer to other places. Local competition was tougher overall than it had been in Eastern Europe and Russia (which Metro entered in an era of generalized scarcity, in the years after the Berlin Wall came down). Metro managers, who were used to large, formal competitors, experienced the multiplicity of agile rivals in the informal economy as almost a “fog of war.” Other challenges resulted from local tastes: Many consumers preferred to buy live or freshly butchered animals from wet markets, for example. As a result of these difficulties, the company didn’t break even in China until 2008—14 years after entering the market.

India turned out to be even tougher, although Metro had good reasons for optimism: It saw a way to cut out middlemen and thereby lower prices. It offered high-quality, standardized products in an environment with endemic food-quality and hygiene problems and staggering waste. Its wide assortment of goods seemed sure to appeal to its target customers—mom-and-pop retailers, which are so tightly packed together that India has the highest retailer density per capita in the world.

Still, Metro confronted obstacles different from those it had encountered in other markets. It had trouble getting around an anachronistic law that required farmers to sell all produce through government-run auctions. Traders and retailers that Metro thought would benefit from its presence put up raucous resistance. And for the first time in the company’s experience, no one seemed to be in charge: Metro couldn’t find a single-point political authority willing to advocate for it. In addition, its Indian customers were used to informal sources of credit and found it inconvenient to carry away wholesale quantities of goods and produce, owing to India’s dilapidated infrastructure.

Metro’s managers took a long time to understand that their model had to change, but they never really contemplated giving up. Just because a company is “global,” however, doesn’t mean it should do business in every country. Sometimes the amount of adaptation needed is so great that its core operating model would fall apart. Though Metro ultimately created more value in India than elsewhere, I believe, it did so only after very slow experimentation. This was partly because whatever adaptations the local team proposed and headquarters approved had to unfold in the context of an undisciplined political process and constant shrill criticism from unfamiliar media, often in the vernacular. Also, organizational rigidity had inevitably set in, stemming from individual managers’ overconfidence in the formula for past successes. Metro’s managers are first-rate, but contextual intelligence can’t be rushed or mandated into existence.

The difficulties I describe aren’t peculiar to developed-country companies trying to enter emerging markets. Metro’s tribulations in India, for example, resemble those that organized commerce faced with the Poujadism of 1950s France, when mom-and-pop businesses were up in arms against the establishment. Germany encountered similar forces in that period. And developing-economy enterprises trying to move into first-world markets have to change their operating models, too. Whereas at home they may have succeeded by managing around—or taking advantage of—conditions such as a cash-only society, intrusive or corrupt government officials, and a shortage of talent, they face different challenges in developed markets.

Narayana Health, founded in Bangalore, is an example. Its famous cardiac-surgery group performs 12% of the heart operations done in India each year. CABG (coronary artery bypass graft) surgery costs the patient as little as $2,000, compared with $60,000 to $100,000 in the United States, yet Narayana’s mortality and infection rates are the same as those of its U.S. counterparts. Still, it’s unclear whether the group’s operating model will transfer easily to the Cayman Islands, where Narayana opened a facility in February 2014. Why? Because it achieved success under specifically Indian conditions: A huge number of patients need the surgery, which means that surgeons quickly acquire expertise and thereby reduce costs. Having to overcome the logistical, financial, and behavioral barriers that kept poor patients away taught valuable lessons. Nurses double as respiratory and occupational therapists, and family members are now enlisted to help provide postoperative care. In addition, construction materials are inexpensive and the loose regulatory culture allows for experimentation. In the Caymans, Narayana will inevitably have to pull apart this operating model, and a coherent replacement will emerge only gradually.

Some early signs are encouraging. The Caymans’ material and labor costs are higher than India’s, but construction practices honed at home have already allowed Narayana to build a state-of-the-art hospital in the islands for much less than it would have cost in most Western locations. The health group has another big thing going for it: Its culture has been one of experimentation from the beginning. The Caymans’ very different regulatory systems will limit innovation in health care delivery methods, but an ingrained habit of questioning assumptions, trying out new approaches, and adjusting them in real time should serve Narayana well as it adapts.

How Can We Get Better at This?

Some of the ways to acquire contextual intelligence are obvious, though they’re neither easy nor cheap: hiring people who are “fluent” in more than one culture; partnering with local companies; developing local talent; doing more fieldwork and more cross-disciplinary work in business schools and requiring students to do the same; and taking the time to understand the nature and range of local variations. (See the sidebar “Tuning In to Cultural Differences.”) Exploring all those approaches in detail is beyond the scope of this article, but I’d like to highlight a few perhaps less obvious points.

The “hard” stuff is easy (believe it or not)

Once you accept up front that you know less than you think you do, and that your operating model will have to change significantly in new markets, researching a country’s institutional context isn’t difficult—in fact, general information is usually available. It can be helpful to work from a road map or a checklist, which will help you recognize and then categorize unfamiliar phenomena. (Winning in Emerging Markets provides a tool for spotting institutional voids along with checklists on product, labor, and capital markets in emerging economies.) The institutional context should influence not just your industry analysis but any other strategic tools you typically use: break-even analysis, identification of key corporate resources, and so on.

One big caveat: Developing economies often lack the data sources—credit registries, market research firms, financial analysts—that managers in OECD countries take for granted. This absence creates an institutional void in developing economies that companies must fill through investments of their own. HSBC partnered with a local retailer to create Poland’s first credit registry, for example, and Citibank did something similar in India as part of its effort to introduce credit cards there.

The soft stuff is hard

We tend to have very persistent mental models, particularly about emerging markets, that are not rooted in the facts and that get in the way of progress. One of these is the view that all countries will eventually converge on a free-market economy. But considerable evidence suggests that state-managed markets like China’s will be with us for the foreseeable future. I’ve written elsewhere that the Chinese government is the entrepreneur in that economy; to automatically equate governmental ubiquity with inefficiency, as we often do in the West, is wrong.

Tuning In to Cultural Differences

UNDERSTANDING LOCAL VARIATIONS involves observing both customers and employees. On the “buy” side, differing aesthetic tastes aren’t immediately apparent to many managers, but they matter a lot.

To succeed in India, Metro Cash & Carry increased the visual density of its stores’ previously uncluttered aisles so that they would more closely resemble crowded Indian street markets. In contrast, eBay stuck with its U.S. playbook in China, allowing Taobao to win the Chinese market in less than three years; the upstart succeeded in part by capitalizing on local responsiveness to colorful, active websites.

Computer scientists and cognitive psychologists have demonstrated that different cultural groups have differing tastes in how information and products are represented. (An interactive at labinthewild.org allows you to compare your engagement style with that of diverse other respondents.)

Tastes also differ in luxury services; for instance, hotel room décor that appeals to one set of customers may alienate another. Artwork evoking England in its imperial age may be pleasing in York but irritating in Mumbai. Chinese executives accustomed to celebratory red-and-gold furnishings may perceive modernist minimalism in their Berlin or New York hotel rooms as cold and hostile. Religious imagery is similarly controversial: The Hindu goddess of wealth is often used to connect products to prosperity in India, whereas companies in the West rarely use religious iconography to market their wares.

Advertising agencies must work with different manifestations of universal values all the time. Bartle Bogle Hegarty’s campaign for Johnnie Walker scotch whisky, for example, sought to link the product to the notion of a continual quest for self-improvement, which research had shown was the most powerful indicator of eventual male success. The iconic brand emblem—a striding man—embodied the idea that one should “keep walking.” But what worked in the West—ads that focused on individual progress—failed in China and Thailand, where customers responded instead to evocations of camaraderie, shared commitment, and collective advancement. (One of the creative leads of the campaign speculated with me recently that the man’s striding from left to right might well play differently in societies that write from right to left.)

On the “sell” side, managers must evaluate how to align incentives, motivation, and retention policies with local norms and expectations. If a country lacks efficient stock markets, for example, making stock options part of a compensation package becomes problematic. Similarly, individualized compensation schemes may be ineffective in an environment where collectivist values dominate.

A second persistent mind-set is the impulse to rely on simple explanations for complex phenomena. Metro’s managers were slow to reconceptualize their operating model in part because they found it easier to address one factor at a time and hope to be done with it. (I see this problem in my classes all the time—sophisticated executives read a case and home in on one particular difficulty, whereas in reality a constellation of intersecting issues must be addressed.) Often the cognitive biases that Kahneman and Tversky first wrote about—such as anchoring and overconfidence—reinforce this tendency.

Experimentation is messy—and essential

It’s not enough to identify which of our mental models and biases need to be jettisoned. We must develop new models and frameworks. They will of course be imperfect—but we can’t build a better knowledge base without codifying what we learn along the way. And that requires even billion-dollar corporations to think like entrepreneurs—to create hypotheses about what will work, to document and test assumptions, and to experiment in order to learn, cheaply and quickly, what does or doesn’t work. Like entrepreneurs, companies shouldn’t analyze experimental results to the point of exhaustion but instead develop the capacity to act speedily on results.

General ideas travel; specific dimensions may not

Learning to distinguish between the two is key. (Once again, creating value and motivating the workforce are universally considered essential—but the meaning of “value” and the road to “motivation” differ enormously between cultures.) Metro has continued to define itself in the same way across borders: as a B2B wholesaler that gives small and midsize enterprises access to a diverse range of hard and soft goods. But major adjustments were needed to make that definition work in varying contexts. Regarding payment and delivery, for example, Metro learned to manage not just conventional cash-and-carry operations, but also cash-and-no-carry, carry-and-no-cash, and no-cash-no-carry. (See “What’s Universal? What’s Context-Specific?”)

What’s Universal? What’s Context-Specific?

FIGURING OUT WHAT WILL TRAVEL from location to location and what won’t is essential for nonprofits and fast-growing entrepreneurial ventures as well as for the established companies we’ve discussed here.

Consider Teach for America, a nonprofit started in the late 1980s, which helps talented college graduates spend a few years teaching in America’s underperforming schools. It has recently mushroomed into a global network called Teach for All. The core ethos remains the same: Match willing, high-needs schools with recent graduates. But adapting the model requires a fair amount of contextual intelligence. Similarly, Aspiring Minds (of which I am a cofounder), an Indian talent-assessment service aimed at democratizing the market for talent, focuses on various out-of-the-mainstream job seekers in different markets.

The future can’t be telescoped

We all tend to assume that social and economic transformations occur more quickly than they actually do. Some technological changes have an immediate impact (mobile phones have disseminated rapidly in emerging markets), but they are the exception. Robust research shows that countries take decades, on average, to adopt new technologies invented elsewhere. Institutional change is, if anything, even slower.

Research with my colleague Krishna Palepu suggests, for example, that the transition in Chile from a focus on bank loans to a focus on issuing securities (a key transition for entrepreneurship) took much longer than anticipated two decades ago. More was required than the creation of new organizations and new rules: Individuals had to adapt their behavior to the changed context. That didn’t happen until foreign demand for information resulted in the emergence of local financial analysts and investment advisers, who first had to develop deep investing expertise. Similarly, in Korea the shift away from overreliance on bank debt and toward equity financing was far slower than proponents expected after the Asian financial crisis of the late 1990s. Analysts needed time to shed their biases, and it was difficult to locate truly independent directors.

For reasons akin to what we found in Chile and Korea, the harmonization of accounting, corporate governance, and intellectual property standards proceeds at a glacial pace relative to conventional managerial expectations—often because of political objections at the local level.

Generate your own data

To help focus on the facts as they are in a given context, rather than as managers think they should be, companies ought to obtain their own data whenever possible. This is particularly important when Western managers start to operate outside North America and Europe. What some scholars have called WEIRD (Western, educated, industrialized, rich, and democratic) societies may differ from the rest on a number of measures, including beliefs about fairness, a tendency to cooperate, the use of both inductive and moral reasoning, and concepts of self. Therefore, instead of hiring outsiders to do market research and assemble information on how other multinationals have entered a market, managers should conduct their own experiments to learn about the local context and what their company is capable of achieving within it. Some companies are experimenting with crowdsourcing data collection—a practice that’s still in its infancy but showing real promise.

Be aware that context matters when eliciting information. In some settings community norms affect behavior more than individual-level incentives do. Thus a company interested in water conservation might learn more from studying how villagers use the communal well than from studying household water use. Focus groups may be ineffective in hierarchical societies, so it is important to figure out what “status” looks like in a given location.

Success requires patience

As noted, institutional change can’t be rushed. Neither can enterprise-level change. Companies must be willing to invest in immersing their high-potential employees in particular local contexts. The global advertising giant WPP has a fellows program that places 10 recruits annually with its operating companies around the world to develop leaders with a multidisciplinary, culturally flexible perspective. Each fellow gains exposure and engagement while being mentored by senior WPP executives. Viewed as a ticket to success within the organization, the fellows program has resulted in 65% retention (over long time horizons) of these high-potential executives—a significant result in an industry notorious for turnover.

The Universal Importance of Contextual Intelligence

Understanding the limits of our knowledge, which is at the heart of contextual intelligence, is a very basic component of human comprehension. Yet it’s also a profoundly difficult, complicated process that has vexed philosophers from Plato to Isaiah Berlin, who distinguished between knowing the facts and making a judgment in a widely read 1996 essay.

I believe that contextual intelligence is systematically undervalued in dozens of situations. I’ve focused here on corporations planning to enter new markets. I could as easily have written about giant state-owned enterprises, entrepreneurs, and nonprofits that are tackling even bigger problems—such as how to expand the formal economy to include the 4 billion people who currently make a living in the informal economy. At best, this excluded population engages in rudimentary commerce mediated by personal relationships, which limits the possibility of expanding its networks. Engaging effectively with this population will take massive doses of contextual intelligence. We need to understand so many things better than we currently do: How do they prioritize spending, given their extremely limited resources? What forms of communication will they respond to? How can they accumulate capital in the absence of collateral? The answers to those questions will differ from Mumbai to Nairobi and from Nairobi to Santiago.

Originally published in September 2014. Reprint R1409C